By Mark Yamada and Ioulia Tretiakova

By Mark Yamada and Ioulia Tretiakova

Special to the Financial Independence Hub

Nobel laureate William Sharpe described managing retirement assets as the “nastiest hardest problem in finance.” Living longer on a fixed pool of capital is only the start of a problem complicated by the myriad of possible personal and family needs and obligations that develop over a lifetime.

The need

Demographics are driving big change in the retirement market. Not only will Gen Y workers have fewer opportunities to save for retirement because of high predicted job turnover and reduced access to workplace pensions, but retiring baby boomers are being abandoned by the very industries created to serve them.

The pension, mutual fund and wealth management industries are direct responses to boomers joining the work force, but fewer retiring boomers meet the criteria for investment advisors who are compensated for growing assets. Retiree portfolios don’t get contributions and many are too small to qualify as brokerage minimums rise. Most mutual fund fees are too high for this cohort for whom costs are more important than ever before. The number of advisors is also shrinking, not only because of compensation and compliance pressures but also because advisors too are retiring.

Saving more, starting earlier and taking more risk are the accepted ways to improve retirement outcomes. Two or more of these options may no longer be available for retirees. A growing crisis in retirement savings is stretching an already extended social welfare system and new thinking is needed if disaster is to be averted.

Solutions not products

Our research motivation (Journal of Retirement and two Rotman International Journal of Pension Management papers) is a belief that investing can be improved to solve problems. The pension problem, for example, is best resolved by focusing on what workers really want, reliable replacement income in retirement rather than trying to pick the best performer every period. Consumers today want solutions. The investment industry is still about products.

Just as someone who only owns a hammer sees every problem as a nail, the industry has a singular focus on “maximizing returns.” This sounds good, but anyone using Google maps knows the fastest route to a destination is not necessarily the shortest. UPS routes deliveries to avoid turns against oncoming traffic to reduce accidents and delays waiting for gaps. Their drivers make 90% right hand turns and experience shorter delivery times, lower fuel consumption and operate smaller fleets. What if investment portfolios could similarly be routed more efficiently to correct destinations?

Autonomous portfolios

The self-driving automobile that protects passengers from immediate risks and routes itself to a predetermined destination provides a template for an autonomous portfolio.

Getting to a destination is a different strategy than going as fast as possible all the time. For starters, brakes and steering are needed not just an accelerator pedal. Maximizing returns, the investment industry’s primary approach, is about going fast. If your strategic asset mix is 65% stocks and 35% bonds, your advisor will periodically rebalance to this mix. If stocks go down, she will buy more stocks. This sounds like the right thing to do, and it is, if your investing time horizon is long enough to make back accelerating loses over the next market cycle; your portfolio is throwing money at a falling market after all. For an aging population in general and retiring baby boomers in particular, this is an increasingly risky and unpalatable proposition.

How we can do it

To protect portfolios we keep risks as constant as possible. When volatility rises, some risky assets, like stocks, are sold and less risky ones, like bonds, are added. When volatility falls, we add riskier assets. The critical effect is avoiding big losses. Statistically this is like card counting in the casino game of blackjack. When volatility is higher than average, the deck is stacked against the player. This means we expose portfolios primarily to markets that are favorable. It’s an unfair advantage but it’s legal!

Two portfolios are used for the navigation (GPS) function; one for safety and one for growth. Both are maintained at constant risk to limit exposure to immediate market hazards. Progress towards the goal drives decision-making. If the overall portfolio falls behind, the balance shifts towards growth, “risk on.” When the portfolio is tracking properly or is ahead of target the shift is to safety, “risk-off.” The concept is simple and based on common sense. The critical elements are when and by how much risk should be increased/decreased and how to structure the two portfolios to maintain consistent risk. How long you and your spouse are likely to live is an important input.

We studied different ways to withdraw funds from a portfolio that were designed to make the money last longer. In addition, we assumed nobody would want to reduce spending once they retired. A hybrid spending policy plus the dynamic constant risk approach met this objective best.

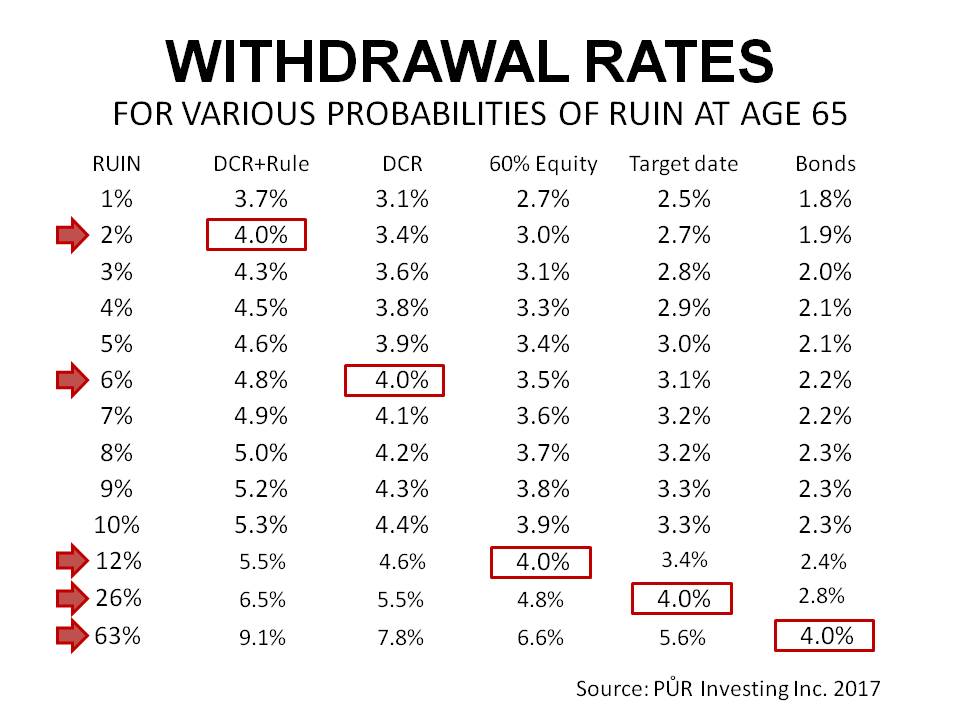

The table at the top of this blog shows key results. Withdrawal rates for each of five strategies ranging from all bonds (right column) to DCR plus hybrid spending rule (second left column) are shown. If your portfolio is 100% bonds and you are withdrawing 4% of the initial value of the portfolio at age 65, there is a 63% chance of running out of money. That is not good!

We used target date funds (TDFs) as the reference mix because it is the most popular default option in U.S. defined contribution pension plans (like group RRSPs in Canada). Target date fund asset mixes automatically become more conservative (less equity) as the retirement date approaches, relieving members of this task. A default option is the investment choice made by an employer when the plan member doesn`t choose an investment. Most deposits to DC plans go to TDFs. There are two types of TDF, one that ends at retirement date that force members to withdraw funds and invest on their own and a second group that manages the money through retirement with an asset mix that is the equivalent of a 50% equities 50% bond portfolio.

The TDF, with a 26% chance of ruin at a 4% withdrawal rate is also bad with a 26% probability of ruin (1 in 4) but is better than all bonds. The DCR+Rule could provide a 6.5% withdrawal rate, 62.5% higher, for the same 26% chance of running out money. Viewed a different way, staying with a 4% withdrawal rate with DCR+Rule would reduce the probability of ruin to 2%! Now there are choices. On average we observe a 51% increase in withdrawal rate between TDFs and DCR+Rule for probability of ruin below 25%.

How you can do it

Advisors: We will license the technology to qualified advisors for a fee. Our preference will be to establish enterprise licenses with advisor firms. Our software tracks individual portfolios and sends recommended rebalancing trades to the advisor to keep portfolios tracking towards their goals and provides feedback along the way.

Products: Introducing a solution into an industry geared to distribute products is challenging. We could develop a product that addresses the same needs, but it may not be as tailored as we would like.

Individual investors: We may offer tools on a monthly subscription basis so investors can assess their own needs and construct and manage their own solutions. If investors provide the sweat equity by learning about, building and monitoring a solution themselves, they can reduce costs and maximize the benefit of our approach.

Let us know what you think.

Mark Yamada, President and CEO of PŮR Investing Inc., has led teams of investment professionals including as president of the investment manage subsidiary of a multinational financial services company, was founding managing director of the private client division for a publicly-traded asset management firm and has served on the Investment Fund Products Advisory Committee of the Ontario Securities Commission. As co-author of the Rotman International Journal of Pension Management and Journal of Retirement research, Mark founded PŮR Investing to provide new solutions for individuals in an industry still focused on products.

Mark Yamada, President and CEO of PŮR Investing Inc., has led teams of investment professionals including as president of the investment manage subsidiary of a multinational financial services company, was founding managing director of the private client division for a publicly-traded asset management firm and has served on the Investment Fund Products Advisory Committee of the Ontario Securities Commission. As co-author of the Rotman International Journal of Pension Management and Journal of Retirement research, Mark founded PŮR Investing to provide new solutions for individuals in an industry still focused on products.

Ioulia Tretiakova, MSc., CFA, FRM, is VP and Director of Quantitative Strategies for PŮR Investing Inc. She has worked as a quantitative analyst in Toronto and New York and her research into the practical application of volatility management in mass-customized portfolios and the use of ridge regression in the analysis of ETFs is groundbreaking. Lead author of two peer-reviewed papers for the Rotman International Journal of Pension Management and recently for the Journal of Retirement, Ioulia’s application of stochastic control theory to practical challenges in retirement have changed thinking about defined contribution pension management.

Ioulia Tretiakova, MSc., CFA, FRM, is VP and Director of Quantitative Strategies for PŮR Investing Inc. She has worked as a quantitative analyst in Toronto and New York and her research into the practical application of volatility management in mass-customized portfolios and the use of ridge regression in the analysis of ETFs is groundbreaking. Lead author of two peer-reviewed papers for the Rotman International Journal of Pension Management and recently for the Journal of Retirement, Ioulia’s application of stochastic control theory to practical challenges in retirement have changed thinking about defined contribution pension management.

Well no explanation of what dcr is.. and the link has a required subscription. Seems like a complicated bet based on past occurrences. I could be wrong but this article does a poor job of explaining the process. If this process is so difficult to explain perhaps it’s just magic.