By Benjamin Felix, PWL Capital Inc.

Special to the Financial Independence Hub

When people have corporations it’s common for them to retain all earnings in excess of their living expenses inside of their corporations to avoid paying personal tax.

This seems logical. By leaving the money in the corporation there is more money to invest in the corporate investment account, and we know that about $50,000 of dividends can be taken out of a corporation nearly tax-free, making the idea of leaving everything in the corporation until it’s time to draw a conservative retirement income appear very attractive. This strategy may have also been motivated by the tax advantage that used to exist for taking a dividend-only income.

Shift to mix of salaries & dividends

Things have changed enough that we thought this common logic may be worth revisiting. With CRA tightening integration we are seeing more accountants recommend a mix of salary and dividends rather than an all-dividend income, bringing the RRSP back into the ring in the fight against taxes. And with the TFSA’s annual contribution room now sitting at $10,000 per year, it has become a heavyweight planning tool.

We set out to determine if it makes sense for incorporated individuals to withdraw additional salary or dividends in excess of their living expenses to contribute to the RRSP or TFSA, respectively. To do this, we modelled the total after-tax value of $1 of active small business income in the personal hands of the individual. This is best explained with examples:

· The individual can retain the $1 of excess earnings in the corporation, pay the 15.5% small business corporation tax, invest $0.845 in the corporate investment account, and eventually pay personal tax on the withdrawal of a dividend.

· They can draw $1 of additional salary (deductible to the corporation, and taxable in their personal hands), and then make an offsetting $1 RRSP contribution. In this case, tax is deferred leaving $1 to be invested in the RRSP which will eventually be taxed as income on withdrawal.

· They can pay the 15.5% small business corporation tax on the $1 of excess earnings, take out a dividend today (paying personal tax at 38.29%*), and invest $0.521 in the TFSA where there are no tax implications on an eventual withdrawal.

RRSP good option under all circumstances

The results of the analysis are intuitive. The RRSP is a good option under any circumstances because it offers income tax deferral, and tax-deferred investment growth. If the tax rate on withdrawal is expected to be lower than the tax rate on contribution, the RRSP becomes more attractive than both the TFSA and the corporation.

If the tax rate on contributions is expected to be the same as the tax-rate on withdrawals, the individual is indifferent between the RRSP and TFSA, but favours them both over the corporation. While using the TFSA involves taking a significant haircut upfront, all future growth will be tax-free. This means that the rate of growth in the TFSA will be higher than the after tax rate of growth of the corporate investment account.

Given a long enough period of time, the TFSA will overcome its initial tax hit and surpass the after-tax value of the corporate investment account. The TFSA has no time restrictions, and can remain untouched to eventually pass to a beneficiary tax-free on the death of the individual – depending on the age and health of the owner, it can have a very, very long time horizon.

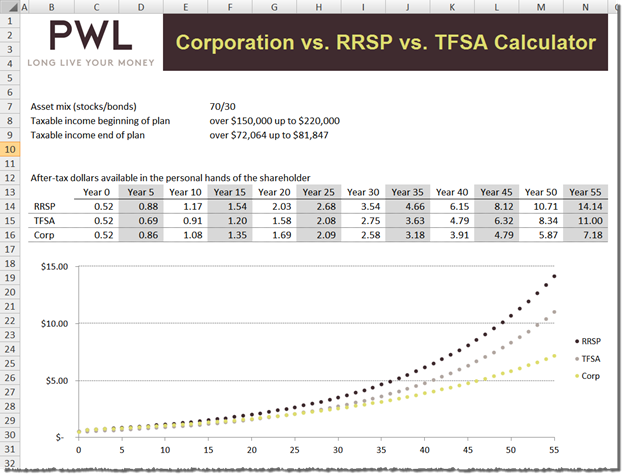

Our broad conclusions were that the RRSP must not be overlooked as a financial planning tool for incorporated individuals that have RRSP room, and the TFSA should definitely be considered by incorporated individuals in cases where the time horizon is very long.

These issues are discussed in more detail in our recent whitepaper, A Taxing Decision. Similar analysis can be run for varying inputs (asset mix, beginning and ending tax rates) using the tool, seen below, that we have made available on our website:

Note that to maximize the $10,000 annual TFSA limit, the individual would need to start with $19,193.86 of excess earnings in the corporation at the assumed* tax rates in Ontario in 2015.

*The examples discussed consider an individual with income between $150,000 and $220,000 in Ontario in 2015.

Benjamin Felix is an Investment Advisor with PWL Capital in Ottawa. He completed an MBA in Financial Management from Carleton University in 2013, and is a 2016 Level III Candidate in the CFA Program. He helps Canadians make smart financial decisions, and manages their portfolios.

The shift to a mix of salary and dividends has become an effective choice for shareholders as noted. The salary component also increases your future CPP entitlement.