On April 12, 2015, I wrote my first post on this blog.

A decade of writing.

441 articles.

1 Million Words.

Wow.

It’s been a heckuva ride. I’m in awe that over 16,000 of you subscribe to my blog and read what I write (a sincere “Thank You!” to all of you). It’s an honor, and I take it seriously. In that very first post, I wrote the following:

“This is the story of my journey, told in The Present before it becomes The Past.”

I’ve always liked that sentence, and it’s become one of my goals with this blog. To share my journey, as I’m living it, with the hope that sharing my experiences will help others achieve a great retirement.

At this point in my journey, I feel I’ve accomplished that goal.

As I seek to continually experiment with my retirement lifestyle, I challenge myself to embrace the freedom these years offer. Sometimes it’s hard, and today is one of those days. As that journey has evolved, it’s reached the point where it’s led to a major decision for this blog.

That decision?

I’m retiring from full-time blogging.

But…I’m getting ahead of myself. To gain insight into my decision and what it means for this blog, read on…

I’ve known a lot of bloggers over the past decade, most of whom have faded away. That’s not a surprise, given that 80% of blogs fail to survive beyond 18 months.

They just … disappear.

One day, you’re reading their stuff, and a few months later, you realize you haven’t seen anything from them in a while. A year later, they’re all but forgotten.

I’m taking a different approach

As always, I’m being transparent about this phase of my journey, and I’d rather tell you what I’m thinking than have you wonder where I’ve gone. This is my Present, before it becomes my Past.

After 10 years of diligent writing, it’s time to shift gears. I still enjoy writing, but it’s becoming more of an obligation than the true joy it’s been in the past. With over 440 articles in my archives, it’s harder to find fresh topics to challenge my mind. I think less and less about potential topics, a sharp contrast to the earlier years of writing when ideas were constantly flooding my mind.

It’s time to move on

I’ve always encouraged you to remember that Retirement Is Like A Game of Poker, and challenged you to constantly improve the cards you’re holding. If a card is getting stale, don’t hesitate to exchange it for a new card from the deck.

I’d be a hypocrite if I didn’t apply the same advice. The blogging card has gotten a bit stale, so I’m shuffling the deck and putting the cards down for a while.

I hope you’re doing the same.

Never stop experimenting.

Never stop improving your hand

The Future of The Retirement Manifesto

The good news is, this blog isn’t going anywhere. I have no intention of selling it, and I plan on keeping it online well into the future. I’ll still write when the urge strikes.

The thing that will change is the frequency of my writing.

After all, I’m retiring from full-time blogging. 😉

I don’t know exactly what that means yet, but I’m going to explore it for a while to see where it leads. I’ve been writing about retirement for a long time, perhaps I’ll use this platform to share thoughts on other topics in the future. Most likely, I’ll follow the path that Mr. Money Mustache and JL Collins have taken, and write when I feel I have something worthwhile to say. They both only write a few times a year, but I still read every word. I hope my readers will do the same for me.

Stay tuned (and please don’t unsubscribe)…

I’m getting busier with other activities that I enjoy, and the blogging card has become more intrusive. I seldom find time to sit at my keyboard, and I’m fine with that. I prefer to be out… .. Continue Reading…

Over the past year, Canadian seniors have faced rising inflation, high interest rates, and ongoing economic uncertainty, all of which are reshaping what retirement looks and feels like in Canada.

Retirement was once viewed as a time of ease and stability; instead, for many, it now feels like a constant calculation of trade-offs and tough decisions. Recent data paints an unfortunate picture, as retirement confidence is declining fast. Only 36% of Canadians feel confident in their ability to stay financially stable in retirement and just 7% feel very confident, while 27% are not confident at all.

This isn’t about long-term planning gone wrong: it’s about the real-time impacts of economic conditions that have changed dramatically over the last few years. Inflation has outpaced income, and daily essentials like food, utilities, medical care and housing are up nearly 30% over the past three years. However, there are ways to regain control.

A Shifting Retirement Reality

Many older Canadians are now exploring alternative ways to stretch their resources. For some, that has even meant returning to work: nearly half (46%) of Canadian homeowners aged 55+ are considering part-time jobs to make ends meet with rising living costs. For others, it means delaying retirement altogether: 67% say they’re concerned their savings won’t sustain the quality of life they had envisioned.

Meanwhile, traditional supports like the Canada Pension Plan, Old Age Security, and personal savings no longer offer the security they once did, especially since many seniors are financially supporting family members. According to another survey, 1 in 3 Canadian grandparents are financially supporting their children or grandchildren, with 53% saying that support has increased over the last two years. With 65% acknowledging that assistance impacts their own retirement savings, it’s clear that seniors are carrying more financial weight than ever.

Taking back Control

In response, seniors are taking steps to regain their financial control. One critical first step is getting a clear understanding of the full financial picture: knowing what money is coming in and what is going out. By distinguishing between “wants” and “needs,” retirees can prioritize essentials like housing, food, healthcare, and look for opportunities to cut back where possible.

Exploring New Solutions

In a financial landscape that is ever-changing, more and more seniors are open to innovative solutions that may not have been part of their initial retirement plans. Three-quarters of Canadian seniors own the homes they live in, and most entered the housing market decades ago. With years of sustained low interest rates and population growth that has outstripped new housing supply, home prices have tripled nationwide in the last 20 years (and more than that in many markets). Continue Reading…

Looking for creative ways to generate income beyond the typical 9-to-5? In this article, 16 financially independent people share real-life stories of unconventional income streams they’ve successfully leveraged on their path to financial freedom.

From flipping niche collectibles online to building mobile apps and renting out specialized equipment, these insights offer practical advice and inspiration for anyone seeking to diversify their income and think outside the box.

Flip Niche Collectibles Online

Flip Expired Domains for Profit

Develop Useful Mobile Applications

Create Online Courses for Therapists

Offer Ice as a Subscription Service

Provide Emergency Phone Consultations

Monetize Drone Inspections Separately

Acquire and Improve Underperforming Blogs

Sell Niche Digital Products Online

Rent Out Specialized Equipment

Sell Stock Photos Online

Invest in Income-Generating Websites

License Valuable Industry Data

List Properties on Airbnb

Publish Ebooks on Amazon Kindle

Embrace Unexpected Opportunities

1.) Flip Niche Collectibles Online

Exploring unconventional income streams is like finding hidden treasures; it’s about spotting opportunities in unexpected places. One such stream I’ve tapped into is buying and flipping niche collectibles sourced from online marketplaces. Initially, I stumbled upon this while pursuing a personal hobby. Seeing the high demand and low supply for certain vintage items, I realized there was potential to turn this into a lucrative side business. The key here is to develop a keen eye for what has high resale value and stay informed about the trends within that niche.

For anyone interested in pursuing this avenue, I’d recommend starting with a category you’re passionate about, as this naturally increases your understanding and interest in collecting items.

Next, it’s crucial to learn the best places for acquiring collectibles at lower prices, whether that’s thrift stores, estate sales, or online auctions. Regularly engaging with communities and forums can also provide insights and opportunities to buy and sell. Ultimately, while this might seem like just a fun hobby, with the right approach, it can become a significant part of achieving Financial Independence.

It’s essential to approach this with a mixture of enthusiasm and caution; start small to understand the market dynamics before fully diving in. Balancing patience with smart, informed decisions can open up an exciting path towards not just financial goals, but also personal fulfillment in seeing your collections bring joy to others as well. — Alex Cornici, Writer, The Traveler

2.) Flip Expired Domains for Profit

One of the most unconventional income streams I leveraged on my path to Financial Independence was expired domain flipping: buying undervalued domain names with strong SEO authority and reselling them at a premium.

A few years ago, I was searching for a domain for a side project when I stumbled upon an auction site selling expired domains. Out of curiosity, I bought one for $15 that had thousands of quality backlinks from reputable sites. Within two weeks, I flipped it to a niche blogger for $750: a 4,900% return on investment. That’s when I realized there was a hidden market for domains that still carried strong SEO value.

After that first success, I developed a system to find, evaluate, and flip domains efficiently:

Finding High-Value Expired Domains – I used tools like Ahrefs, SpamZilla, and ExpiredDomains.net to search for domains with strong backlink profiles.

Assessing SEO Value – Instead of buying any expired domain, I looked for high-authority links, clean backlink profiles, and past relevance to industries in demand (finance, health, tech).

Selling to the Right Buyers – I joined Facebook groups, niche forums, and SEO communities, where bloggers and businesses actively sought pre-aged domains to boost rankings.

One of my best flips was a tech-focused domain I purchased for $120. It had backlinks from major publications and had been a trusted resource in the industry. Within a month, I sold it to a startup for $5,000: because for them, the built-in SEO authority saved months of ranking effort.

If you want to get into domain flipping:

Start small – Buy one or two domains and learn the process before scaling.

Focus on SEO value, not just catchy names – A strong backlink profile is what makes an expired domain valuable.

Network in the right places – Many buyers are in SEO communities, niche blogs, and online business groups.

Expired domain flipping isn’t about luck: it’s about recognizing digital real estate opportunities before others do. If you can spot value where others see nothing, you can build a profitable and scalable income stream. — Ahmed Yousuf, Financial Author & SEO Expert Manager, CoinTime

3.) Develop useful Mobile Applications

I earn well as a CTO, but I want that financial security where I do not have to depend on a single income stream. That is why I started developing mobile applications as an additional source of revenue. Since I am already a software developer, shifting into mobile apps was a natural transition. The technical foundation was there, and I saw an opportunity to build something outside of my daily work.

I discovered this opportunity from a colleague of mine who had been making passive income through mobile apps for years. He built simple apps that solved everyday problems and made money through ads and subscriptions. That conversation changed how I looked at mobile development. I decided to start with something I understood well. My first app was an expense tracker designed for freelancers who struggle with budgeting and tax prep. I kept it simple, focusing on an intuitive interface and automation features. After launching it in the app stores, I introduced a premium version with added features, which turned it into a passive income stream. I earn about $5,000 to $7,000 per month from this app alone, and that number grows as more users download and subscribe.

For anyone interested in pursuing this, the first thing that you need to do is find a common problem that does not have a convenient solution yet. Successful apps do not have to be groundbreaking. They just need to be useful. Start small, validate your idea with a test audience, and make the experience smooth and reliable. Mobile app development is one of the few income streams where effort upfront can turn into long-term financial stability without constantly trading time for money. — Paul DeMott, Chief Technology Officer, Helium SEO

4.) Create Online Courses for Therapists

As a Licensed Clinical Social Worker and digital nomad, one unconventional income stream I’ve leveraged is the creation of online courses and communities for therapists. It started with “DIY Insurance Billing for Private Practice,” which has attracted over 950 clinicians. This course was born out of my own struggles with insurance billing. By changing my learning into a resource, I’ve tapped into an overlooked need among therapists seeking autonomy and financial stability.

In addition, I founded the “Bill Like A Boss” community, offering a support network and a directory for therapists to find billers and virtual assistants. This not only provided value but established me as a thought leader in a niche market. By addressing this specific pain point, the model created additional revenue while enhancing client satisfaction and loyalty.

For those interested in a similar path, identify a gap in your professional area where you possess unique insights or skills. Develop a resource or service that addresses this need, and build a community around it. Emphasize practical support and collaboration to create a product or service that stands out. — Kym Tolson, Therapist Coach, The Traveling Therapist

5.) Offer Ice as a Subscription Service

One unconventional income stream I’ve successfully leveraged is the “as-a-service” business model, specifically in the ice equipment space. Most businesses traditionally buy or lease ice machines, dealing with maintenance, repairs, and eventual replacements. We flipped the script by offering ice as a subscription service-turning what used to be a hassle into a predictable, all-inclusive solution for businesses. Instead of making a significant upfront investment, customers pay a monthly fee for equipment, maintenance, and even backup ice if needed. This model creates steady, recurring revenue while eliminating customers’ most significant pain points.

I discovered this opportunity by recognizing an overlooked challenge in the food service and hospitality industries. Ice machines are essential but notoriously unreliable, and when they break down, it disrupts business. I saw how companies were stuck in a cycle of costly repairs or expensive replacements. We removed customers’ financial and operational headaches by shifting from ownership to service while building a long-term, scalable revenue stream.

For others looking to pursue unconventional income streams, my advice is to rethink how everyday products or services are delivered. Find something businesses or consumers rely on but don’t enjoy managing, then explore how a subscription or managed-service approach could make their lives easier. Stability, convenience, and predictability are powerful selling points. Look for inefficiencies, talk to customers, and see where to add value. Often, the best opportunities aren’t about reinventing the wheel but making it roll more smoothly. — Travis Rieken, Sr. Director of Product Management, Easy Ice

6.) Provide Emergency Phone Consultations

Plumbing work usually brings to mind hands-on labor, but there’s another way to earn: charging for emergency phone consultations. Plenty of homeowners panic over a small leak or a backed-up sink, and sometimes all they need is guidance rather than an immediate service call. I set up a system where customers could pay a flat $50 fee for a quick troubleshooting session, helping them avoid unnecessary expenses while making sure my time was compensated. This worked well for after-hours calls, since many people preferred a lower-cost solution instead of paying $200+ for an emergency visit. Over time, this turned into a consistent side income without extra travel or physical labor.

The idea came naturally after seeing how often customers called with simple problems. I figured if I was already answering questions, I might as well make it an official service. For anyone considering a similar approach, start by identifying where your expertise could provide quick, high-value solutions. Setting up a dedicated phone line or online booking system makes it easy, and promoting it through social media or existing clients can bring in steady business. Turns out, a small shift in how you offer services can add thousands to your income each year. — Caleb John, Director, Exceed Plumbing

7.) Monetize Drone Inspections Separately

Drones were originally just a tool for our roofing business, but it didn’t take long to see another opportunity. Homeowners, insurance companies, and real estate agents needed high-resolution roof inspections even when they weren’t planning repairs. So, we started offering drone-based reports as a separate service, charging $150 per scan. This turned into a profitable source of side income, especially since our AI analysis provided insights that traditional inspections didn’t. Given that a single drone could handle up to 10 inspections per day, this quickly added thousands in extra revenue without major operating costs.

The idea came after noticing that not every roof inspection led to a job, but the demand for assessments was still there. Instead of only using drones for internal purposes, we turned them into a paid service. For those in tech-driven industries, there’s often a way to take existing tools and monetize them separately. Sometimes, the things that support your main business can bring in just as much revenue when positioned as independent services. — Nathan Mathews, CEO and Founder, Roofer

8.) Acquire and Improve Underperforming Blogs

One unconventional income stream that worked surprisingly well for me was acquiring underperforming blogs, improving their content and SEO, and turning them into revenue-generating assets. Most people think of websites as businesses that require years to build, but I realized that buying neglected blogs with decent domain authority and traffic potential was a faster way to scale.

I discovered this by accident. I was deep into content marketing, and while working with clients, I noticed how many businesses let their blogs stagnate. Some had strong backlinks and history but were mismanaged or abandoned. So I started making offers, acquiring them for relatively minor costs, and applying the exact strategies I used for clients: cleaning up the content, fixing technical SEO issues, and creating a long-term content plan. Within months, traffic (and revenue) would grow through ad monetization, affiliate marketing, or even reselling the blog for a profit.

Anyone interested in this should start small. Look for blogs in niches you understand, ideally with decent backlink profiles and some organic traffic. Many are run by hobbyists who’ve lost interest so that you can negotiate good deals. But don’t just buy and hope; have a clear plan to improve the site. SEO, fresh content, and proper monetization can quickly turn a struggling blog into a valuable asset.

This strategy isn’t discussed enough, but it’s a scalable way to create income streams without starting from scratch. Knowing how to spot potential, move quickly, and execute effectively is key. — James Parsons, CEO, Content Powered

9.) Sell Niche Digital Products Online

Selling niche digital products is an unconventional yet highly effective income stream that provides scalability and passive revenue with minimal ongoing effort. Unlike content-driven monetization strategies that require continuous engagement, digital products — such as financial templates, investment research, and specialized e-books — offer a one-time creation model with unlimited sales potential. This approach is particularly useful for professionals who can leverage their expertise to create high-value, ready-made solutions for a specific audience.

My journey into digital products began when I realized that many individuals and small business owners struggled with financial planning and investment tracking. I had developed budget templates, financial calculators, and investment worksheets for personal use, but after refining them for broader usability, I started selling them through platforms like Gumroad, Etsy, and Sellfy. As demand grew, I optimized listings, bundled complementary products, and used SEO-driven marketing to reach more buyers, turning a side project into a steady revenue stream. Continue Reading…

No one expects a monetary crisis to strike until it does. Some events that might throw you into a tizzy include losing your job, a pet getting ill and needing emergency veterinary services or the family vehicle breaking down.

To stick to financial goals, you must have a plan for when the current one falls to pieces. Creating a budget that allows you to survive a sudden catastrophe while saving for a home, travel or retirement is the secret ingredient to keeping the nest egg you need.

Amid the Storm: Identify and Prioritize Essential Expenses

An annual emergency savings report by Bankrate, YouGov and SSRS found that 59% of Americans are not comfortable with their emergency savings. For millions of people struggling paycheck to paycheck, anything outside their normal costs spells trouble.

The first thing to do when you experience fewer funds than bills coming in is to assess where you are and how much money you need to survive.

Identify Needs versus Wants

Although your favorite treat from the grocery store may seem like a need, you can likely find something less expensive to fuel your body. Some examples of needs include:

Shelter

Food

Heating and cooling

Once you have a list of the things you can’t live without, you’ll be better able to assess your priorities. In the short term, calling creditors or subscription services to pause payments or end plans can free up enough money to get through the predicament or assess how much money you need now.

Renegotiate Bills

The next step is to call each company to see what flexibility you have. For example, you need utilities to cook, heat your home and use the lights. Many local utility companies will put you on a payment plan so the bill remains the same around the calendar year rather than increasing exponentially during extreme weather.

For credit cards or subscriptions, explain your financial crisis and ask how to reduce monthly payments. Remember that delaying them may increase the total interest paid on the debt, so only use this technique to survive a short-term spending mess.

Cut to the Bare Bones

If you lose your income or have an unexpected expense, you may need to slash spending even more. Look to local resources for help. Food banks can provide sustenance when you lack grocery funds. Talk to your local county, township or public trustee about help with power bills and other resources in your area.

3 things to do to prepare for Financial Emergencies and Unexpected Expenditures

Life is filled with surprise charges. One way to plan for any crisis is to budget for it now. Weathering the next monetary tsunami will feel more like jogging up a hill than crawling up a steep mountain when you’re prepared. Here are some things you can do to be ready:

Create Multiple Streams of Income

Prepare for extra expenses like medical emergencies or the added costs of parenthood by finding ways to bring in more income. If the raises at work are lower than inflation, you can pick up a side hustle and join the gig economy to cover emergency funding.

In addition to diversifying your income sources, you can receive education to become eligible for higher-paying roles at work. Get an online certification, take a course through the local community college or enter management training through the workplace.

Add apps that earn you money for doing things like walking, taking surveys or buying things online. Look for creative ways to bring in extra cash, such as selling art you create or selling used items. Continue Reading…

Canadians in retirement, or those nearing retirement, are faced with unique challenges in the present-day market. Interest rates have moved up from their historic lows since 2022. The benchmark rate for the Bank of Canada (BoC) reached its zenith of 5.00% in July 2023. Economic headwinds forced the hand of the BoC in 2024 and 2025. The benchmark rate now stands at 2.75%, with more rate cuts expected before the end of the year. (The BOC stood pat on April 16th).

This downward trend for interest rates means that investors who want a secure investment while outpacing inflation may have to look beyond GICs and other fixed-income products in this changing climate. Market volatility is another headwind investors are now contending with, spurred on by a new and aggressive U.S. administration.

There was enthusiasm surrounding the broader economy and the stock market coming into 2025. The previous GOP administration cultivated a reputation as a market-friendly one in the late 2010s. That momentum ground to a halt due to the COVID-19 pandemic, but the perception of a market-friendly GOP largely remained.

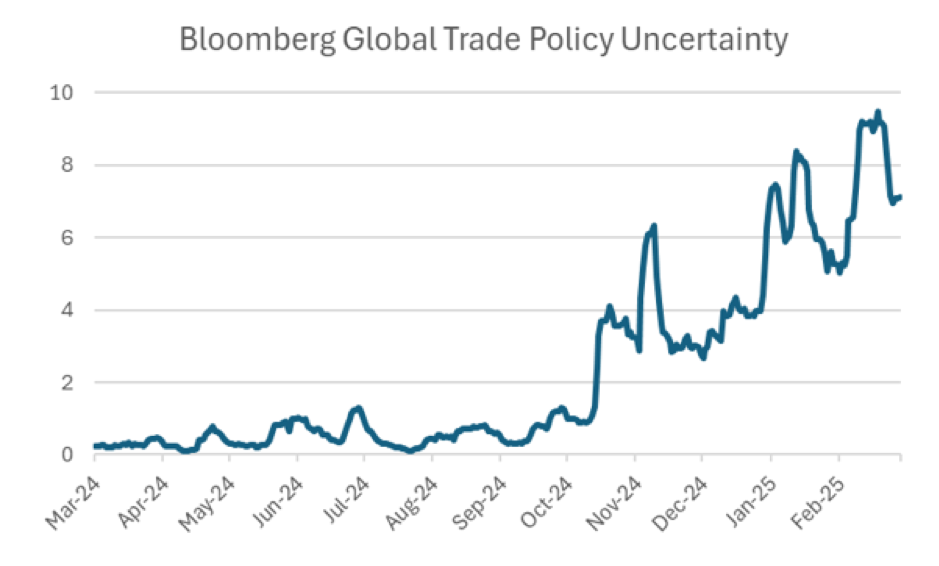

Investor outlook has soured in the late winter and early spring, in large part due to the uncertainty surrounding U.S. government policy, particularly when it comes to tariffs.

Source: American Association of Individual Investors, Bloomberg, Harvest ETFs. As of March 21, 2025.

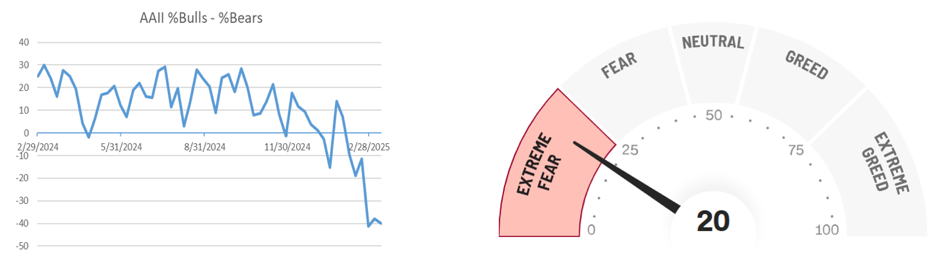

This uncertainty has resulted in elevated levels of market volatility. Some names have suffered retracements of 50% or more over the past two months. This market is unique in that the sell-off was not triggered by one significant catalyst. Indeed, it is lingering trade policy uncertainty that is fuelling negative sentiment.

Source: American Association of Individual Investors, CNN (Fear and Greed Index). As of March 20, 2025.

The S&P 500 has dropped 8% in the year-to-date period as of close on Friday, April 10, 2025. A research note from Vanguard recently speculated that volatility was likely to remain due to factors like policy uncertainty, disruptive currents in the economy like artificial intelligence development, and the shifting policy of the Federal Reserve.

Demand for Low Volatility products has increased in this environment. These ETFs offer Canadian retirees a pure low volatility play with exposure to 100% Canadian equities. Moreover, we have introduced Harvest’s trusted option writing strategy to the second Low Volatility ETF. It aims to lower portfolio volatility while generating high monthly cash distributions.

Harvest Low Volatility ETFs: A smoother Investment Experience

Harvest’s new Low Volatility ETF suite could be appealing to defensive and long-term investors. This approach to equity investing is factor-based, disciplined, outcome-oriented, is designed to mitigate risk, as well as provide long-term growth. Moreover, the suite includes a high-income solution that generates monthly cash distributions through an active covered call writing strategy. Continue Reading…