Getting a mortgage renewal letter seems pretty straightforward. Your lender gives you a new rate and payment, you sign it, and you’re done.

At least that’s how it looks.

What I started wondering was: how does the average homeowner actually know if the offer they’re getting is any good?

I’m not a mortgage broker or financial adviser. I’m just someone who started digging into this and realized it’s surprisingly difficult to get a simple answer. You can search mortgage rates online in about 30 seconds. The problem is that the rate you find isn’t necessarily comparable to the renewal offer sitting in front of you.

There can be different conditions, different mortgage types, different equity requirements and all sorts of other details attached to an advertised rate. So if your bank offers you 4.89% and you find 4.24% online, that doesn’t automatically mean your bank is ripping you off.

But I’d certainly want to know why there’s a difference.

The rate is a starting point

Obviously the interest rate matters.

A difference that looks fairly small on paper can make a noticeable difference to your payment, especially with a large mortgage balance.

But there are other things worth looking at too.

What are the prepayment privileges? What happens if you need to break the mortgage early? Is it portable? Are there fees or restrictions? And if another lender has a lower rate, what would it actually cost and involve to move the mortgage?

Those details aren’t nearly as exciting as finding a lower rate, but they can matter.

There’s nothing wrong with staying with your bank

I think this part sometimes gets lost.

Switching lenders isn’t automatically the smart move. Continue Reading…

How American and Canadian investors can reduce capital gains taxes after decades of buying and holding.

AlainGuilot.com via Grok

By Alain Guillot

Special to Financial Independence Hub

Buying a broad-market ETF and holding it for decades is one of the simplest ways to build wealth.

You buy an ETF like the Vanguard S&P 500 ETF (VOO) for U.S. investors or the iShares S&P/TSX 60 Index ETF (XIU) for Canadian investors. You reinvest the dividends, ignore the daily market noise and continue adding money whenever you can.

Twenty years later, the strategy has worked beautifully.

But now you have a new problem: how do you reduce capital gains tax when selling an ETF that has increased enormously in value?

This is the strange punishment for being a successful long-term investor.

You followed the advice to buy and hold. You resisted panic selling. You avoided speculation and unnecessary trading.

Now your portfolio may contain hundreds of thousands of dollars in unrealized gains.

Selling a large amount in one year could create a substantial tax bill. It could also push your income into a higher tax bracket and affect income-tested benefits.

This is not merely a theoretical question for me. I have accumulated VOO and XIU for many years, and I know that selling a large portion at once could create a painful tax expense.

Fortunately, selling everything in one year is not the only option.

First, Understand the Capital Gains Problem

Suppose you invested $200,000 in VOO over many years.

Your investment is now worth $700,000.

Your unrealized capital gain is approximately:

$700,000 market value − $200,000 cost = $500,000 gain

You do not owe capital gains tax simply because VOO increased in value.

The tax is generally triggered when you sell or otherwise dispose of the investment.

That means you have some control over when the gain is realized.

The central question is not:

How can I avoid paying any tax?

A better question is:

How can I realize this gain gradually and pay the lowest reasonable amount of tax over my lifetime?

That change in perspective is important.

Reduce Capital Gains Tax by Avoiding One Giant Sale

The worst approach may be to sell the entire position without first calculating the consequences.

A large sale could concentrate decades of gains into a single tax year.

In both Canada and the United States, capital gains interact with the investor’s other income. Realizing more gains can bump you up to a higher tax braket and thus you will pay a higher tax rate.

A more efficient strategy is often to sell your ETF gradually.

For example, an investor could sell enough each year to cover:

Annual living expenses

Planned travel

Major purchases

Charitable donations

Portfolio rebalancing

Instead of realizing a $500,000 gain in one year, the investor might spread the gain over 10, 15 or 20 years.

This does not eliminate the tax.

It gives the investor more control over the rate and timing and hi might be taxed in a lower tax bracket.

Strategy 1: Sell more during Low-income Years

Some years are naturally better than others for realizing capital gains.

Good opportunities may arise:

After retirement but before pensions begin

Before collecting Social Security or government benefits

Before mandatory retirement-account withdrawals

During a sabbatical or period of reduced employment

In a year with large deductions

In a year when business income is unusually low

These lower-income years can create room to realize gains at a more favourable rate.

For American investors

The United States applies special federal tax rates to long-term capital gains.

Depending on taxable income, some long-term capital gains may fall into the 0% federal capital gains bracket. Higher-income investors generally face 15% or 20% federal rates, and some may also owe the 3.8% net investment income tax. State taxes may apply as well.

This creates a powerful planning opportunity.

An American investor with unusually low taxable income may sell some VOO, realize a long-term gain and potentially pay no federal capital gains tax on part of that gain.

The investor can then buy VOO again.

The newly purchased shares receive a higher cost basis, reducing a future taxable gain.

For Canadian investors

Canada does not have a special 0% capital gains bracket comparable to the American system.

Instead, only a portion of a capital gain is included in taxable income. The proposed increase in Canada’s capital gains inclusion rate was cancelled, leaving the one-half inclusion system in place.

If a Canadian investor realizes a $20,000 capital gain, $10,000 is generally included in taxable income under the one-half inclusion rate.

The final tax depends on the investor’s federal and provincial marginal tax rates.

A Canadian investor with little other income may therefore realize gains at a relatively modest tax cost. The investor can repurchase their ETF immediately, increasing the adjusted cost base.

This practice is known as capital gain harvesting.

Strategy 2: Harvest Capital Gains every year

Most investors have heard about tax-loss harvesting.

Capital gain harvesting receives far less attention.

Here is how it works:

Estimate your taxable income for the year.

Calculate how much additional capital gain you can realize without entering an undesirable tax bracket.

Sell enough of your ETF to realize that gain.

Repurchase the same ETF inmediately after selling it.

Record the transaction and update the cost basis.

The investor remains invested while gradually increasing the tax cost of the portfolio.

Over many years, this can reduce the unrealized gain that remains in the account. I use this strategy every year. I sell a portion of my investments, realize some capital gains, and buy the same investment inmediately after selling it.

Can you buy the same ETF back immediately?

Yes, when you sold it for a gain.

The American wash-sale rule and the Canadian superficial-loss rule are designed to restrict the recognition of losses when substantially identical securities are quickly repurchased.

They do not generally prevent an investor from repurchasing an investment immediately after realizing a gain.

Capital gain harvesting can therefore be completed without remaining out of the market for 30 days.

The disadvantage is that you are paying some tax earlier than necessary. As a citizen of this wonderful country, I don’t mind paying some taxes on my gains, as long as those taxes are not exessive and feel as a punishment for my success.

Money paid in tax today can no longer remain invested and compound.

The strategy is most attractive when the current tax rate is lower than the rate you reasonably expect to face later.

Strategy 3: Use Capital Losses to Offset your ETF Gains

A diversified portfolio may contain investments that have declined in value.

Selling one of those investments creates a capital loss that may offset part of the gain realized from selling your ETF. This strategy is called Tax-loss harvesting.

For example:

Gain from selling VOO: $30,000

Loss from selling another investment: $12,000

Net capital gain: $18,000

This allows the investor to reduce the VOO position while limiting the immediate tax bill.

United States

American investors can use capital losses against capital gains.

When losses exceed gains, a limited amount may generally be deducted against other income, with unused losses carried forward to later years.

The wash-sale rule must be considered before repurchasing the losing investment.

Canada

Canadian net capital losses can generally be used against taxable capital gains.

Unused net capital losses may normally be carried back as far as three years or carried forward to future years.

Canada’s superficial-loss rule may deny an immediate loss when the investor—or an affiliated person—buys the same or identical property during the restricted period and still owns it 30 days after the sale.

Again, this rule matters for losses, not gains.

Strategy 4: Donate your ETF instead of Cash

Investors who regularly support charities should consider donating appreciated ETF shares directly.

This can be much more tax-efficient than selling your ETF and donating cash.

For American investors

An American investor who donates qualifying appreciated securities held for more than one year may generally avoid recognizing the embedded capital gain.

The investor may also qualify for a charitable deduction, subject to deduction limits, documentation requirements and whether the investor itemizes deductions.

The charity receives the shares and can sell them without creating a capital gains tax bill for the donor.

Instead of donating $10,000 in cash, the investor could transfer $10,000 of his long held ETF containing a large unrealized gain.

The investor keeps the cash and removes some of the portfolio’s oldest, lowest-cost shares.

For Canadian investors

Canada also offers favourable treatment for direct donations of publicly traded securities to registered charities.

Qualifying donations can receive a zero capital-gains inclusion rate, while the donor may also receive a charitable donation tax credit.

The important word is directly.

Selling your ETF first and donating the cash may trigger the capital gain. Transferring the ETF shares directly to the charity may avoid it.

This is one of the few strategies that can genuinely eliminate the tax on part of an appreciated ETF position.

Of course, it only makes financial sense for money that the investor already intends to give to charity.

Strategy 5: Choose which Shares to Sell

This is one area where the American and Canadian systems differ significantly.

American investors may identify specific shares

An American investor may have purchased his favorite ETF at many different prices.

Some shares may have a cost basis of $150, while newer shares may have a basis of $500.

When selling, the investor may be able to instruct the broker to sell specific shares.

Selling the highest-cost shares first produces a smaller taxable gain.

For example:

Sale price: $600

Old share cost: $150

Gain: $450

Compared with:

Sale price: $600

Newer share cost: $500

Gain: $100

Specific-share identification can help American investors control which gains are realized. Proper instructions and records are essential. IRS guidance requires investors to maintain records supporting the basis of their investments.

Canadian investors use an average adjusted cost base

Canadian investors generally cannot select the highest-cost ETF shares and pretend those were the only units sold.

Identical securities are pooled together.

The investor must calculate the average adjusted cost base of all identical ETF units held in non-registered accounts. The gain on a sale is based on that average cost.

This makes accurate recordkeeping especially important.

Broker records may not always correctly combine ETF held across multiple Canadian taxable accounts.

Honestly I prefer the Canadian systeme of average adjusted cost much better. I have been making many different purchases during more than 10 years. It’s a headache to keep record of that small purchase I did of the XIU ETF 10 years ago.

Strategy 6: Keep Accurate Records

Before worrying about how to reduce capital gains tax, make sure the gain has been calculated correctly.

An incorrect cost basis can produce an unnecessarily large tax bill.

The records should include:

Every purchase

Reinvested distributions

Brokerage commissions

Stock splits

Transfers between brokers

Return-of-capital distributions

Previous sales

Currency conversions, when applicable

Special issue for Canadians holding U.S ETFs in U.S. dollars

U.S. ETF trades in U.S. dollars, but Canadian taxes must generally be calculated in Canadian dollars.

The purchase cost must be translated into Canadian dollars using the appropriate exchange rate at the time of purchase. The sale proceeds must also be translated using the relevant exchange rate at the time of sale.

A gain that appears to be modest in U.S. dollars may be larger in Canadian dollars if the Canadian dollar weakened during the holding period.

The CRA calculates gains by subtracting the adjusted cost base and selling expenses from the proceeds of disposition.

Investors who accumulated a U.S. ETF over 20 years may need to reconstruct many transactions.

That effort can be worthwhile.

Finding forgotten purchases, commissions or reinvested distributions may increase the adjusted cost base and reduce the taxable gain.

Strategy 7: Stop Reinvesting Dividends

An investor who is approaching retirement may not need to continue reinvesting every dividend from their ETF.

Instead, the cash distributions can be used for living expenses.

Within the article, there are a few ETFs I’ve considered to adjust our portfolio for AI success long-term:

Fund: Global X Artificial Intelligence & Technology ETF (NASDAQ: AIQ)” that ETF provides balanced diversification across the entire AI ecosystem, including hardware, software platforms, and foreign AI leaders. Top holdings frequently include giants like Nvidia, Broadcom, and Apple.

Beyond that article you can also consider Fund: TD Global Technology Leaders Index ETF (TSX: TEC) – with a lower MER and TEC is also heavily-traded in Canadian-dollars so this is a low-cost option for global tech.

Finally, you can stick with what I * used to own QQQ or a Canadian-listed ETF that clones it – those ETFs invest in the top-100 companies on the NASDAQ-100 index so it’s a very passive way to own tech and AI-related tech.

* I used to own QQQ but I sold all of it about a year ago now in favour of 1. portfolio simplicity and 2. Canadian-listed ETF investing. I’m better for it – since my two-fund Canadian-listed ETF solution is up about 12% combined YTD for almost 50% of my portfolio and we don’t need to worry about AI run-ups or bubbles anymore in doing so. We ride diversified returns…

Like Jon from the article, although in my early 50s vs. 70s, from where I sit I’m planted firmly in the retirement risk zone whereby the early retirement years need to be monitored carefully: which also implies to me no major portfolio overhauls either. Just some adjustments from time to time.

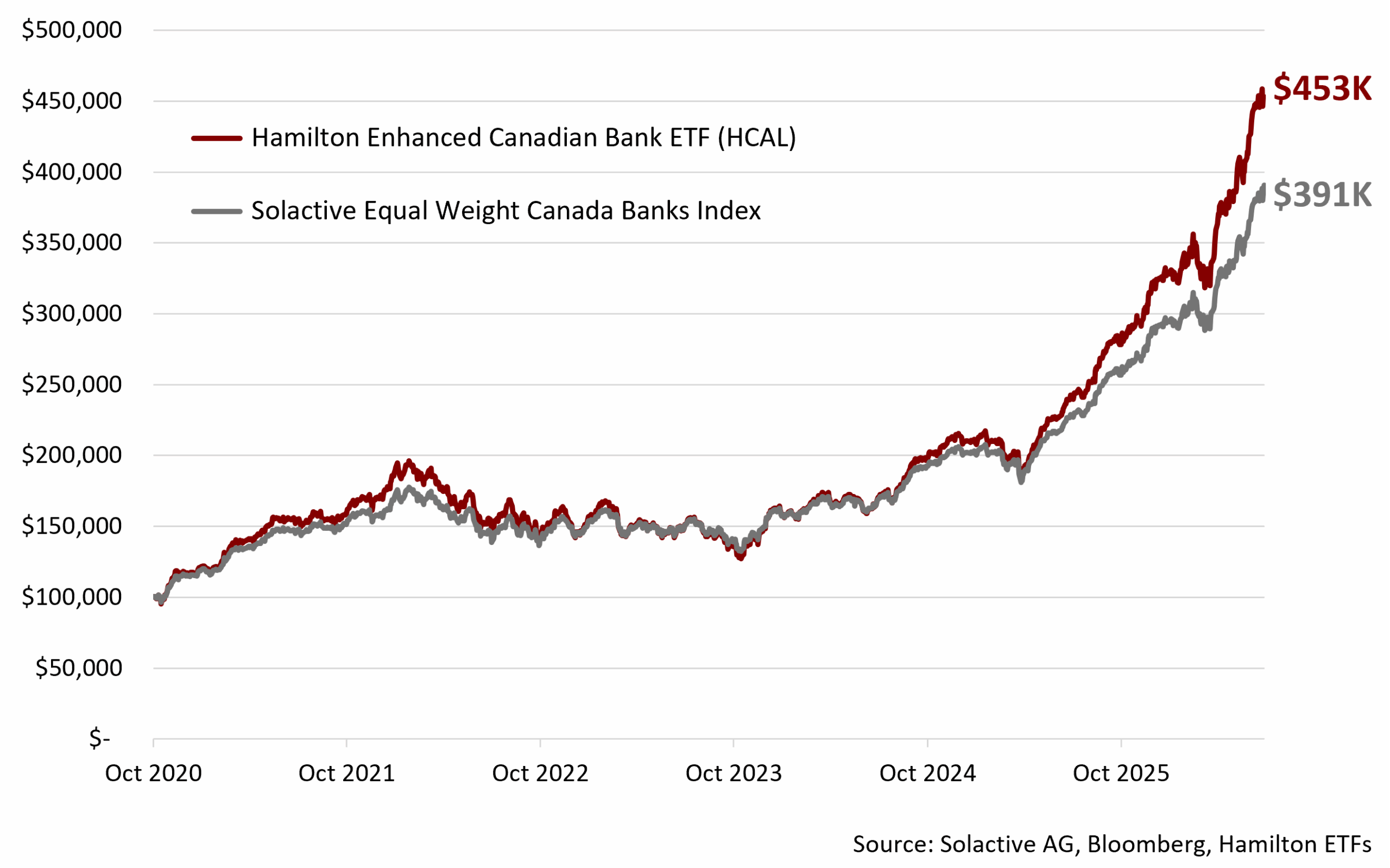

In May 2020, during the early days of the pandemic and while bank stocks were depressed, we presented a webcast entitled “Credit Cycle is Coming – What to Expect.”

During that webcast, we (correctly) predicted that during the expected downturn, the new loan loss accounting would deepen the credit cycle for the Canadian banks and importantly shorten its duration to 2-3 quarters (versus the historical duration of a credit cycle of 4-6 quarters).

Two quarters later, in October, we followed up with a presentation/webcast entitled “Canadian Banks: Cycle is (Basically) Over,” explaining why we believed the cycle was ending, and that the upside from earnings normalization was material.

Demonstrating our conviction, we launched HCAL: the Hamilton Enhanced Canadian Bank ETF, Canada’s first modestly levered ETF on October 14, 2020. We argued that its higher yield and growth potential relative to the Canadian banks created an excellent opportunity for long-term investors to take advantage of the looming recovery. We also noted that notwithstanding its modest leverage of 25%, its volatility profile was not meaningfully different than owning an individual Canadian bank stock[1].

In the year that followed, Canada’s Big Six bank stocks recovered much faster than the market anticipated, due to an improving macro environment and rapid normalization of earnings supported by large reserve releases. In 2021, HCAL rose more than 51%, outperforming the Solactive Equal Weight Canada Banks Index by over 20%[2].

HCAL’s success marked an important milestone in our growth and helped pioneer a new category in Canada, demonstrating that modest leverage, when applied thoughtfully to high-quality stocks and trusted sectors, could enhance long-term returns.

Since inception, HCAL has generated an annualized return to investors of 30.3%, with a higher yield and similar volatility profile to the Big Six Canadian banks (more below).

As a result, HCAL now has over $1 billion in assets under management (AUM), making it the seventh member of the Hamilton $1 billion-and-over club.

In Canada, Banking is King

Known for their consistent dividends and wide ownership, Canada’s Big Six banks are considered among the most reliable blue-chip companies in the country and the backbone of the economy and stock market.

Put simply, for every $100 you invest, you get approximately $125 exposure (net of financing costs), and this approach has delivered higher monthly income and higher long-term returns since HCAL’s inception when compared to the Canadian bank index, specifically the Solactive Equal Weight Canada Banks Index (“Canadian Bank Index”.)

Born out of inventive thinking during a time of uncertainty for the banking sector, HCAL has grown to more than $1 billion in assets under management and become an important part of Hamilton ETFs’ growth and story. Its success reflects our focus on developing thoughtful, differentiated investment solutions, which is key to the Hamilton ETFs ethos.

“As an ETF provider, you want to offer products that make your clients money, it can’t just be about inflows to you. We always ask: is this a good product? Does it add value and choice to investors?” said Executive Chairman and Co-Founder Robert Wessel.

Some of the factors that have made HCAL stand out:

Owning blue-chip Canadian banks: HCAL provides exposure to the Canadian banks, one of Canada’s most trusted sectors with an uncommonly long record of dividend sustainability.

Similar volatility to an individual Canadian bank stock: Since inception, the increase in volatility from the enhanced structure roughly offsets the decline in volatility from diversification. As a result, HCAL has had a volatility profile roughly equal to owning any single Canadian bank stock (see chart below).

The outcome?

HCAL has provided investors with strong returns over its 5-year track record. Since inception, it has provided investors with both a higher long-term return than the Big Six banks, at 30.3% annualized return (see table below) and higher yield with similar volatility to the Big Six Canadian banks.

Hamilton ETFs: Pioneers of Enhanced ETFs

Launched in October 2020, HCAL was Canada’s first “enhanced” ETF followed by the second, the Hamilton Enhanced Canadian Covered Call ETF (HDIV), which launched in July 2021. When creating HCAL, we chose 1.25x exposure, which we believe is a “Goldilocks” level of leverage, because our analysis and back-testing of the strategy suggested higher long-term return potential while maintaining a volatility profile similar to that of an individual Canadian bank stock[6]. Continue Reading…

Yes, I’m stuck in the middle with you

And I’m wondering what it is I should do

It’s so hard to keep this smile from my face

Losing control, yeah, I’m all over the place

Clowns to the left of me, Jokers to the right Here I am, stuck in the middle with you

Stuck in the Middle With You, by Stealers Wheel

Caught between the Rock of FOMO and the Fear of FOL

With the current bull market now into its fourth year and many global stock indices at or near record levels, investors could be forgiven for wondering how much upside there can be from here and when the party will end.

While almost nobody with whom I have spoken believes that a bear market is imminent, they are concerned that it is becoming more likely. Despite this increased wariness, people are also cognizant that running for the hills could entail foregoing considerable gains should markets continue their trajectory. They are trapped between the “rock” of FOMO (fear of missing out) and the “hard place” of FOL (fear of losses). Buffett best described this recurring dilemma in his statement:

“The line separating investment and speculation, which is never bright and clear, becomes blurred still further when most market participants have recently enjoyed triumphs. Nothing sedates rationality like large doses of effortless money. After a heady experience of that kind, normally sensible people drift into behavior akin to that of Cinderella at the ball. They know that overstaying the festivities — that is, continuing to speculate in companies that have gigantic valuations relative to the cash they are likely to generate in the future — will eventually bring on pumpkins and mice. But they nevertheless hate to miss a single minute of what is one helluva party. Therefore, the giddy participants all plan to leave just seconds before midnight. There’s a problem, though: They are dancing in a room in which the clocks have no hands.”

This month, I discuss whether the current bull market has reached a stage where it is something to be feared. To this end, I will ascertain whether it represents an outlier from a historical perspective with respect to its longevity, magnitude, and valuation. I will also discuss the catalysts that have brought an end to previous bull markets and whether any such “markers” are lurking in the shadows.

It’s not a Question of IF, but WHEN

As the following table illustrates, bear markets have hardly been uncommon.

I have no idea when the next bear market will arrive or how severe it will be. For what it’s worth, I don’t think anybody else does either. However, unless you believe that bear markets have become extinct, markets will continue to suffer periodic episodes of malaise. As the saying goes, “You don’t need to know when something will happen to know that it will.”

Looking for the Signs: Mapping the Present to the Past

From a purely statistical perspective, some measures suggest that the current bull market may have considerable life remaining. However, there are also some signs that have portended the demise of its predecessors.

In terms of length, the current runup in equities does not appear long in the tooth. As of the end of last month [June], it has been 1357 days since the end of 2022’s bear market in mid-October of 2022. By contrast, the average duration of bull markets since WWII has been 1905 days.

With respect to returns, the present bull market appears similarly unalarming, with the S&P 500 Index producing a total return of 123.2%, as compared to an average return of 177.4% for all previous bull markets in the postwar era. However, this average is heavily skewed by the bull run that included the late 1990s tech bubble, during which the index produced a total return of 582.1%. Once this extreme data point is removed, the average bull market return falls from 177.4% to a far more modest 140.6% that makes the current bull market appear considerably less youthful.

From a rate-of-appreciation perspective, the current bull run appears somewhat ahead of itself. In its 1357 days of existence, the S&P 500 Index has delivered a total return of 123.2%, as compared to an average return of 104.8% over the same period during the three previous bull markets. Only the post-global-financial-crisis bull run had a greater rate of ascendance, returning 125.4% over its initial 1357 days. However, when equities troughed in March 2009, the forward P/E ratio of the S&P 500 was approximately 11. Once investors became comfortable that the world was not collapsing, bargain basement prices and hyper-stimulative monetary policies served as rocket fuel for stock prices. In contrast, the current bull run began with a P/E ratio of over 16 and current rates are particularly accommodative, which makes this bull market’s pace of gains appear somewhat anomalous.

Perhaps the most striking feature of the U.S. market is its strength over an extended period. With the exception of the short-lived Covid Crash and the relatively shallow and short bear market of 2022, markets have been on a largely uninterrupted winning streak. Annualized returns over the past 10 years through the end of 2025 are 14.68%, as compared to an average of 10.97% for all rolling 10-year periods in the postwar era. In a worst-case scenario, reversion to the long-term mean would require a 44% decline, while a more benign path would necessitate subpar returns over an extended period.

Lots of Steak. But also, some Sizzle

Don’t get me wrong: if earnings growth had kept pace with stock prices over the past ten years, I would not be particularly concerned that stocks have gotten ahead of themselves. After all, it is widely understood that the S&P 500 Index has become increasingly dominated by a handful of mega cap tech stocks that have delivered phenomenal earnings growth. Continue Reading…