Once you achieve Financial Independence, you may choose to leave salaried employment but with decades of vibrant life ahead, it’s too soon to do nothing. The new stage of life between traditional employment and Full Retirement we call Victory Lap, or Victory Lap Retirement (also the title of a new book to be published in August 2016. You can pre-order now at VictoryLapRetirement.com). You may choose to start a business, go back to school or launch an Encore Act or Legacy Career. Perhaps you become a free agent, consultant, freelance writer or to change careers and re-enter the corporate world or government.

In May 2020, during the early days of the pandemic and while bank stocks were depressed, we presented a webcast entitled “Credit Cycle is Coming – What to Expect.”

During that webcast, we (correctly) predicted that during the expected downturn, the new loan loss accounting would deepen the credit cycle for the Canadian banks and importantly shorten its duration to 2-3 quarters (versus the historical duration of a credit cycle of 4-6 quarters).

Two quarters later, in October, we followed up with a presentation/webcast entitled “Canadian Banks: Cycle is (Basically) Over,” explaining why we believed the cycle was ending, and that the upside from earnings normalization was material.

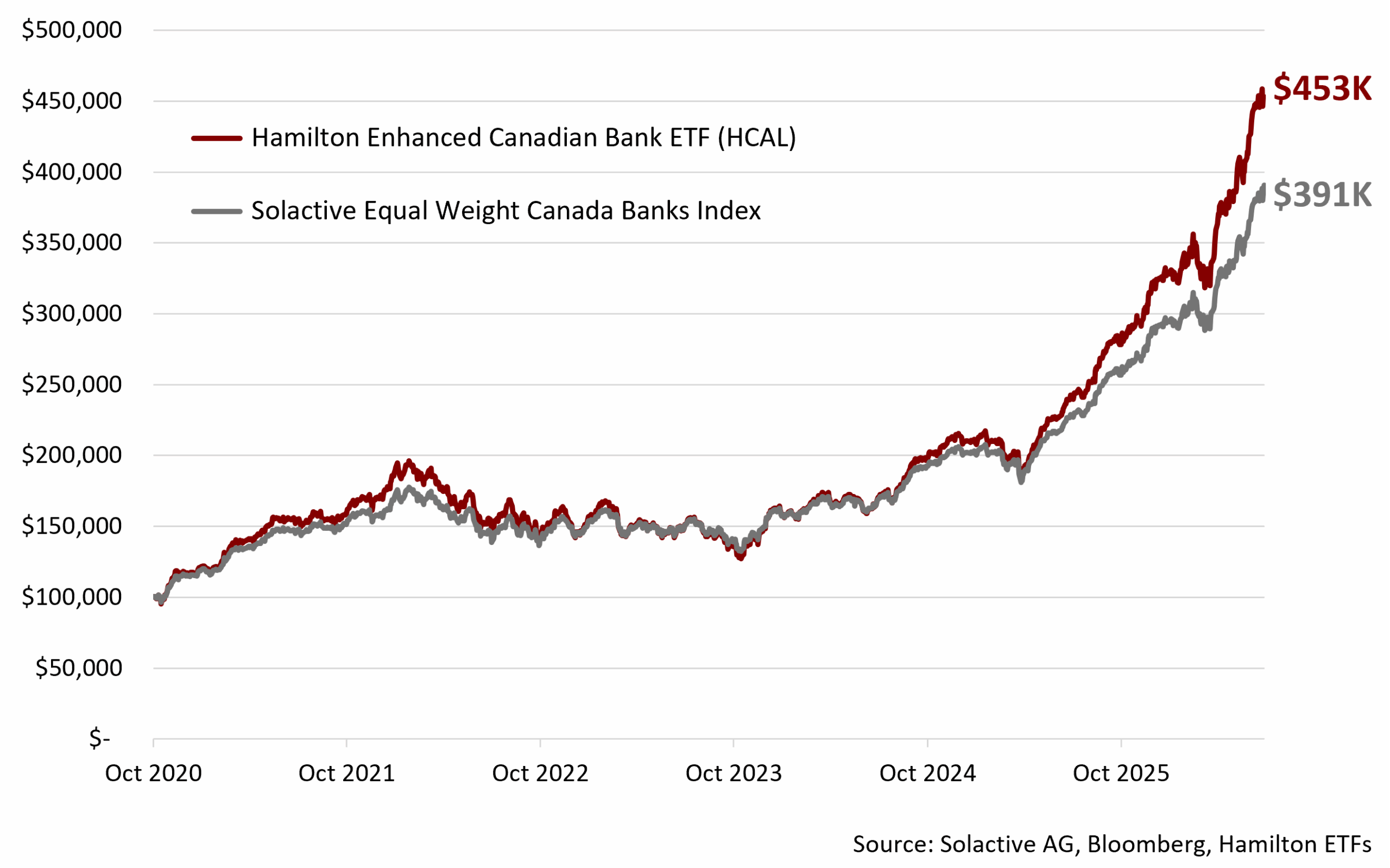

Demonstrating our conviction, we launched HCAL: the Hamilton Enhanced Canadian Bank ETF, Canada’s first modestly levered ETF on October 14, 2020. We argued that its higher yield and growth potential relative to the Canadian banks created an excellent opportunity for long-term investors to take advantage of the looming recovery. We also noted that notwithstanding its modest leverage of 25%, its volatility profile was not meaningfully different than owning an individual Canadian bank stock[1].

In the year that followed, Canada’s Big Six bank stocks recovered much faster than the market anticipated, due to an improving macro environment and rapid normalization of earnings supported by large reserve releases. In 2021, HCAL rose more than 51%, outperforming the Solactive Equal Weight Canada Banks Index by over 20%[2].

HCAL’s success marked an important milestone in our growth and helped pioneer a new category in Canada, demonstrating that modest leverage, when applied thoughtfully to high-quality stocks and trusted sectors, could enhance long-term returns.

Since inception, HCAL has generated an annualized return to investors of 30.3%, with a higher yield and similar volatility profile to the Big Six Canadian banks (more below).

As a result, HCAL now has over $1 billion in assets under management (AUM), making it the seventh member of the Hamilton $1 billion-and-over club.

In Canada, Banking is King

Known for their consistent dividends and wide ownership, Canada’s Big Six banks are considered among the most reliable blue-chip companies in the country and the backbone of the economy and stock market.

Put simply, for every $100 you invest, you get approximately $125 exposure (net of financing costs), and this approach has delivered higher monthly income and higher long-term returns since HCAL’s inception when compared to the Canadian bank index, specifically the Solactive Equal Weight Canada Banks Index (“Canadian Bank Index”.)

Born out of inventive thinking during a time of uncertainty for the banking sector, HCAL has grown to more than $1 billion in assets under management and become an important part of Hamilton ETFs’ growth and story. Its success reflects our focus on developing thoughtful, differentiated investment solutions, which is key to the Hamilton ETFs ethos.

“As an ETF provider, you want to offer products that make your clients money, it can’t just be about inflows to you. We always ask: is this a good product? Does it add value and choice to investors?” said Executive Chairman and Co-Founder Robert Wessel.

Some of the factors that have made HCAL stand out:

Owning blue-chip Canadian banks: HCAL provides exposure to the Canadian banks, one of Canada’s most trusted sectors with an uncommonly long record of dividend sustainability.

Similar volatility to an individual Canadian bank stock: Since inception, the increase in volatility from the enhanced structure roughly offsets the decline in volatility from diversification. As a result, HCAL has had a volatility profile roughly equal to owning any single Canadian bank stock (see chart below).

The outcome?

HCAL has provided investors with strong returns over its 5-year track record. Since inception, it has provided investors with both a higher long-term return than the Big Six banks, at 30.3% annualized return (see table below) and higher yield with similar volatility to the Big Six Canadian banks.

Hamilton ETFs: Pioneers of Enhanced ETFs

Launched in October 2020, HCAL was Canada’s first “enhanced” ETF followed by the second, the Hamilton Enhanced Canadian Covered Call ETF (HDIV), which launched in July 2021. When creating HCAL, we chose 1.25x exposure, which we believe is a “Goldilocks” level of leverage, because our analysis and back-testing of the strategy suggested higher long-term return potential while maintaining a volatility profile similar to that of an individual Canadian bank stock[6]. Continue Reading…

The “Dogs of the TSX” dividend investing strategy for Canadian stocks has been a focus of mine for the past 14 years. I don’t follow the “Dogs” strategy with a majority of my portfolio, but it is a key factor when I look at my relative weighting of Canadian stocks at the end of each year. My key Dogs pick for 2024 and 2025 was Power Corp – and man did they make me look smart last year! (More on that in a second…)

I want to make it clear that the Dogs of the TSX is not something that I created. In fact, it’s actually an American idea. Michael B. O’Higgins wrote a book called the Dogs of the Dow back in 1991, and the idea was later adapted to the Canadian market. I first came across the “Dogs” method of stock picking when MoneySaver magazine started a column titled BTTSX – short for Beating the TSX – dividend stock strategy. (Click here to skip directly to my 2026 picks).

The theory behind the Dogs of the TSX strategy is to look for solid cash-flow-positive stocks that have fallen out of favour for one reason or another. In other words, you’re looking to take advantage of short-term market inefficiency when it comes to the pricing of blue-chip Canadian stocks. A low price and a high dividend results in a high dividend yield.

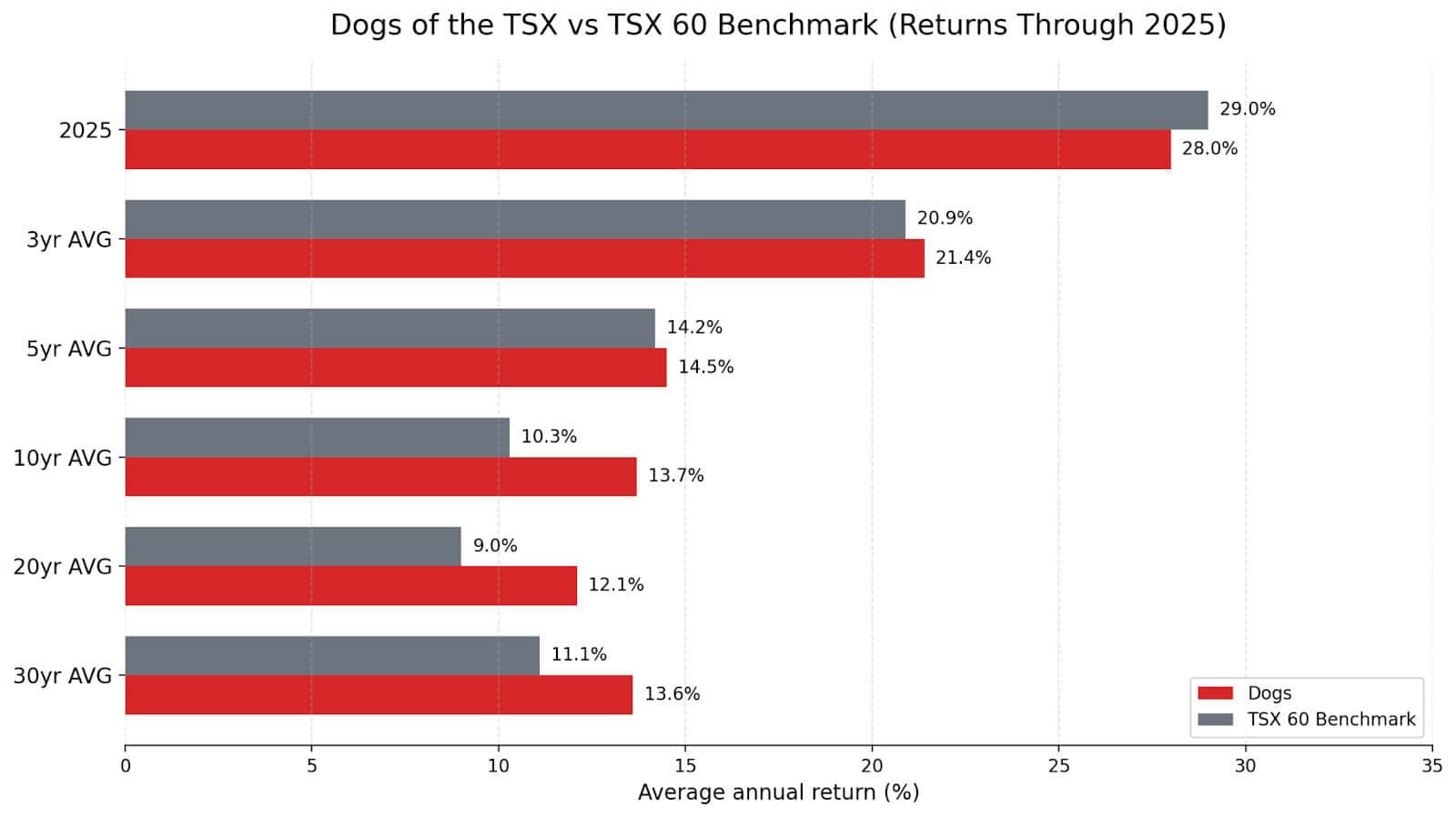

The chart below illustrates the total return (dividends plus price capital gains) versus the TSX 60 benchmark over the years. Looking at 2025, our Dogs of the TSX portfolio of 10 stocks was very similar to the overall TSX 60 index. In fact, the average return lead that the BTTSX strategy has over 3- and 5-year periods is fairly minor. That said, when we look out over the longer terms, we see consistent outperformance in the range of 2-3% per year.

If you had $100,000 invested 30 years ago, the constant difference in compounding would have left you about $2 million richer today had you followed the Dogs of the TSX BTTSX strategy.

When we look back over the last year, the banks had a great year, and the telecommunications companies continued to get beat up. Consequently, we’re going to lose TD off of the list this year (its share price has finally caught up to its dividend payout).

In its pure original form, the Dogs the TSX strategy simply involved ranking the companies in the Toronto Stock Exchange 60 index (aka: TSX 60) by their dividend yield. The highest yield gets the top spot. Then you simply invest equal amounts in all top ten dividend yield stocks.

The idea is that investing in companies that have relatively high free cash flow – but relatively low share prices – is an excellent way to systemically outperform the broader market. No need to pick stock winners with any sort of fancy algorithm – just choose dividend stocks that are out of favour and consequently have high yields.

The average yield for the stocks making the 2026 Dogs of the TSX is about 5.26%. That’s down about 1% from last year – showing that valuations on these companies have raced ahead of their free cash flow and dividend payouts. (In theory, it could also be the case that these companies cut their dividends, but since only BCE did that, we can eliminate that theory.)

In my own implementation of the BTTSX strategy I often eliminate Real Estate Investment Trusts (REITs), and any stocks that have cut dividends OR have insanely high payout ratios (foreshadowing a future dividend cut). Those rules helped me avoid the Algonquin disaster in years past. I didn’t trim much of my BCE holdings before the cut, and I have to admit that I’m getting nervous about Telus: but haven’t pulled the trigger yet.

You’ll notice that my Dividend Dogs of the TSX list has a lot in common with my Best Canadian Dividend Stocks list that I update monthly. There’s obviously a lot of overlap in selecting value-driven, stable, Canadian company stocks.

Top Canadian Dogs of the TSX Pick for 2026: Emera (EMA)

My 2024 and 2025 Dogs of the TSX picks were identical to one another: Power Corp (POW).

While I looked pretty average in January last year, I look pretty darn smart today! That’s because Power Corp saw a total return of over 75% last year!!

In fact, the share price has done so well, that it has outpaced the dividend, and dropped POW right off the BTTSX list for 2026. The biggest driver was Great-West Life’s robust earnings. On top of that, IGM has quietly stabilized its asset base, and Wealthsimple continues to expand its footprint, with more rumours swirling about that Schedule 1 bank licence approval. Investors are finally pricing in the fact that Power Corp isn’t just a stodgy old financial holding company. It’s a well-run, diversified business with growth levers in both traditional finance and the fintech space.

The other stock I highlighted as a Dogs of the TSX stock to watch was TD Bank: and again, TD did so well (total return of about 70%!) that it’s not on the list this year!

It is nearly impossible to duplicate those results going forward. Those two picks both hit the perfect tailwind, and while I believed they were significantly undervalued 12 months ago, I would have told you that you were crazy if you said they’d have total returns of more than 50%, nevermind 70%!

Now, I’m not nearly as bullish on the overall market going into 2026 as I was in 2025. I don’t see any screaming “buy now” deals out there. That’s why my 2026 Dogs of the TSX pick is Emera.

It’s definitely not a stock that’s going to light up Reddit boards. What it is, is a regulated utility with a high starting yield, visible growth, and a US-expanding business mix that I think the market is still undervaluing.

At its core, Emera is a regulated electric and gas utility operator. More than 90% of its earnings come from regulated sources, and roughly 96% of its assets sit inside rate-regulated frameworks. That price stability is exactly what you want when you’re building a dividend-focused portfolio in a market that feels a bit stretched.

Emera operates across Canada, the U.S., and parts of the Caribbean, but the business is much simpler than the geographic footprint suggests.

The short version is this: Florida’s data center growth is the story. Canada is secondary. Everything else is noise.

Emera’s crown jewel is Tampa Electric, which sits under its TECO Energy subsidiary in Florida. That operation benefits from population growth, constructive regulation, and a steady stream of capital investment tied to grid hardening, electrification, and storm resilience. If you believe Florida continues to grow and data centers continue to put pressure on electrical grids (and all signs point that way), Emera has positioned itself very well.

One of the reasons Emera stands out to me right now is management’s five-year, $20 billion capital plan, announced late in 2025. This isn’t vague guidance. It’s a detailed roadmap that extends 7–8% consolidated rate base growth through 2030, with nearly 80% of that capital earmarked for Florida.

That’s meaningful growth for a regulated utility. And importantly, it’s growth that regulators expect and allow utilities to earn returns on.

Canadian assets (which are mostly through Nova Scotia Power) do introduce some political and regulatory friction. But when I look at where Emera is allocating capital, it’s clear management understands where the best risk-adjusted returns are coming from. The payout ratio is pretty darn high, and the balance sheet carries too much debt for my liking. That said, with interest rates coming down in the US, and regulations coming off the books, I like the short- and medium-term prospects.

In a market where many stocks feel priced for perfection, Emera feels priced for caution. That’s what I’m looking for in 2026.

June 2026 Update: So far so good, Emera. It’s up about 7% on the year, which means that it is slightly outpacing the overall TSX 60 index. When you consider that its dividend is higher than that of a TSX 60 ETF, the gap opens up a bit more. American assets and earnings continue to perform well (as I figured they would). So while it’s not performing as well as my Toromount Industries Dividend King pick, or as well as Power Corp (which just continues to power on after last year’s incredible run, up 13% so far in 2026), Emera continues to add steady dividends and capital gains to my portfolio.

One thing to note in regards to Power Corp (which still holds a prominent place in my TSX Dogs Portfolio after its big move last year) is that its Wealthsimple subsidiary continues to post explosive growth. While I don’t at all like the direction the company is going from a user perspective, it is undeniably finding new ways to monetize its young customer base. The company recently made waves by saying it was going to be one of the first Canadian companies to bring predictive markets (think online betting like Kalshi or Polymarket down in the States) to Canada. If casinos are a license to print money, online casinos are a license to print money right across an entire country!

Visit DSR & Get Our Exclusive Discount

Dogs of the TSX Dividend Stock Strategy Implementation

Here is the step by step procedure of how this strategy is implemented: Continue Reading…

Of all the Retirement Rules of Thumb discussed over the decades I’ve spent writing about investing and Retirement, few are more ubiquitous than financial planner William Bengen’s famous 4% Rule, which is his rough estimate of the annual percentage of a portfolio that can safely be withdrawn each year without causing your retirement nest egg to run out of money in old age (adjusted for inflation.) While he has more recently updated it to a slightly higher 4.7%, the “Rule” continues to fascinate and sometimes provoke financial advisors, retirement gurus and media pundits.

Below, we asked various North American advisors, business owners and other experts to weigh in via Linked In and Connectively (formerly Featured.)

Here’s how the question was posed earlier this month on Connectively:

What is your view of William Bengen’s famous 4% Rule, which he seems to have adjusted up to about 4.7%? Are either of these realistic percentage gains, or are they too optimistic or too pessimistic? If you have clients of varying ages (from Gen Z to retired Boomers), did any religiously cleave to this Rule or is it just a starting point around which specific investment objectives were overlaid?

As usual, we have only lightly edited the responses which appear more or less intact, complete with author picture, title and links to their respective web sites. The subheadings are either direct quotes from their input (indicated in quotation marks) or slightly edited variations of quotes.

“The Rule works as a conversation starter, not a finish line.”

Bengen’s rule is a solid anchor, not a contract. I’ve worked with retired clients who treated 4% as gospel and ended up leaving significant money on the table because they were terrified to spend: even when markets had doubled their portfolio.

The honest answer is that the “right” number depends entirely on sequence-of-returns risk, tax drag, and spending flexibility. A Boomer pulling from a traditional IRA faces a very different math than a Gen Z client with decades of Roth compounding ahead. Same percentage, completely different outcome.

Where I’ve seen the rule actually help is as a conversation starter, not a finish line. One business owner client near Crown Point was fixated on hitting a magic retirement number. When we layered in tax-efficient withdrawal sequencing — mixing taxable, traditional, and Roth accounts — their sustainable spending rate shifted meaningfully without touching the portfolio risk profile at all.

The Bengen rule also assumes relatively static spending, which almost no one has. Clients in their early retirement years typically spend more on travel and experiences, then spending drops mid-retirement, then healthcare costs spike late. A single fixed percentage ignores that entire curve. A living financial plan accounts for it. — Daniel Delaney, Owner, Seek & Find Financial

A useful mental anchor but don’t treat it like gospel

The 4% Rule is a useful mental anchor, but treating it as gospel is like using a map from 1994 to navigate a city that’s been rebuilt three times since. Bengen’s original research was groundbreaking for its era. It gave people a simple number to hold on to. But the world it modeled — steady bond yields, predictable inflation corridors, a relatively stable geopolitical backdrop — that world doesn’t fully exist anymore.

Here’s how I think about it. The 4% Rule assumes you’re a passive participant in your own financial life. You retire, you draw down, you hope the math holds for 30 years. That framing made sense when most people had one career, one pension, and one plan. Today, the most financially resilient people I know, from Gen Z creators to semi-retired Boomers, don’t think in terms of a single withdrawal rate. They think in terms of optionality.

I’ll give you a real example. A former VC CFO I spoke with last year told me he stopped thinking about the 4% Rule entirely when he realized his “retirement” would include three or four income-generating projects running simultaneously, most of them enabled by AI tools that didn’t exist five years ago. His withdrawal rate fluctuates between 2% and 6% depending on what’s producing cash flow in a given quarter. The rule became irrelevant because his income never fully turned off.

Bengen adjusting to 4.7% reflects updated data, but it still operates inside the old paradigm: accumulate, then deplete. For younger generations, the line between accumulation and distribution is blurring completely. A 28-year-old building a side business with AI isn’t thinking about safe withdrawal rates. They’re thinking about how to make their capital work alongside earned income indefinitely.

So is 4% too optimistic or pessimistic? Neither. It’s just incomplete. The better question isn’t “what percentage can I safely withdraw?” It’s “how do I build a life where I’m never fully dependent on withdrawals alone?” That reframe changes everything. — Runbo Li, Cofounder and CEO, Magic Hour AI

GenZ and Millennials ignore it completely

I view the 4% Rule as more of an idea to explore, not something carved in stone, and the 4.7% update is essentially Bengen coming clean about what many of us already say: One number will not make it through intact after meeting real-world markets, tax brackets, and spending needs. It is those Boomers taking 4% as their gospel and panic selling in a tough year or, worse, never adjusting for a tough sequence of returns early on during retirement where I have seen people make their biggest mistakes. On the other hand, my Gen Z and Millennial audience members ignore it completely because they are decades away, and they have much better control over income right now through negotiation or side work such as surveys and focus groups than by worrying about a withdrawal rate that is years away from being used. In my opinion, use 4% as a quick and dirty check and build yourself a withdrawal range based on your own individual circumstances. — Scott Brown, Founder, MintWit

“Real life rarely matches the assumptions behind any single retirement rule.”

From my perspective, the 4% Rule has always been more useful as a planning framework than a guarantee. Whether someone uses the original 4% guideline or William Bengen’s later research suggesting that a higher starting withdrawal rate may have been sustainable under certain historical conditions, I don’t think either figure should be treated as universally correct.

I’ve worked with business owners and professionals at different stages of their careers, and one thing stands out: real life rarely matches the assumptions behind any single retirement rule. Markets change, spending isn’t static, people retire at different ages, and unexpected expenses inevitably arise.

That’s why I encourage people to use the rule as a starting point rather than a destination.

For younger professionals, including many entrepreneurs, the conversation is usually less about withdrawal rates and more about building assets, increasing income, and creating flexibility. For those nearing retirement, the focus shifts toward sustainable income, but I still don’t recommend relying on one fixed percentage alone.

I’ve also noticed that financially disciplined people tend to adjust their withdrawals based on market conditions instead of following the exact same rate every year. They’re willing to spend a little less after a difficult market and a little more when their portfolio performs well.

As a founder, I appreciate simple financial frameworks because they help people begin planning, but they shouldn’t replace individualized decision-making.

If I were advising someone, I’d say the 4% Rule — or even 4.7% — is a reasonable benchmark, not a promise. The more important questions are: How long does your money need to last? How much flexibility do you have in your spending? What’s your investment mix, and how comfortable are you with market volatility?

In my experience, successful retirement planning isn’t about finding the perfect withdrawal percentage. It’s about creating a strategy that can adapt as your life and the markets inevitably change. — Max Shak, Founder/CEO, nerD AI

The Rule is “a stress-test starting point, not a spending command.”

The first clarification is that 4% or 4.7% is a withdrawal rate, not an expected investment gain. Under the original approach, a retiree withdraws that percentage of the starting portfolio in year one and then adjusts the dollar amount for inflation.

For a $1 million portfolio, the difference between 4% and 4.7% is $7,000 in the first year: $40,000 versus $47,000. That difference may look modest, but it becomes important when retirement begins before a major market decline or period of high inflation.

I treat either figure as a stress-test starting point, not a spending command. The appropriate plan depends on retirement length, taxes, fees, portfolio composition, pension or Social Security income, essential spending and the retiree’s willingness to reduce withdrawals after weak markets. A person retiring in their forties should not automatically use the same assumption as someone retiring at seventy with reliable pension income.

I do not have U.S. retirement-advisory clients, but my finance approach is to model several scenarios rather than rely religiously on one percentage. The safer plan is usually one that protects essential spending, keeps a separate reserve and allows discretionary withdrawals to adjust when markets or inflation behave badly. — Cem Oner, Founder / Finance & Public Data Publisher, hesapcebimde.com

If you are underweight equities or neglect rebalancing, “a fixed 4 per cent can be too optimistic; with disciplined equity exposure and regular rebalancing it is more attainable.”

I view William Bengen’s 4% rule as a useful planning baseline but not a fixed rule for every retiree. It provides a clear starting point for estimating sustainable withdrawals, but its realism depends on factors I see often in client portfolios, such as asset allocation, rebalancing habits, and savings adequacy. When investors are underweight equities or neglect rebalancing, a fixed 4 percent can be too optimistic; with disciplined equity exposure and regular rebalancing it is more attainable. Very few clients strictly adhere to a single percentage in my experience. Instead, the rule is typically used as an initial benchmark onto which specific investment objectives and cash flow needs are overlaid. I therefore advise starting with the 4 percent figure, conducting a full portfolio audit, and automating contributions and rebalancing to align the plan with individual goals. — Amir Husen, Content Writer, SEO Specialist & Associate, ICS Legal

Financial Advice should not be based on a single Rate of Return

Looking back at my over two decades of experience working with financial companies to boost their Internet presence, one thing I’ve learned is that guidelines like the 4% rule are so well-known because they’re easy to remember. The problem here is that most people confuse headlines or popular guidelines as a reasonable solution for their retirement. Whether they’re talking about 4%, or William Bengen’s idea around 4.7%, in some circumstances, I would consider those as opening lines of discussion.

Highly trusted financial institutions do not base their advice on a single rate of return. Financial institutions provide interpretation of the assumptions made regarding rate of return and customize advice according to retirement age, required income, taxes, health care expenses and other sources of income.

From my perspective, good financial advice doesn’t make any promises about guarantees. This allows one to realize the reasons why a certain rule may be wrong and to start a conversation with an expert in this field. A notable percentage may help clarify a complex idea, but good retirement strategies are always based on flexibility. — Derek Iwasiuk, Co-owner, Director of marketing, Searchtides

It all depends on Sequence of Returns, which is out of your control

The 4% Rule works fine as a starting number. That’s why most people accept it as a default. But you shouldn’t consider it a guarantee. Just guidance, not prescriptive one. The rule works only within the confines of the assumptions used to create it. Bengen wasn’t using an average of the stock and bond market returns. He used one specific period in the market and one very particular mix of assets.

The 4.7% rule is similar, only it uses slightly different numbers. When looking to live off your investments for the rest of your life, can you really go wrong using either number? It depends on the sequence of returns, which is completely out of your control. Continue Reading…

I liked Charles Ellis’ book Winning the Loser’s Game so much that I had to read his latest: Rethinking Investing. It is very short at just over 100 small pages, but is packed with good advice. Some of it is specific to U.S. tax laws, but most of it is useful for Canadians.

Ellis takes on three huge areas of personal finance. The first is your portfolio allocation, or what you should invest in.

The second is your savings plan, and the third is your “spending rule,” or how to spend your assets during retirement.

A detailed treatment of these areas could easily run to thousands of pages, so this book is necessarily at a high level. Ellis wants you to get the broad ideas right, so that you won’t make big mistakes as you fill in the details.

Ellis calls compounding investment returns “your power curve.” He explains that most of your investment growth comes at the end, which provides motivation to begin early. Saving is “your first priority.”

Saving

He offers thirteen specific suggestions for saving money, such as use employer matching, automate deductions from pay, invest bonuses, buy preowned cars, consider a smaller house, “self-insure for auto damages under $10,000 — or whatever you can comfortably afford to pay in the unlikely event of a major accident” — and use term life insurance.

Unlike recent popular advice to focus only on big expenses, Ellis says that “Lots of small-expense items can add up and cut your potential savings.”

Investing

Ellis repeats the main themes of Winning the Loser’s Game to explain why low-cost index investing is the way to go. “The growing market dominance of expert professional investment managers … has made the market harder and harder to beat.”

There are three factors slowing down the “widespread adoption of indexing.” Referring to index investing as “passive” has negative connotations for most people. “Nobody wants to be known as passive.” The second factor is that “most investors find it hard to believe that talented active managers with superb information won’t beat the market.”

These active managers “fought against indexing as though they and their careers were seriously threatened: as they surely were and certainly are!” The third factor comes from the media, who know “that indexing’s persistent successes would not make for compelling or even interesting copy.”

When investors make active choices on market timing, they tend to perform poorly. Unfortunately, Ellis points to reports from DALBAR for evidence of this pattern. While it’s true that retail investors make poor market timing choices on average, DALBAR’s methodology for computing their losses is nonsense.

Bond allocation

Ellis makes an interesting pitch for investors to own more stocks and fewer bonds. He asks investors to include the following as part of their bond allocation: “home equity, the present value of your Social Security benefits [CPP and OAS in Canada], and your future estimated savings plus any likely inheritance.”

While I think many people would be better off with a lower bond allocation during their working years, I have to push back on the future estimated savings and inheritances. Maybe government workers can treat future savings as bond-like, those in the private sector have a lot of uncertainty in their future savings.

As for an inheritance, I see huge uncertainty in most cases. A parent may end up needing the money for elder care, or may give it to someone else, or may have less money than you think. The money I will leave to my sons is mostly invested in stocks, and they will get what’s left after all my spending. The amount they will get does not have bond-like attributes.

All that said, if thinking about home equity, government payments, future savings, and an inheritance helps people tolerate the short-term swings in stock prices, then maybe Ellis is right to give this advice, even if it isn’t all technically correct.

Retirement spending rule

Ellis encourages people to think about drawing from their savings in retirement like a university endowment. “First, average the year-end values of your assets over the prior several years (preferably more than five years) to dampen the impact of market fluctuations.” Then choose a prudent annual withdrawal percentage, “likely 4–5%.”

“For example, if you settle on a 5% rate of withdrawal and a six-year moving average of the year-end value of your assets, a 30% drop in the stock market would lead to only a 5% reduction in your payout that year.” This approach offers an alternative to “having a portfolio laden with low-return bonds.” Continue Reading…

Learn how leadership shifts can change your portfolio and how sector rotation can help you respond.

By Saakshi Mehta, VP, ETF and Alternatives Strategy at BMO GAM

(Sponsor Blog)

Market commentary often reduces equity performance to a single question: are markets up or down? But equity markets do not move as a single block. They are made up of many industries, each responding to different economic forces and expectations around growth, risk and profitability. What looks calm at the index level can mask meaningful shifts beneath the surface.

Chart 1 introduces the Global Industry Classification Standard, or GICS, the framework most investors use to define equity sectors. By grouping companies based on their primary business activities, GICS provides a consistent structure for observing how leadership shifts across the market over time.

This is why sector rotation matters. Whether you actively rotate sectors or not, understanding sector exposures is essential for knowing what risks you’re taking and what’s driving your portfolio’s performance. Ignoring sectors can mean flying blind to some of the most important forces affecting your investments.

Sector rotation strategy is a valuable tool for individual investors seeking to enhance returns and manage risk, but it requires discipline, realistic expectations, and an understanding of both the opportunities and challenges involved.

Chart 1: Global Industry Classification Standard (GICS)

Source: MSCI, S&P Dow Jones, BMO GAM

The Core Concept

A sector rotation framework begins with the key observations: where leadership is forming, what forces are driving it, and how sustainable that leadership might be. In that sense, sector rotation is less about forecasting and more about interpreting what markets are already signaling.

The goal is to overweight sectors expected to outperform and underweight or avoid those likely to underperform. Capital tends to move toward areas where expectations are improving and away from areas where optimism has already peaked.

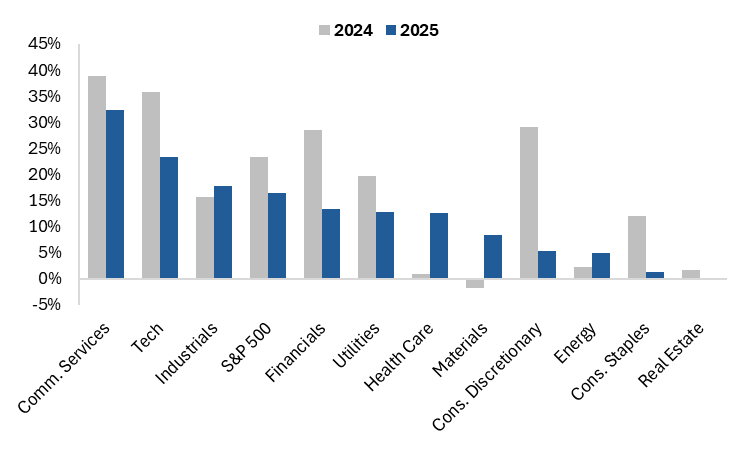

Sector rotation involves shifting your portfolio allocations among different market sectors based on where we are in the economic cycle. This matters because the performance gap between the best and worst sectors in any given year can exceed 15-20 percentage points (Chart 2). Being positioned in the right sectors can meaningfully improve your returns, while being stuck in lagging sectors can significantly hurt performance.

Chart 2: Sector Performance in the US in 2024 and 2025

Data as of year-end 2024 and 2025

Source: Bloomberg, BMO GAM

Divergence is a Feature, not a Bug

Sectors are influenced by different economic and structural forces. Interest rates, inflation, regulation, innovation, labour costs and commodity prices do not affect all businesses in the same way. Because these drivers rarely move in sync, sector performance naturally diverges.

That divergence is not a flaw. It is a defining feature of equity markets. It creates periods of concentration, periods of diversification, and conditions that allow leadership to rotate rather than remain fixed.

Market structure adds another layer. Sector composition varies significantly across regions. As Chart 3 shows, U.S. equity markets are heavily weighted toward Technology, while Canadian equity markets are dominated by Financials and resource-linked sectors. The same global environment can therefore produce very different outcomes depending on which market an investor is exposed to.