By Michael J. Wiener

By Michael J. Wiener

Special to Financial Independence Hub

Occasionally, a friend or family member asks for help with their investments. Whether or not I can help depends on many factors, and this article is my attempt to gather my thoughts for the common case where the person asking is dissatisfied with their bank or other seller of expensive mutual funds or segregated funds. I’ve written this as though I’m speaking directly to someone who wants help, and I’ve added some details to an otherwise general discussion for concreteness.

Assessing the situation

I’ve taken a look at your portfolio. You’ve got $600,000 invested, 60% in stocks, and 40% in bonds. You pay $12,000 per year ($1000/month) in fees that were technically disclosed to you in some deliberately confusing documents, but you didn’t know that before I told you. These fees are roughly half for the poor financial advice you’re getting, and half for running the poor mutual funds you own.

It’s pretty easy for a financial advisor to put your savings into some mutual funds, so the $500 per month you’re paying for financial advice should include some advice on life goals, taxes, insurance, and other financial areas, all specific to your particular circumstances. Instead, when you talk to your advisor, he or she focuses on trying to get you to invest more money or tries to talk you out of withdrawing from your investments.

The mutual funds you own are called closet index funds. An index is a list of all stocks or bonds in a given market. An index fund is a fund that owns all the stocks or bonds in that index. The advantage of index funds is that they don’t require any expensive professional management to choose stocks or bonds, so they can charge low fees. Vanguard Canada has index funds that would cost you only $120 per month. Your mutual funds are just pretending to be different from an index fund, but they charge you $500 per month to manage them on top of the other $500 per month for the poor financial advice you’re getting.

Other approaches

Before looking at whether I can help you with your investments, it’s worth looking at other options. There are organizations that take their duty to their clients more seriously than the mutual fund sales team you have now.

One option is a professional advisor who invests client money in low cost funds. Another option is a client-focused mutual fund company that charges lower fees and provides some good advice for their investors. Either option would save you money and give you better financial advice than you’re getting now. It takes some knowledge to be able to determine whether some other financial advisor is really offering one of these better options. I can help with this if you like.

Can I help directly?

Maybe. I’m only willing to completely take over investments for my closest family members, and even then only if I think leaving it all to me is what they really want. I can set you on a good path, but you may not be able to stay on it, and I may tire of trying to explain why you shouldn’t stray from that path when you decide to sell everything, or buy cryptocurrencies, or whatever idea you’ve come up with.

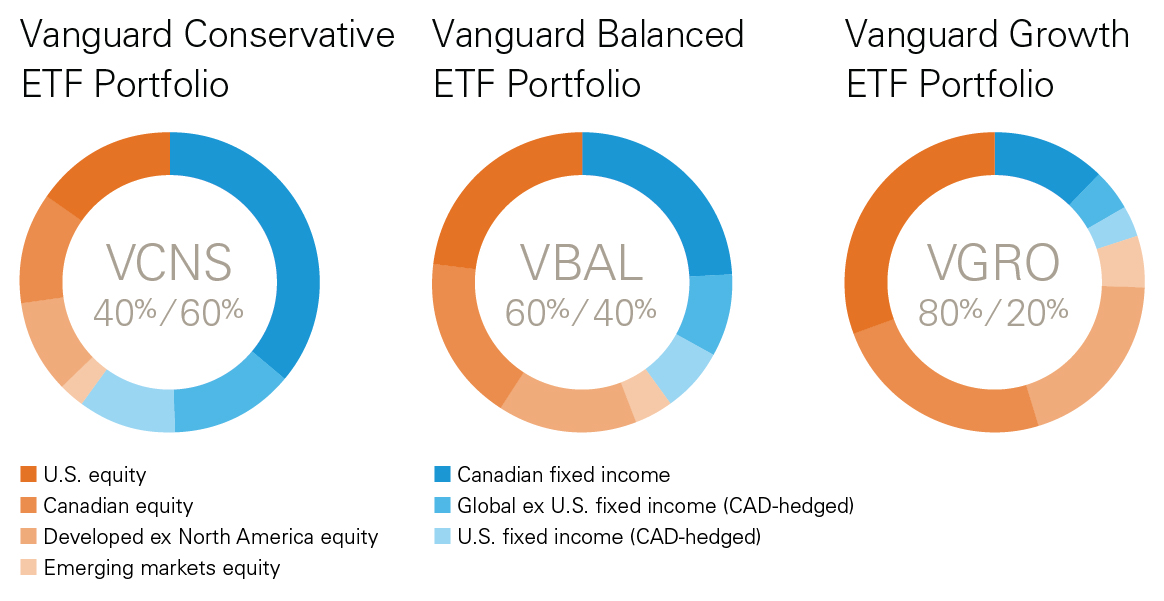

In your case, the good path I’m talking about would be to invest money you won’t need in the next few years in Vanguard’s exchange-traded fund called VBAL. VBAL owns substantially the same stocks and bonds you have in your current portfolio. The difference is that you’ll pay about $880 per month less in fees. After a decade, you’ll save more than $100,000.

[Editor’s Note: VBAL, shown to the right, is 60% equities to 40% fixed income. VGRO is 20% more aggressive while VCNS is the inverse of VBAL, with 60% in fixed income.]

So, if the market goes up 10% one year, you’ll end up with about $10,500 more than if you keep your investments where they are now. And if the market goes down 10% in another year, you’ll still end up with about $10,500 more that year than if you stay where you are now. Either way, the outcome is better.

Risk

The biggest risk I see will come when the market falls substantially at some point in the future, and you’ll decide that I should have foreseen this event and warned you to sell. Nobody can predict market crashes reliably. The best plan is to maintain a sensible risk level in your portfolio and ride out market pain. But that’s much easier said than done.

Many people have a hard time believing that stock market crashes are inevitable and unpredictable, and some financial advisors promise to help steer you around market declines. They may or may not be aware that the managers of the funds they sell can’t avoid losses. If you don’t learn that getting caught in a market crash and having to ride it out is an inevitable part of investing, you’re doomed to jumping from one expensive advisor to another every time stocks crash.

Conclusion

So, the short answer to the question of whether I can help you with your investments is that it depends on how easily you can be distracted from a simple and successful investing path and how much energy I have for talking you back to that path.

Michael J. Wiener runs the web site Michael James on Money, where he looks for the right answers to personal finance and investing questions. He’s retired from work as a “math guy in high tech” and has been running his website since 2007. He’s a former mutual fund investor, former stock picker, now index investor. This blog originally appeared on his site on June 22, 2023 and is republished on the Hub with his permission.

Michael J. Wiener runs the web site Michael James on Money, where he looks for the right answers to personal finance and investing questions. He’s retired from work as a “math guy in high tech” and has been running his website since 2007. He’s a former mutual fund investor, former stock picker, now index investor. This blog originally appeared on his site on June 22, 2023 and is republished on the Hub with his permission.