By Mark Seed, myownadvisor

Special to Financial Independence Hub

A reader recently asked me the following based on reading a few pages on my site:

Mark, does it make sense to have 100% of your portfolio in stocks? If so, at what age would you personally dial-back to own more cash or GICs or bonds? Thanks for your answer.

Great question. Love it. Let’s unpack that for us.

References:

Should you have 100% of your portfolio in stocks?

Maybe as a younger investor, you should.

Let me explain.

Members of Gen Z, which now includes the youngest adults able to invest (born in the late-1990s and early-2000s), represent a cohort that could be investing in the stock market for another 60 more years.

According to a chart I found on Ben Carlson’s site about stuff that might happen in 2023, over 60+ investing years in the S&P 500 (as an example) historical indexing performance would suggest you’d have a better chance of earning 20% returns or more in any given year than suffering an indexing loss. Pretty wild.

Source: A Wealth of Common Sense.

Shown another way as of early 2023:

Source: https://www.slickcharts.com

This implies younger investors, in my opinion, should at least consider going all-in on equities to take advantage of long-term stock market return power when they are younger given:

- As you age, your human capital diminishes – your portfolio (beyond your home?) can become your greatest asset.

- Younger investors can also benefit from asset accumulation from periodic price corrections – adding more assets in a bear market; allowing assets to further compound at lower prices when corrections or crashes occur (i.e., buying stocks on sale).

Consider in this post on my site:

In the U.S.:

- a market correction occurs at least once every 2 years, of 10% or more

- a bear market at least every 7 years, where market value is down 20% or more

- a major market crash at least every decade.

And in Canada for additional context:

The C.D. Howe Institute’s Business Cycle Council has created a classification system for recessions, grouping them together by category.

According to the council:

“Category 1 recessions have only a short, mild drop in GDP and no decline in quarterly employment. At the other extreme, Category 5 recessions involve extremely rapid contractions of the economy over an extended period of time.”

| Monthly Peak | Monthly Trough | Category 1 to 5 |

| October 2008 | May 2009 | 4 |

| March 1990 | April 1992 | 4 |

| June 1981 | October 1982 | 4 |

| January 1980 | June 1980 | 1 |

| December 1974 | March 1975 | 2 |

| March 1960 | March 1961 | 3 |

| March 1957 | January 1958 | 3 |

| July 1953 | July 1954 | 4 |

| April 1951 | December 1951 | 3 |

| August 1947 | March 1948 | 2 |

| November 1937 | June 1938 | 5 |

| April 1929 | February 1933 | 5 |

Source: C.D. Howe Institute Business Cycle Council.

Canada has experienced five recessions since 1970.

Our domestic recessions usually last between three to nine months.

“This means you should at least prepare for three to nine months of very bad economic results and markets to weather, at any time.” – My Own Advisor.

Should you have 100% of your portfolio in stocks?

Maybe as an established investor, you should not.

Let me explain.

My thinking is that as you age, you should at least consider easing up on 100% stocks in your portfolio for the same reasons younger investors should go all-in on equities. Time.

Or lack thereof, less time to recover.

“Established investors may want to consider shifting from asset accumulation towards income generation and asset preservation.” – My Own Advisor.

This way, assets so carefully accumulated over the preceding years need not be sold off at inappropriate times such as a stock market corrections, crashes or prolonged bear markets.

Recall in the last two (2) lost decades, it could literally take a decade until equity markets come into demand-favour again.

Older investors will recall the 1970s was no picnic, starved for market growth.

The second “lost decade” started around the early 2000s. The hype over technology start-ups in the early 2000s led to overvaluations and the burst of the dot-com bubble, wiping out some $5 trillion U.S. in technology-firm market value between March and October of 2002.

Amazon, a stock darling today, was one of the few companies that survived this crisis. Its stock had plunged some 90% across 2000-2002.

To sum up, the 1999-2009 U.S. investing period was marked by the collapse of the late dot-com bubble, the 9/11 terrorist attacks, the Iraq and Afghanistan wars, as well as two recessions, the deepest being the 2008-2009 Financial Crisis. During that period, the S&P 500 gained nothing as part of annualized returns and here in Canada we didn’t do any better.

While any future “lost decade” would be rare, history can rhyme.

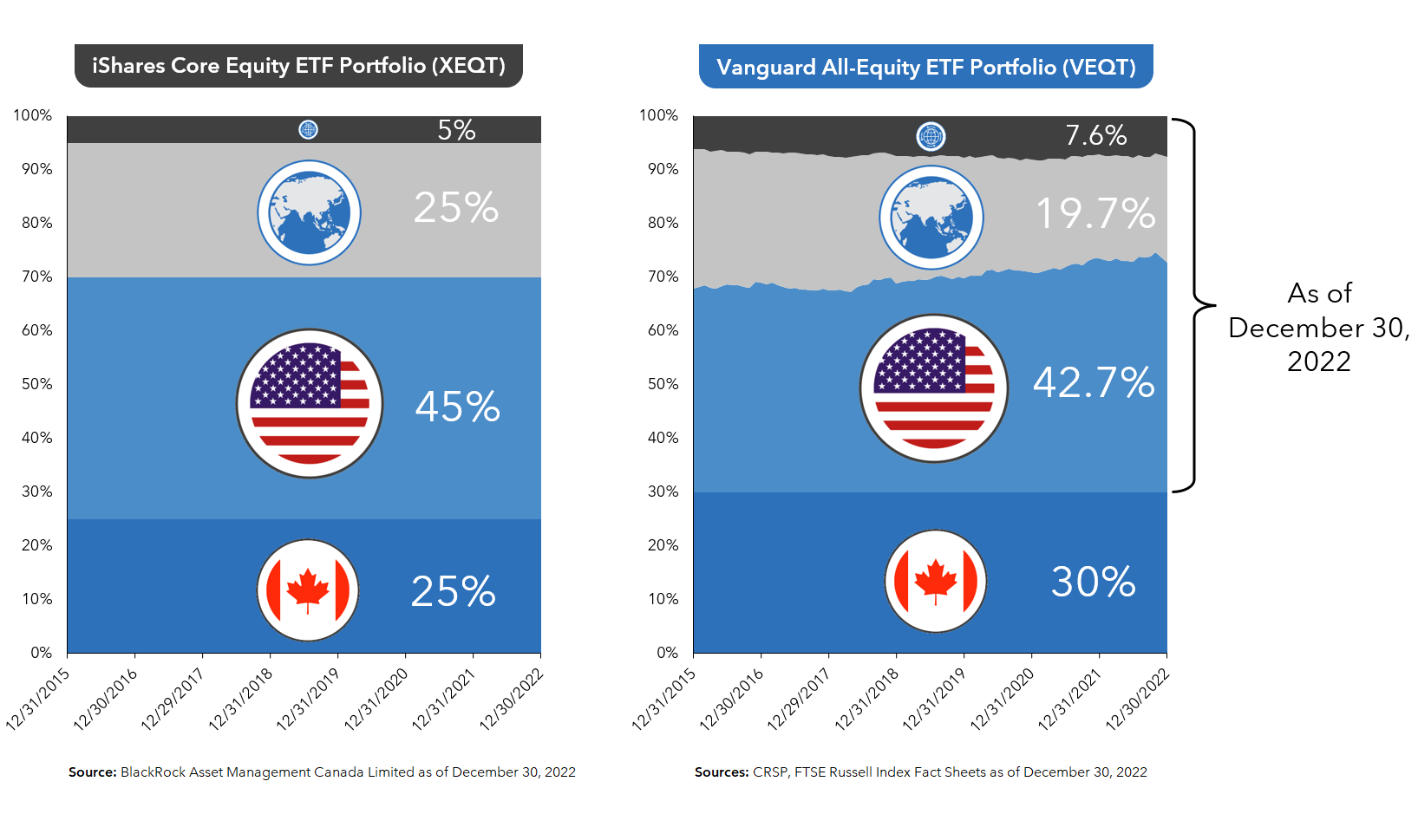

As such, I am ensuring I/we have diversification beyond U.S. indexes to provide additional possibilities for income and growth beyond the tech- and cap-weighted S&P 500 of today.

Source: https://www.syfe.com/magazine/are-we-heading-into-another-lost-decade-of-investing/

Should you have 100% of your portfolio in stocks summary

DIY investors, readers and passionate investors know from my site that there is no universal answer for every investor, so it’s important to think through both the upsides and downsides when it comes to your investing plan.

Odds are, if investing history is any guide, that over a period of 5, 10 or more years, stocks should perform better than bonds.

For this reason, I/we will continue to have a strong bias to stocks in our portfolio over bonds and some cash.

Instead of worrying about stock market corrections, how long any stock market correction might last, I’m more inclined to worry about some things within my control and influence:

- My sustained savings rate for investing.

- The ability to remain with my hybrid investing plan of stocks and low-cost ETFs.

- Keeping some cash to pounce when equity opportunity strikes, and

- Avoiding fearmongering market news.

“I see the stock market, as a tool, for average people/average investors to be long-term business owners.” – Larry Bates, Beat the Bank.

While a 100% equity investment portfolio could make sense for younger investors, decades away from retirement, keeping 100% of your portfolio in stocks as you enter retirement or remain in retirement could introduce unnecessary risk.

“The individual investor should act consistently as an investor and not as a speculator.” — Ben Graham.

You are an investor, not someone who can predict the future.

Base your investing decisions on real facts and analysis.

As we have remembered today, stocks unto themselves can be unreliable over a 10-year investing timeline.

As we work towards semi-retirement, we intend to increase our cash wedge while owning a mix of dividend stocks that should provide rising income and low-cost ETFs that should deliver growth.

I’ll keep you posted if we change our minds/approach and I hope you do the same.

Thanks for reading.

Mark

Footnote, added after posting. Food for thought from Ben Graham, Warren Buffett’s mentor:

Mark Seed is a passionate DIY investor who lives in Ottawa. He invests in Canadian and U.S. dividend paying stocks and low-cost Exchange Traded Funds on his quest to own a $1 million portfolio for an early retirement. You can follow Mark’s insights and perspectives on investing, and much more, by visiting My Own Advisor. This blog originally appeared on his site on August 28, 2023 and is republished on the Hub with his permission.

Mark Seed is a passionate DIY investor who lives in Ottawa. He invests in Canadian and U.S. dividend paying stocks and low-cost Exchange Traded Funds on his quest to own a $1 million portfolio for an early retirement. You can follow Mark’s insights and perspectives on investing, and much more, by visiting My Own Advisor. This blog originally appeared on his site on August 28, 2023 and is republished on the Hub with his permission.

I have all my portfolio in stocks and it will stay in stocks until I die.

Alain, so you just completely ignore the wisdom communicated in the above article. Not a recommended strategy for most diy investors who always struggle with stock volatility.