Another turning point, a fork stuck in the road

Time grabs you by the wrist, directs you where to go

So make the best of this test and don’t ask why

It’s not a question, but a lesson learned in time

It’s something unpredictable, but in the end is right

I hope you had the time of your life

— Good Riddance (Time of Your Life), by The Green Day

By Noah Solomon

Special to Financial Independence Hub

The Latin term sine qua non literally means “Without which, not.” It refers to something that is indispensable. With respect to investing, this term applies to risk management, which is essential for achieving better than average results over the long term.

In this month’s commentary, I will discuss the advantages and drawbacks of the more commonly used approaches to reduce portfolio volatility. I will also explain why volatility management for its own sake is a value-destroying endeavour. Lastly, I will provide a contextual framework for measuring managers’ risk management skills.

Macro Forecasting: Failing Conventionally

Ever since tariff-related concerns unsettled markets in April, I have been asked countless times what I think is going to happen and how investors should be positioned. Relatedly, to improve performance by predicting macro developments, you need the ability to:

- Consistently predict short-term developments, and

- Make portfolio changes that produce results that are better than what would have been the case had you simply done nothing.

By no means is this failure due to lack of effort, diligence, or intelligence. However, the simple fact is that interest rates, inflation, unemployment, and economic growth are all influenced by thousands of factors. Not only do these factors influence economic conditions on an individual level but also influence each other. In other words, millions of complex interactions affect macroeconomic conditions, thereby making forecasting a thankless endeavour.

How prices respond to events is not merely a function of the events themselves but also of the degree to which events are already discounted in prices before they occur (i.e. investor expectations). This observation explains why overly optimistic expectations can result in a company’s stock falling after it reports stellar results. Similarly, it also explains how excessively pessimistic expectations can result in price increases after disappointing news.

In short, with respect to price movements and events, it’s not about whether an event is positive or negative, but rather about how the event compares with what was expected. Unfortunately, when it comes to gauging expectations, and by extension, how much of a given event is “baked in” to security prices, investors are by and large flying blind. There is no place where you can determine exactly what investors are expecting regarding inflation, GDP, or unemployment. Whereas asset prices offer some clues in this regard, they by no means offer any reasonable degree of precision.

Finally, even if people could predict future events and accurately estimate broad-based expectations of such events, it is still unclear if such knowledge would lead to superior performance, as shorter-term price movements are largely a function of swings in investor psychology, which are impossible to predict.

If I am correct in my assertion that basing one’s investment strategy, either in whole or in part, on forecasting future developments is at best impractical, then why does doing so remain popular? All I can offer in this regard is the following:

1.) The proverbial “size of the prize” is so large that investors can’t resist the temptation, regardless of how poor the odds: if you could consistently profit from short-term market movements, your performance would make even Buffett’s look poor!

2.) Entertainment value: predicting economic trends can be intellectually engaging and even a “sport” for some.

3.) Following the herd: Managers may engage in forecasting for the simple reason that everyone else is doing it, and that it would therefore be irresponsible not to. According to John Maynard Keynes, “Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally.”

Volatility: Winning the Battle but Losing the War

Considered in isolation, portfolio volatility is undesirable. However, like almost anything desirable, volatility reduction comes at a price. All else being equal, the more you tilt your portfolio in favour of lower-volatility securities and strategies, the lower your returns will be. I suspect that most people who allocate a portion of their portfolios to lower-volatility assets have a reasonable appreciation for what they are getting. However, I also believe that they have little appreciation for what they are giving up in exchange for this benefit, or more specifically for the magnitude of this sacrifice.

The aftermath of the late ’90s Tech Bubble involved a three-year decline in stocks. During this time, hedge funds weathered the storm relatively well, far outperforming their traditional, long-only peers.

Predictably, the pain of those years in combination with an augmented appetite for stability prompted investors to pile into hedge funds, which caused assets to grow from several hundred billion dollars in 2000 to over $2 trillion by 2007 and to over $4 trillion today.

Just as Adam Smith’s theory of supply and demand would have predicted, the aftermath was far less rosy than hoped for. While the average hedge fund made good on its promise of stability, returns were sorely lacking, resulting in massive opportunity costs for their investors. Over the past 10 years, the HFRX Global Hedge Fund Index has delivered an annualized return of 1.87%, as compared to 9.8% for the MSCI All Country World Equity Index. Using these figures, a $10 million investment in the HRRX Index ten years ago would currently have a value of $12,035,470, while the same amount invested in global stocks would be worth $25,469,675.

Given this stark difference, investors should ask themselves whether their aversion to volatility is mostly financial or mostly emotional. By definition, the answer is the latter for those with long-term horizons. In such cases, the emotionally driven component of volatility aversion has proven, and likely will prove to be very costly indeed!

Private Assets: See no Evil, Hear no Evil, Speak no Evil

Over the past decade or so, private assets have become increasingly viewed as a “you can have your cake and eat it too” panacea which can deliver strong returns while simultaneously shielding investors from high volatility and severe losses in challenging environments. These perceived attributes have led to explosive growth in private investment funds, with assets under management increasing from roughly $600 billion in 2000 to $7.6 trillion as of the end of 2022.

There is good reason to be somewhat suspect of private asset funds’ low volatility and short-term, unrealized returns. While most funds may provide accurate asset values for their holdings, this may not always be the case. Although 2022 was a horrific year for both stocks and bonds, many private equity, private debt, and private real estate funds reported negligible losses.

A Financial Times article titled, “The volatility laundering, return manipulation and ‘phoney happiness’ of private equity,” suggests that not only is “return manipulation” prevalent among private asset managers, but that decision makers who allocate to them are both aware of and complicit in this practice. The author cites a University of Florida study by Jackson, Ling, and Naranjo based on nearly two decades of data from private real estate funds. The paper concludes that “private equity fund managers manipulate returns to cater to their investors.” The study also contends that fund managers “do not appear to manipulate interim returns to fool their investors, but rather because their investors want them to do so.”

On its face, this seems illogical. Surely allocators are not ostriches who bury their heads in the sand to avoid an unpleasant reality. If a manager boosts or smooths returns over the short term, those who allocate to them on behalf of organizations or employers can make themselves look good by reporting results that are artificially consistent and high. But as the saying goes, “you can run but you can’t hide.” Given that inaccuracies eventually come to light as private debt matures and private equity holdings get sold, what’s the point of pretending?

As legendary investor Charlie Munger stated, “Show me the incentive and I’ll show you the outcome.” When one considers that the median tenure of managers who allocate to private asset funds is four years, then being complicit in “aspirational” valuations and mock volatility is rational (at least from a self-serving perspective). In effect, they can benefit from artificial “good times” and be well out of dodge before payback time!

Lastly, unlike publicly listed securities, private holdings have liquidity risk, thereby exposing investors to the possibility of not having liquidity when they are most likely to want/need it. Moreover, I would be surprised if the same Adam Smith dynamic that has been a meaningful headwind for hedge funds does not “infect” private asset managers in a similar fashion, causing future returns to be far more muted. Given an average gestation period of 5-10 years for PE investments, the latest realized returns being reported by managers is based on funds with vintages between 2015 and 2020, when assets under management were between $2-$4 trillion as compared to $10 trillion today.

To be clear, I do believe that private assets can play a valuable role in portfolios. That being said, I also believe that their perceived ability to deliver high returns with low volatility is somewhat unrealistic.

There’s no Free Lunch, but there are Free Snacks: The Beauty of Lopsidedness

Generally speaking, if you want to lower the risk profile of your portfolio, this entails sacrificing returns. By the same token, if you want to reach for higher returns, this inevitably necessitates taking on more risk.

If a manager delivers twice the return of their peers but also exhibits twice the volatility, then they have not added any value for their clients. Rather, they have simply produced twice as much of the “good thing” (return) in exchange for exposing their clients to twice as much of the “bad thing” (volatility). Similarly, for a manager who has half the volatility of their peers with half their returns, the same “robbing Peter to pay Paul” dynamic applies : zero value added.

The Merriam-Webster dictionary defines the term lopsided as “lacking in balance, symmetry, or proportion.” On its face, this description is far from flattering (I certainly wouldn’t take kindly to being referred to as lopsided). However, when it comes to investing, lopsidedness can be good or bad.

To reiterate, nobody can truly be certain about what the future will bring. As stated by Nobel Prize winning physicist Niels Bohr, “Prediction is very difficult, especially if it’s about the future!” It is futile for investors to bang their heads against a wall trying to ordain the future. However, it is a worthwhile endeavour to construct portfolios that can deliver more gains in good times than losses in bad times. Alternately stated, investments should harbour profit potential that is disproportionately large relative to their loss potential.

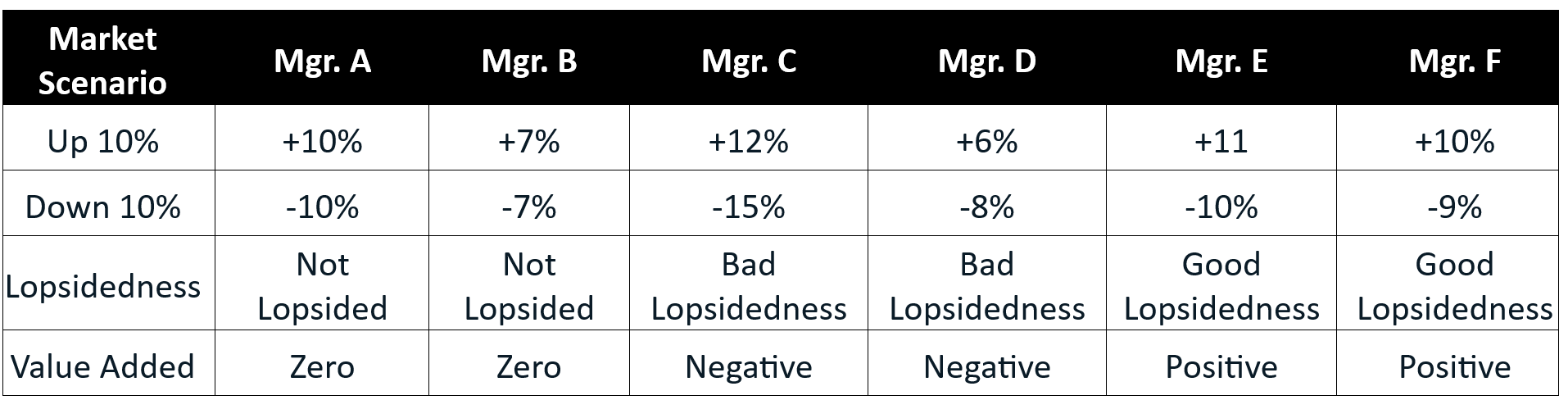

Manager Study: Responses to Market Advances and Declines:

- Both managers A and B are do no harm but do no good for investors.

- Manager A captures 100% of the upside in rising markets but also experiences the same proportion of the downside in declining markets.

- In a similar vein, manager B captures 70% of the market’s upside in the good times but only experiences the same proportion of the market’s losses when things go awry.

- Managers C and D are undesirable.

- Manager C reaps 120% of the market’s gains in favourable times but suffers 150% of the market’s losses in challenging environments.

- Manager D suffers from a similar problem of “bad” lopsidedness, participating in only 60% of market gains while experiencing 80% of market losses.

- Lastly, managers E and F are superior managers.

- Manager E participates in 110% of rising markets while suffering 100% of market declines.

- Manager F is also beneficially lopsided, reaping 100% of market gains while suffering 90% of its downside.

Even long-term investors who are focused exclusively on higher long-term returns and are unconcerned with shorter-term volatility are still better off using leverage to invest in managers E or F rather than allocating to the badly lopsided manager C with the highest returns. In doing so, they could achieve higher returns than manager C with either the same or lower volatility (depending on how much excess returns are desired).

Similarly, even investors who are highly focused on shorter-term volatility are better off investing a lesser amount in managers E or F than they would in badly lopsided manager D with the lowest volatility. In doing so, they would achieve lower volatility than manager D with either the same or higher returns (depending on how great their desire for volatility mitigation).

The bottom line is that, regardless of where you lie with respect to your risk/return preferences, you are always better off with positively lopsided managers who are more efficient deployers of capital.

Summing it all up: Emotions, Suspicions, and Balance

1.) If you are seeking to avoid volatility for emotional reasons, it is important that the long-term financial consequences of doing so are significant.

2.) If you wish to reduce volatility for the “right” (i.e. purely financial) reasons, you should be suspicious of investments that promise high returns with relatively low volatility.

3.) For private investments that offer a better risk/return trade-off than conventional assets, you should consider whether this improvement sufficiently compensates you for the former’s lack of liquidity.

4.) Regardless of asset class, investors should evaluate managers and strategies based on their balance between their ability to generate profits in good times vs. their propensity for losses in bad times.

Happy investing!

Noah Solomon is Chief Investment Officer for Outcome Metric Asset Management Limited Partnership. From 2008 to 2016, Noah was CEO and CIO of GenFund Management Inc. (formerly Genuity Fund Management), where he designed and managed data-driven, statistically-based equity funds. Between 2002 and 2008, Noah was a proprietary trader in the equities division of Goldman Sachs, where he deployed the firm’s capital in several quantitatively-driven investment strategies.Prior to joining Goldman, Noah worked at Citibank and Lehman Brothers. Noah holds an MBA from the Wharton School of Business at the University of Pennsylvania, where he graduated as a Palmer Scholar (top 5% of graduating class). He also holds a BA from McGill University (magna cum laude). Noah is frequently featured in the media including a regular column in the Financial Post and appearances on BNN. This blog originally appeared in the May 2025 issue of the Outcome newsletter and is republished here with permission

Noah Solomon is Chief Investment Officer for Outcome Metric Asset Management Limited Partnership. From 2008 to 2016, Noah was CEO and CIO of GenFund Management Inc. (formerly Genuity Fund Management), where he designed and managed data-driven, statistically-based equity funds. Between 2002 and 2008, Noah was a proprietary trader in the equities division of Goldman Sachs, where he deployed the firm’s capital in several quantitatively-driven investment strategies.Prior to joining Goldman, Noah worked at Citibank and Lehman Brothers. Noah holds an MBA from the Wharton School of Business at the University of Pennsylvania, where he graduated as a Palmer Scholar (top 5% of graduating class). He also holds a BA from McGill University (magna cum laude). Noah is frequently featured in the media including a regular column in the Financial Post and appearances on BNN. This blog originally appeared in the May 2025 issue of the Outcome newsletter and is republished here with permission