By Dina Ting, CFA, Franklin Templeton ETFs

(Sponsor Blog)

It’s that time of year again. Holiday shoppers know the secret: start with a meaningful primary gift that makes an impression. Add smaller delights for a personal touch. Asset allocators can do the same: anchor portfolios with a broad emerging market (EM) core and use dynamic tilts1 for the perfect stocking stuffers.

The broad EM equity rally has now entered a more structurally supportive phase rather than a pure sentiment bounce. EM equities have advanced for 10 straight months, now up more than 30% year to date, outpacing U.S. large caps, which returned slightly less than half that over the same period.2 We believe this outperformance is likely to continue through year‑end amid a weaker US dollar, improving earnings and growing demand for geographic diversification.

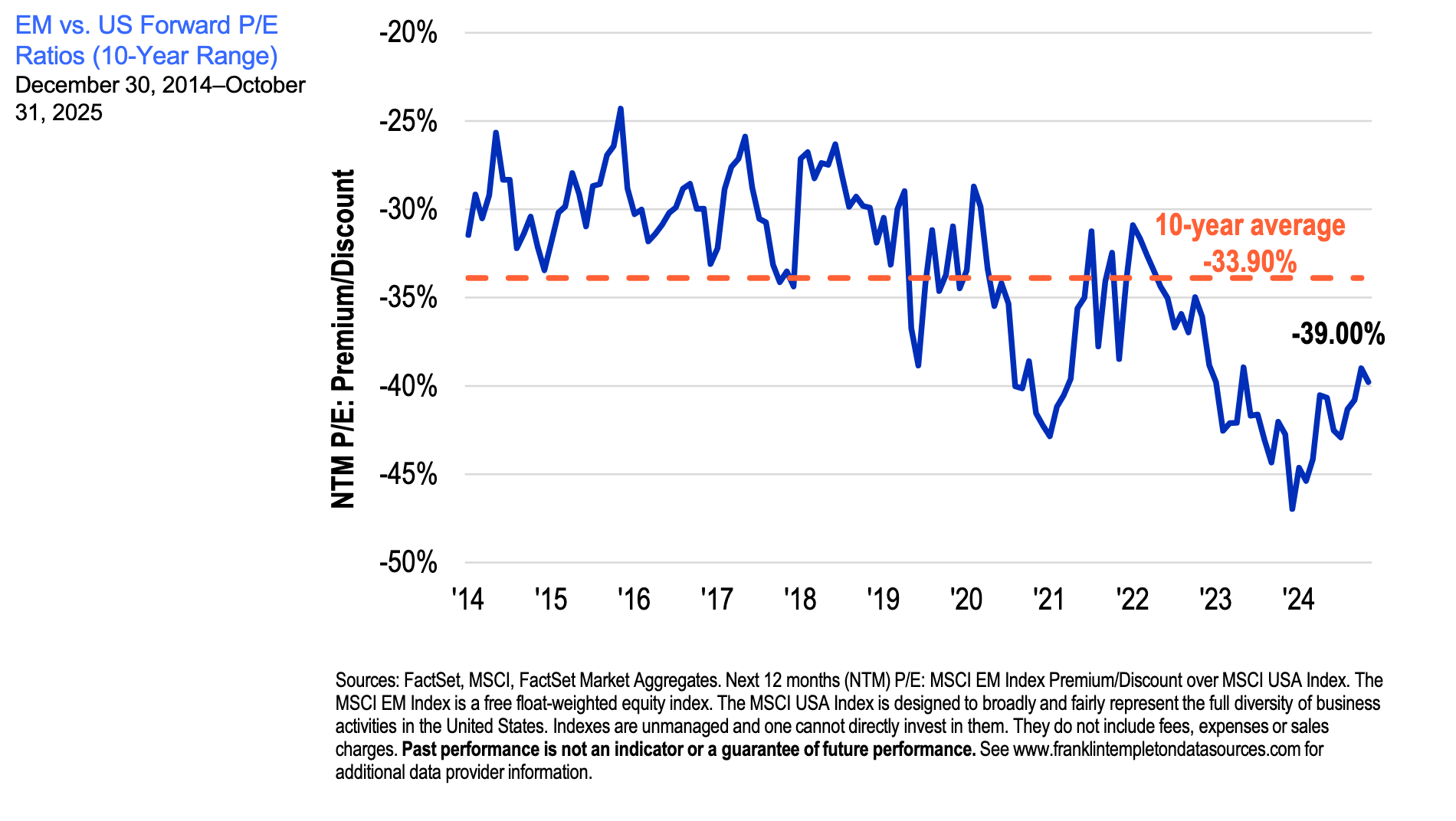

Valuation gaps remain wide: EM equities recently traded at nearly a 40% discount versus US peers: one of their lowest forward price-to-earnings (P/E) differentials in over a decade. Meanwhile, early macro indicators suggest modest expansion among EM manufacturing sectors.

In terms of portfolio construction, a diversified EM allocation anchors exposure to global easing, demographic growth and digital transformation, while selective country tilts reflect conviction-driven opportunities. Such an approach helps investors look beyond short-term noise and stay invested through the macro cycle. With valuations still moderate, we believe the risk-reward for EMs broadly remains compelling.

Why broad core + dynamic tilts works now

Global supply-chain remapping triggered by tariffs has created more stark standouts and laggards across the EM universe and we believe a broad EM core can help capture the multiplicity of growth vectors, while dynamic tilts allow investors to capture standout growth pockets when dispersion widens. South Korea’s equity market, for example, has emerged as a clear leader this year, up nearly 70% year-to-date: the strongest returns for any major market globally.3

This surge has been powered by a combination of AI-driven demand for memory chips, foreign-investor inflows returning after years of under-allocation, and corporate-governance reforms that are helping erase the long-standing “Korea discount.”4

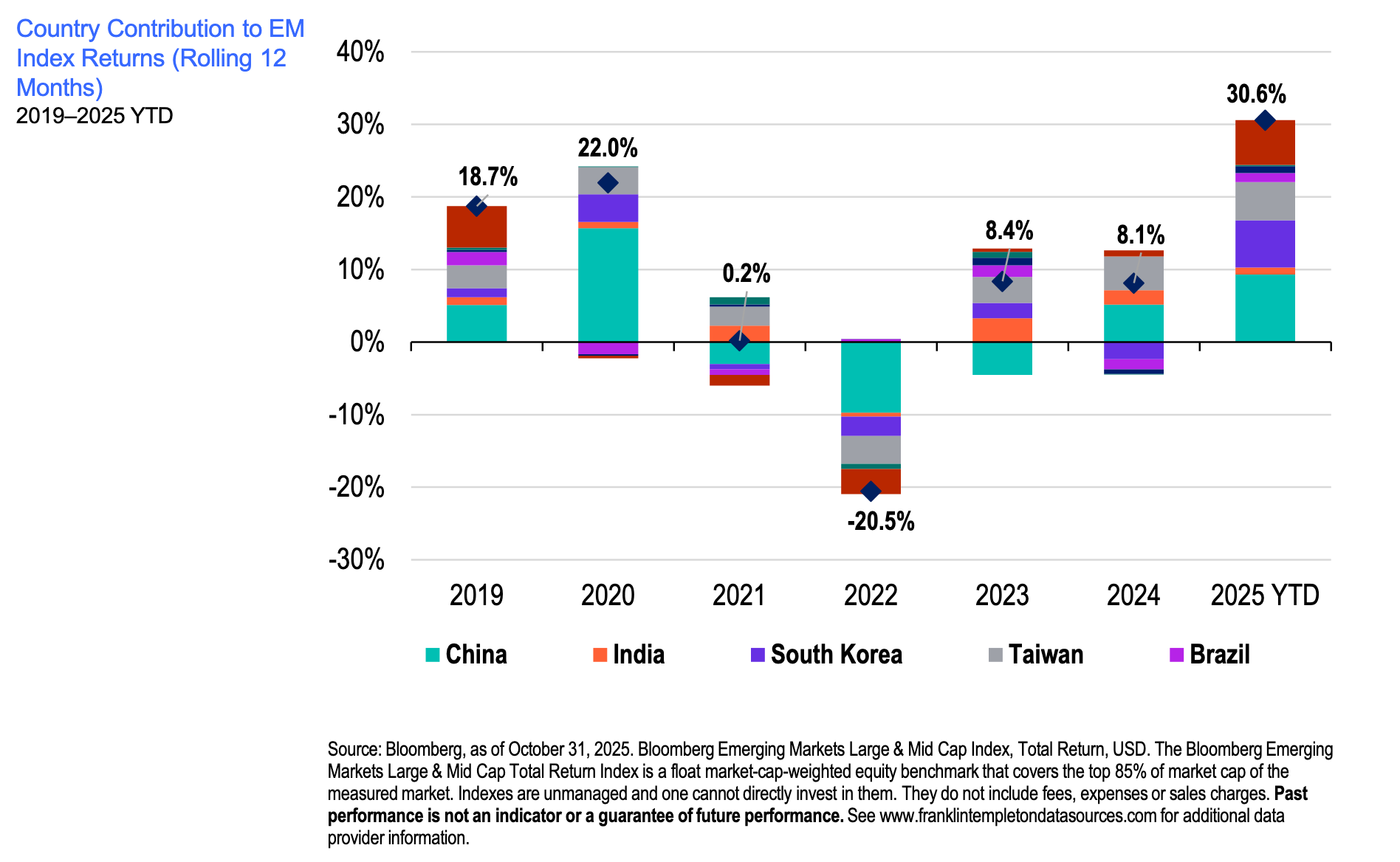

By contrast, China’s contribution has moderated, reflecting slower post-COVID 19 normalization and softer capital inflows. Based on estimates derived from the Brookings/Haver Analytics dataset covering 25 EMs, China’s share of total EM portfolio inflows appears to have fallen: from roughly 40%–50% before the pandemic to below 20% by mid-2025.5This indicates a reallocation of capital toward faster-growing, reform-oriented economies such as India, Mexico and Brazil.

Nonetheless, we believe Beijing’s support of the country’s real-estate sector and injections of liquidity into its equity markets have been notable. Its leaders have adopted a more measured, targeted stance in supporting businesses and consumers, while gradually rebuilding investor confidence. Additionally, the contribution to returns from China — which holds the largest weighting at 32% vs. 10% for South Korea — within emerging market indexes has turned positive, adding 9.3% year-to-date through October 31, 2025.6 This suggests that improving earnings sentiment and valuation support are beginning to reassert China’s role within the broader EM complex.

In markets, as with the holidays, balance matters: A broad EM core potentially provides staying power, while thoughtful tilts can deliver the finishing touch. Together, we believe this approach may help investors turn dispersion into opportunity for the year ahead.

Dina Ting, CFA, is senior vice president and head of Global Index Portfolio Management at Franklin Templeton. Her team is responsible for managing Franklin Templeton’s suite of index-based strategies, including ETFs. Prior to joining the firm in 2015, Ms. Ting spent nearly a decade at BlackRock, where she led the Institutional Emerging Markets team that managed over 70 global equity portfolios for clients worldwide. She also managed a multitude of iShares ETFs covering smart beta, global real estate, sector-based and emerging market strategies. In 2019, Ms. Ting was named one of Money Management Executive’s Top Women in Asset Management and in 2018, she was recognized by the San Francisco Business Times as one of the Most Influential Women in Bay Area Business. She earned a master of science in management science and engineering from Stanford University and holds a bachelor of science degree in industrial engineering from Purdue University. She is a Chartered Financial Analyst (CFA) charterholder.

Endnotes

- Dynamic tilt is an investment strategy that systematically adjusts asset allocation to favor factors or assets that are expected to perform well based on current market conditions, rather than based on a static, long-term allocation.

- Source: Bloomberg, as of November 14, 2025. EM equities measured by the FTSE Emerging Index; US large caps measured by the S&P 500 Index. The FTSE Emerging Index provides investors with a comprehensive means of measuring the performance of the most liquid large- and mid-cap companies in the EMs. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future performance. See www.franklintempletondatasources.com for additional data provider information.

- Source: Bloomberg, as of November 9, 2025. The Korean Composite Stock Price Index (KOSPI) is a series of indexes that track the overall Korean Stock Exchange and its components. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future performance. See www.franklintempletondatasources.com for additional data provider information.

- The Korea discount is the phenomenon where South Korean companies are valued lower than their global peers due to various factors like poor corporate governance, weak shareholder returns and geopolitical risks.

- Source: “Trends in global capital flows to emerging markets.” Brookings Institution. November 5, 2025.

- Source: Bloomberg. The Bloomberg EM Large & Mid Cap Total Return Index is a float market-cap-weighted equity benchmark that covers the top 85% of market cap of the measured market. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future performance. See www.franklintempletondatasources.com for additional data provider information.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

ETFs trade like stocks, fluctuate in market value and may trade above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns. ETF shares may be bought or sold throughout the day at their market price on the exchange on which they are listed. However, there can be no guarantee that an active trading market for ETF shares will be developed or maintained or that their listing will continue or remain unchanged. While the shares of ETFs are tradable on secondary markets, they may not readily trade in all market conditions and may trade at significant discounts in periods of market stress.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Investments in companies in a specific country or region may experience greater volatility than those that are more broadly diversified geographically.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.