By Lorne Marr, LSM Insurance

Special to Financial Independence Hub

Inflation means the prices of everyday things — like food, housing, transportation, and healthcare — increase over time. This reduces the purchasing power of your money and can affect your family’s standard of living. Permanent life insurance can be a powerful tool to help protect your finances against these rising costs.

What type of Life Insurance helps with Inflation?

Permanent life insurance provides lifelong coverage and builds cash value over time. Unlike term life insurance, which only covers a specific period, permanent policies can grow in value and death benefit, helping your family maintain financial security despite inflation.

Main types of permanent life insurance:

- Whole Life Insurance

- Provides a guaranteed death benefit and builds cash value.

- Participating whole life policies pay dividends, which can buy Paid-Up Additions (PUAs)—small increments of additional insurance that increase both death benefit and cash value.

- Universal Life Insurance (UL)

- Flexible premiums and death benefits.

- Option to choose a level death benefit or an increasing death benefit to keep up with inflation.

There are three main ways permanent life insurance can protect you against inflation:

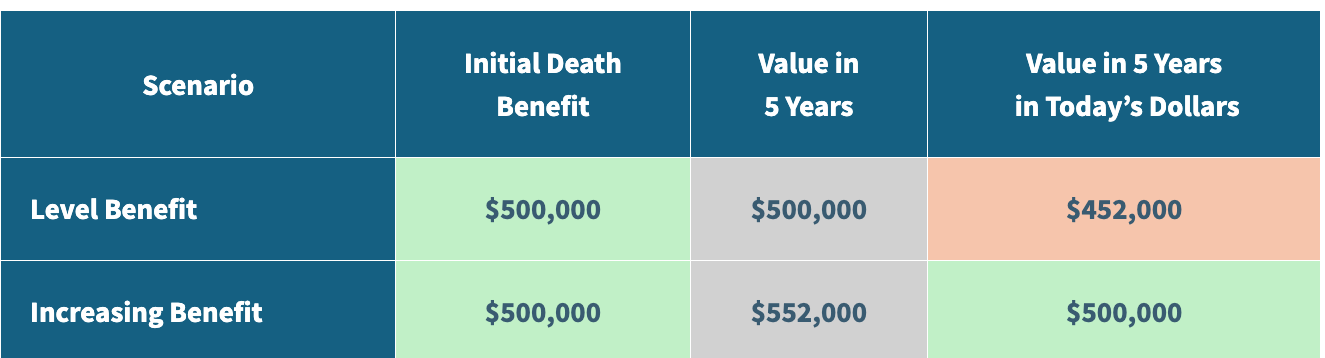

1. Inflation Protection through Increasing Death Benefit Option in Universal Life Policies

How it works: Your death benefit can grow over time to match inflation.

Example (2% inflation):

By choosing an increasing death benefit, your coverage keeps pace with inflation, preserving purchasing power for your family.

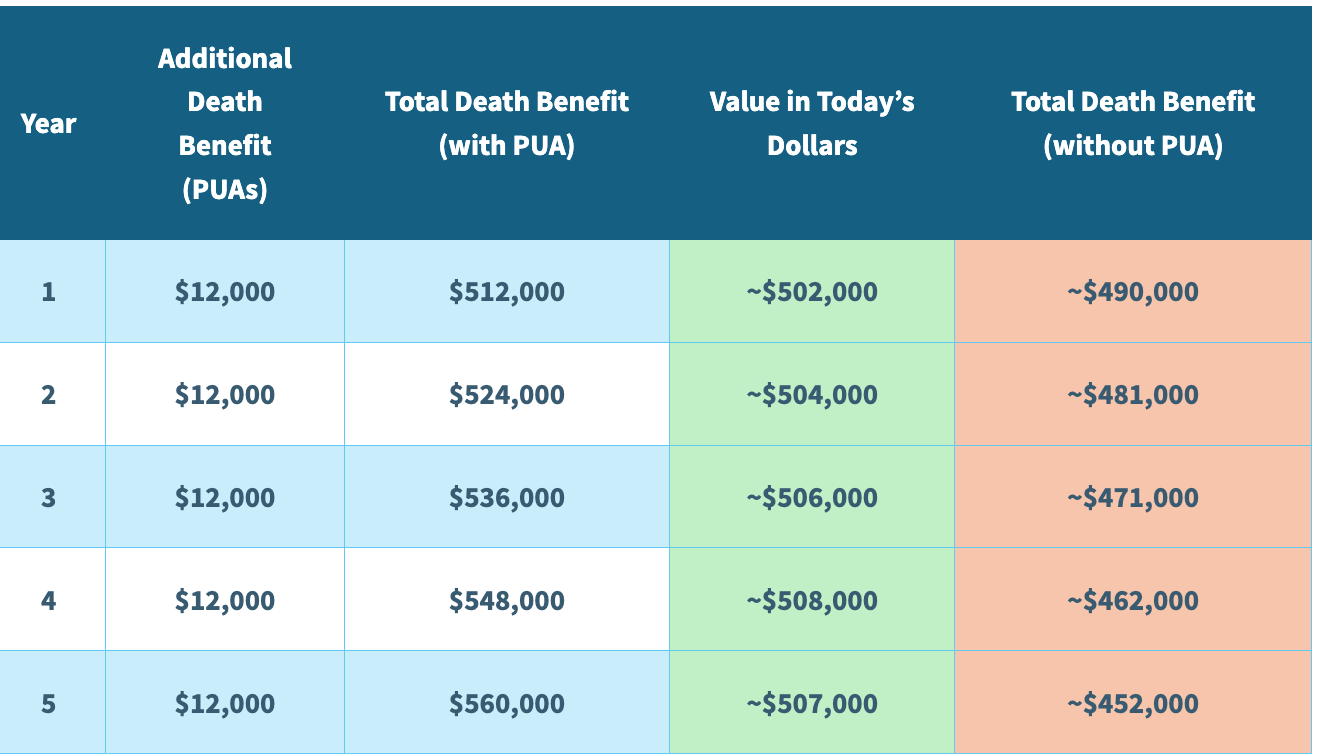

2. Inflation Protection through Participating Whole Life Insurance and Paid-Up Additions

How it works: Dividends from a participating whole life policy can purchase Paid-Up Additions (PUAs), increasing both death benefit and cash value over time.

Example (2% inflation, PUAs $12,000/year):

With 2% inflation, the original $500,000 loses value to $452,000 in today’s dollars. PUAs grow your policy above this, effectively protecting your family against inflation.

3. Inflation Protection through Accumulation Fund Growth

How it works: Both Universal Life and Whole Life policies accumulate cash value, which grows tax-deferred and can be accessed via withdrawals or loans.

Example (cash value $50,000 after 5 years, 2% inflation):

- Inflation reduces the purchasing power of money by roughly 10% over 5 years.

- The $50,000 cash value can be used to cover higher living costs, helping maintain financial stability.

Conclusion

Permanent life insurance — whether Whole Life Insurance or Universal Life Insurance — can help your family maintain financial security in the face of rising costs. Increasing death benefits, Paid-Up Additions, and growing cash value ensure your coverage keeps pace with inflation.

To get the best savings on life insurance, it is crucial to work with an independent broker who has access to policies from multiple providers. Our life insurance specialists can offer you a broader range of insurance solutions than most other brokers, allowing us to navigate through various options to find ways to reduce your costs effectively. By working with us, you benefit from our expertise in identifying and leveraging different strategies to lower your premiums.

To start, simply complete a life insurance quote on the sidebar for an initial, non-committal discussion, and let us help you explore the best opportunities for savings.

Lorne Marr has been in the Life Insurance Industry for 30 years and is the Director of Business Development at Hub Financial as well as the Founder of LSMInsurance.ca and FitInsure.ca. This blog originally appeared there on Dec. 23, 2025 and is republished here with permission.

Lorne Marr has been in the Life Insurance Industry for 30 years and is the Director of Business Development at Hub Financial as well as the Founder of LSMInsurance.ca and FitInsure.ca. This blog originally appeared there on Dec. 23, 2025 and is republished here with permission.