By Robb Engen, Boomer & Echo

Special to the Financial Independence Hub

Canadians have few reasons to save these days. Cheap borrowing coupled with feeble returns on your savings deposits makes it hardly seem worthwhile to park your cash in a savings account. Some banks have decided to punish savers even further by charging fees just for moving your money around.

Gaining Momentum Through Inertia

But one bank has turned to the carrot rather than the stick approach to help its customers save. Scotiabank, which already boasts the best suite of rewards credit cards, in addition to its Moneyback chequing account, has raised the stakes with a new high-interest savings product called the Momentum Savings Account. Here’s how it works:

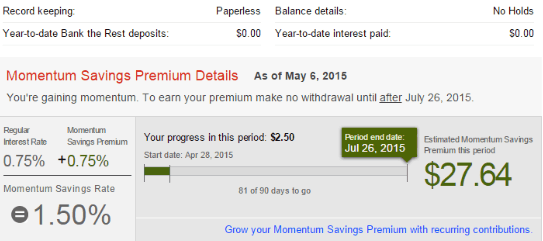

Using a unique incentive that rewards “inaction”, or our tendency to drift toward financial inertia, the Scotiabank Momentum Savings Account pays a bonus interest rate for customers who do not make a withdrawal in a 90-day period.

The account pays regular interest of 0.75 percent when you keep a balance of $5,000 or more. If you resist the temptation to withdraw from your account for 90-days, you’ll receive a 0.75 percent bonus, for a total interest rate of 1.5 percent.

Customers who open an account by June 15th, 2015 will get an additional 0.5 percent bonus, for a total of up to 2 percent until July 31st, 2015.

Momentum Savings also comes with an “Account Tracker” that customers can access online and through their mobile app. It provides a visual “countdown” to the extra interest payment, so you can see when you’ll receive the extra interest. With this tool, you can be strategic about when to withdraw from the account to ensure maximum savings.