By Ahmed Farooq, CFP, CIMA, Franklin Templeton Canada

(Sponsor Content)

ESG (environmental, governance and social) has become a hot topic in investment circles.

Sustainable investing is a key consideration for most asset managers nowadays, reflecting changing attitudes among investors.

Responsible or sustainable investing was once a very niche part of the market, but now accounts for US$35.3 trillion worldwide, according to recent data from The Global Sustainable Investment Alliance (GSIA).

This rise of ESG is most closely associated with equities, but this approach to investing can also be applied in the fixed income space too. Being able to minimize downside risk is a key objective for fixed income investors, and this certainly aligns with the characteristics of ESG investing.

Green Bonds evidence of ESG’s growing significance

ESG’s growing significance was displayed further earlier this year when the federal government’s 2021 budget included a plan to issue $5 billion in green bonds to support environmental infrastructure development in Canada.

Speaking at the recent Exchange Traded Forum, Brandywine Global Investment Specialist Katie Klingensmith discussed the firm’s investment philosophy and how ESG has become an important element of its strategies in recent years.

One of the specialist investment managers brought under the Franklin Templeton umbrella after its acquisition of Legg Mason in 2020, Brandywine Global has US$67 billion in assets under management globally.1

Of that total AUM, US$53 billion is in fixed income, where the investment team combines a global macro perspective with a disciplined value approach to select suitable holdings for the Brandywine funds.

A signatory of the UN-supported Principles for Responsible Investment (PRI) since 2016, approximately 99% of the firm’s assets under management now feature ESG integration.

Brandywine has built its own proprietary ESG portfolio management dashboard as a result, and will publish its first Annual Stewardship Report in 2021. Continue Reading…

Talk of stagflation is all the rage. Sort of. Most of the articles I read about the subject focus primarily, if not exclusively on inflation.

Where’s the ‘stag’ part? The word ‘stagflation’ is a handy portmanteau that came about in the 1970s when, for the first time in modern history, we experienced stagnant economic growth coupled with high and persistent inflation. Those two circumstances were thought to be mutually exclusive. In fact, they represent the worse of both worlds. Normally, if the economy is stagnant, there’s no inflation. Alternatively, if there’s inflation, it was always assumed that it was because the economy was overheating and growing too quickly.

In the second half of 2021, it seems everyone is piling on the stagflation narrative. Nouriel Roubini of NYU was talking about the circumstances being right for stagflation more than a year ago already, but it was only around the middle of 2021 that a narrative like his began to gain traction.

Lynchpin is Inflation

The lynchpin of the story is inflation. Everyone has a view on whether it is transitory or not, even as no one can really deny that we’ve already experienced more inflation for longer in the past 7 or 8 months than in any period in modern history. I’m more worried about stagnant growth, yet far fewer people seem inclined to openly share that concern. Continue Reading…

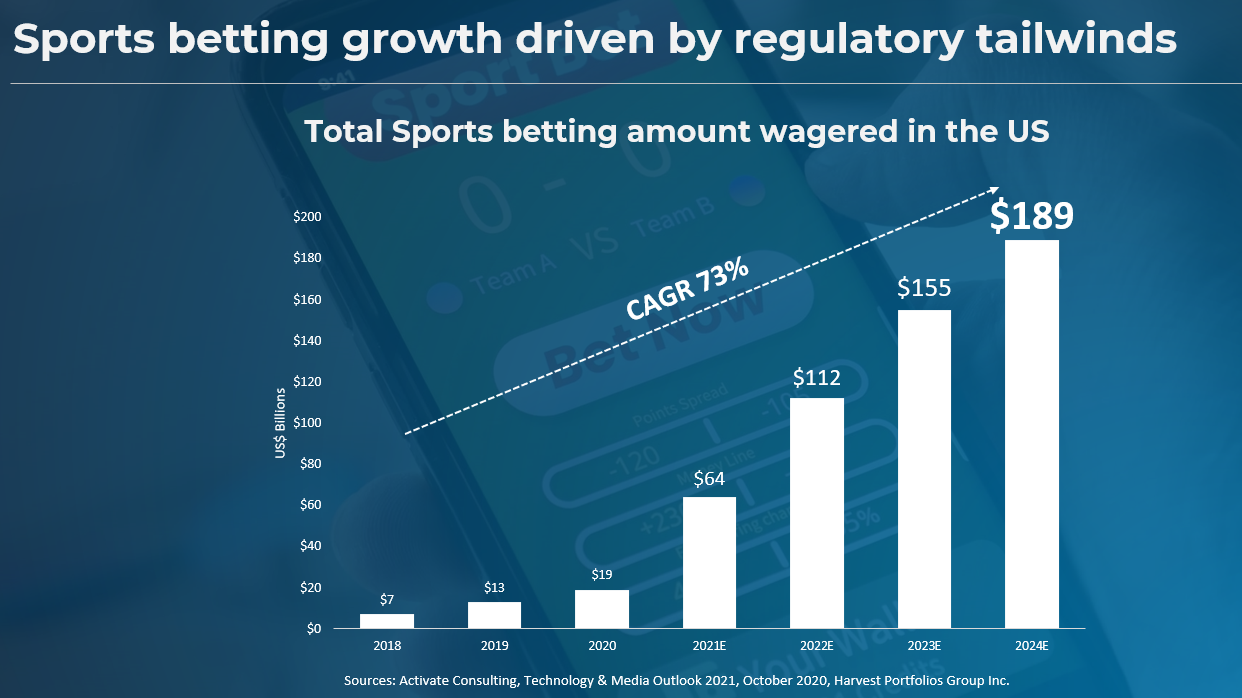

The global sports industry is worth between US$400 to $500 billion a year and in the five years leading up to the pandemic in 2020 had been growing at an annual rate of 14%, according to NewZoo.

The industry is far more than professional teams in hockey, football, baseball and basketball. These North American favourites are dwarfed by soccer which is the world’s most popular games.

When it comes to pro teams, in addition to game tickets, fans buy branded merchandise and play in fantasy leagues. The teams earn more TV revenues as they advance in playoffs. But sports business is more than that. It also involves online gaming, gaming software developers and internet sports gambling. These last areas are large and rapidly growing. While the United States is the world’s largest sports market, China and other parts of Asia are emerging as leaders in eGaming and iGambling.

In the interview below, Harvest CEO Michael Kovacs discusses the ETF, the sector’s outlook and how the ETF aligns with the Harvest philosophy of creating value through ownership of the best global businesses.

Financial Independence Hub [The Hub henceforth]: Why did you launch the Harvest Digital Sports & Entertainment Index ETF?

Michael Kovacs [MK henceforth]: Sports entertainment is a global industry with great growth characteristics. It is regaining a foothold after more than a year of empty stadiums and lost revenues. At the same time, there have been bright spots, including new forms of sports entertainment such as online gaming and internet gambling where the pandemic has been a catalyst.

At Harvest, we seek to identify trends like this. Sports is one that continues to grow globally and also offers reopening opportunities as the pandemic issues decline.

The Hub: How is the ETF designed?

MK: It is passively managed ETF with 40 global stocks that follows the Solactive Sports & Entertainment Index. The companies are publicly traded, mostly in North America, with some in Europe. The ETF is diversified across five areas of the sporting world, with different weightings for each area. It is rebalanced quarterly.

The Hub: What is the strategy?

MK: As mentioned, the ETF is diversified to capture all segments of the industry. Professional sports organizations make up five of the 40 holdings, or 12.5%. There are a number that either trade under their own name or as part of companies that own them. The English soccer team Manchester United Plc is one example. It is one of the game’s strongest brands. It is listed in New York and has a market capitalization of about US$2.7 billion. Another example is Liberty Media-Liberty Formula One. which trades on Nasdaq. It owns the Formula 1 racing and has a market cap of US $18 billion. Madison Square Gardens Sports Corp. is another. It owns the New York Rangers of the NHL and the NBA’s New York Knicks. It has a market cap of US $4.5 billion. These are examples of some of the great sporting franchises out there.

The Hub: Are event and ticket companies and sports equipment and apparel companies another component?

MK: Yes, they are. Together they are about 38% of the ETF. Ticketing makes up five holdings or 12.5%. There are a lot of companies that people would recognize. Live Nation Entertainment Inc. owns the familiar ticketing company, Ticketmaster. Live Nation is a global company that manages ticket sales and resales and also owns and operates entertainment venues and manages careers. In fact, they own and operate several of the premier venues that many Canadians have attended concerts and events.

Sports equipment and apparel is another 10 holdings or 25% of the ETF. Again, many of the companies are household names. Nike Inc. is a global leader in the manufacture and marketing of athletic shoes, branded clothes and equipment. It also sells baseball bats and balls, tennis rackets and golf clubs. Nike’s annual revenues are more than US $18 billion.Adidas which is the second largest global sports apparel company after Nike, owns Reebok and part of the German soccer club Bayern München. Cross ownership like this gives these companies incredible brand power. Continue Reading…

In Part One of this series we mentioned how ‘living in the moment’ — that is being free of ideas of self and the things we wish for — is an opportunity for happiness.

In this part we will first explain how happiness comes from our thoughts, not our financial circumstances, and how making money usually generates more happiness than spending it does. We will then look at how money can buy happiness when you give it away, and how it’s not enough to manage money wisely: we also have to use our money wisely.

For example, let’s imagine two people with the same size investment portfolio living in almost identical apartments. In one case, the individual who may have experienced a windfall is overjoyed to be living on his or her own, while the other person, who may have suffered a financial loss, is sad and embarrassed to now be living in such a small apartment. One person is happy and one is sad. The difference is not based on their different circumstances it is entirely based on their thoughts about their situation.

In his book, The Art of Happiness, Dalai Lama says, “Once basic needs are met – the message is clear: We don’t need more money, we don’t need greater success or fame, we don’t need the perfect body or the perfect mate – right now, at this very moment, we have a mind, which is all the basic equipment we need to achieve complete happiness.”

Overcoming challenges

For most successful people, it’s their accomplishments that gives them the greatest happiness, whether that includes looking after their family, accumulating wealth, or showing resilience and problem solving through difficult situations. Successful people know that a happy life is not a life without problems or negative circumstances: rather it is one where we have the opportunity to overcome challenges and problems.

It’s important to realize that most often, the greater the challenge, the greater the happiness that comes from overcoming it. If parents make things so easy for their children that they never have to work hard and learn to overcome challenges, (including financial challenges) their children may not develop the positive self-image and confidence that comes from solving problems and creating their own financial security. Continue Reading…

Historically, investors have held bonds to diversify and mitigate the volatility of their portfolios. Conventional portfolios have sufficient allocations to low-volatility bonds to weather periodic bear markets in stocks. During the tech-wreck of 2000-02, the global financial crisis of 2007, and the Covid-crash of early 2020, bonds not only held up well relative to stocks, but actually produced gains, mitigating the pain investors experienced from large declines in stocks.

Over the past few decades, bonds have not only provided ample protection from bear markets in equities but have also provided reasonable returns for the privilege. During the 40 years from 1982 to 2020, 10-year U.S. Treasuries produced an average annualized real return of 4.71%.

The Ugly Truth

By any measure, the bond market’s one-two punch of healthy returns and portfolio insurance over the past several decades has been impressive. However, this experience has been highly anomalous from a long-term historical perspective.

The 4.71% annualized real return of 10-year U.S. Treasuries over the 40 years from 1981 to 2020 compares favorably to the corresponding return of only 1.36% for the 80 years beginning in 1941. Their returns over the past four decades look even more out of place when compared to -1.89% annualized real return for the 40 years from 1941 to 1980.

Bonds can also be less stable than stocks and just as vulnerable to extreme losses. Since 1928, the maximum peak-trough loss in real terms of 10-year U.S. Treasuries was -54.3% vs. -56.5% for stocks. Over the same time period, the worst rolling 10-year annualized real return for 10-year Treasuries was -4.7% as compared to -4.06% for the S&P 500 Index.

Bond bear markets can also last longer than those of stocks. Investors who bought Treasuries at the end of 1940 had to wait 51 years before they broke even in real terms. By contrast, the lengthiest period in which stocks remained underwater was the 13 years following the peak of the technology bubble in late 1999.

The current near-zero yields on bonds are likely to be an excellent indicator of what investors can anticipate for future returns. John Bogle, founder of The Vanguard Group, pointed out that since 1926, the yield on 10-year U.S. Treasury notes explains 92% of the annualized returns investors would have earned had they held the notes to maturity and reinvested the interest payments at prevailing rates.

The perils of investing in bonds are well summarized by legendary investor Warren Buffett, who in his 2012 annual letter to Berkshire Hathaway shareholders warned:

They are among the most dangerous of assets. Over the past century these instruments have destroyed the purchasing power of investors in many countries, even as these holders continued to receive timely payments of interest and principal …. Right now, bonds should come with a warning label.

History also cautions against relying on bonds to mitigate portfolio losses when stocks decline. Notwithstanding that bonds provided much needed gains during the tech-wreck of 2000-2002, the global financial crisis of 2008, and the Covid-crash of 2020, stocks and bonds have been positively correlated in 55% of the 93 years from 1928 to 2020.

Putting history aside, the simple fact is that with current short-term rates at zero and 10-year Treasuries yielding 1.5%, it will be difficult for bonds to provide the same degree of protection (if any) in the next bear market. The math just doesn’t work!

From the beginning of 1928 through the end of last year, the annualized real return of the S&P 500 Index was 6.64%, as compared to 1.94% for 10-year Treasuries. Had you invested $1 in the S&P 500 at the beginning of 1928, by the end of 2020 it would have had an inflation-adjusted value of $396.03 vs. only $5.96 had you invested the same $1 in 10-year Treasuries. Put simply, the opportunity cost of maintaining a permanent allocation to bonds cannot be overstated.

Does this mean Bond Investors are Irrational?

The massive drag on portfolio returns over the long-term caused by a permanent allocation to bonds does not necessarily imply that investors who hold them are irrational.

Many investors may not have a sufficiently long investment horizon to weather crushing losses in bear markets and/or may be emotionally incapable of enduring large losses that can occur in portfolios that are heavily weighted in stocks. Continue Reading…