By Dale Roberts, CutTheCrap Investing, Retirement Club

Special to Financial Independence Hub

The following is a special to Findependence Hub. This post is derived from a newsletter from Retirement Club for Canadians, re-shaped and enhanced for this audience.

Retirees typically face the greatest risk in the first few years of retirement. A severe market correction or bout of inflation can permanently impair retirement plans. In fact, the risk for retirees starts several years before the retirement start date, they’re already in the retirement risk zone.

Norm suggested …

“Planning for retirement is tricky at the best of times because it is beset by uncertainties both known and unknowable. High valuations are one of the known problems but that doesn’t make them easy to deal with.”

While a severe market correction early in retirement is a great risk for retirees who will rely extensively on balanced or growth-oriented portfolios, a longer period of low returns can also create risk. The U.S. stock market is trading at worrying levels based on a variety of value factors.

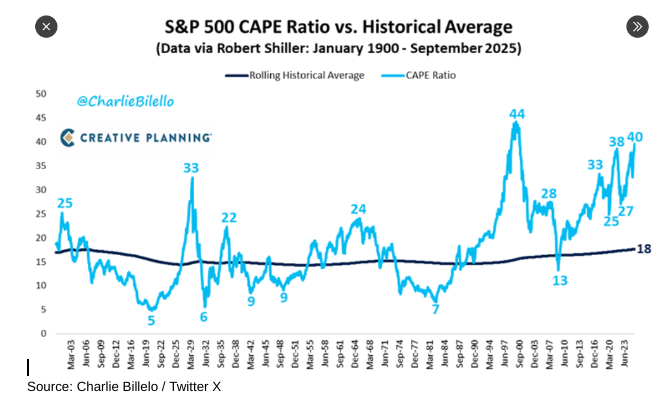

Norm demonstrated that the S&P 500 Index is trading at a cyclically adjusted price-to-earnings ratio near 39, which is approaching the 44 level that we saw in late 1999 as we approached the dot com crash.

Source: Charlie Billelo / Twitter X

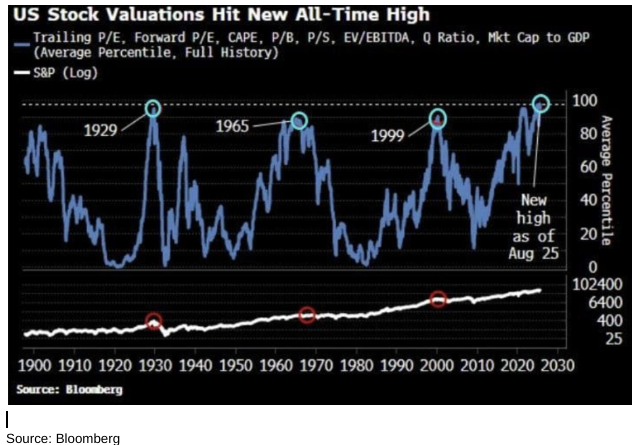

The price-to-sales ratio is approaching its 1999 high.

This ‘everything metric’ says we have the most expensive U.S. market – EVER!

We certainly can’t just step aside and wait for the next recession. Valuation metrics provide no market-timing opportunity. Nothing provides any market timing opportunity. Valuation tends to be a poor near-term market predictor, but it can ‘predict’ the potential returns over the next several years to decade. The data suggest returns for U.S. stocks could be very low in the range of 1-4% annual or even negative in real dollar (inflation-adjusted) returns.

And keep in mind that Canadian stocks (after a very healthy run) are expensive as well. After their big run-up this year, Canadian stocks now trade for nearly 29 times their average inflation-adjusted earnings of the past decade, according to Citigroup, the historical average is 16, TSX returns over the next several years might be challenged as well.

So, there is a risk of a major correction inspired by the lofty levels. And low returns in the first decade can put a strain on the spending plans. Continue Reading…

I’d gladly lose me to find you

I’d gladly give up all I have

To find you, I’d suffer anything and be glad

I’ll pay any price just to get you

I’d work all my life, and I wi

To win you, I’d stand naked, stoned and stabbed

I call that a bargain

The best I ever had

Bargain, by The Who

By Noah Solomon

Special to Financial Independence Hub

Many investors could be forgiven for believing that U.S. stocks are a superior investment to their non-US counterparts. Since the global financial crisis, U.S. stocks have not merely outperformed those of other countries: they have trounced them. Over the past fifteen years, the S&P 500 outpaced other developed market equities by a cumulative 150%.

Notwithstanding this astounding outperformance, successful investing necessitates looking ahead. To assess the likelihood that U.S. stocks will continue to outperform, it is important to (1) analyze the drivers of their past outperformance, and (2) determine the future sustainability of these drivers.

Not as Exceptional as you might think

Over the past decade, U.S. companies have delivered stronger earnings growth than those in other countries. However, given the degree to which their share prices have outperformed, the magnitude of their excess earnings growth is far less than one might suspect. Over the past ten years, American company earnings have outpaced those of foreign companies by a meagre 3.8% on a cumulative basis. Moreover, this excess growth was concentrated in the first part of the decade, with U.S. companies growing their earnings at the same clip as their non-U.S. peers from 2020-2024.

Not only has U.S. earnings growth been undifferentiated over the past five years, but it has achieved this mediocrity due to the stellar growth of a small handful of mega-cap tech stocks. Between 2020-2024, the magnificent six (Tesla was not in the index at the end of 2019), which collectively represent a 32% weight in the S&P 500 Index, grew their earnings at an extraordinary, annualized pace of over 20%. Given that the aggregate U.S. earnings growth, which was bolstered by a handful of mega-cap growth companies, has been undifferentiated, it follows that most U.S. companies have been subpar vs. the rest of the world from a fundamental perspective.

Despite relatively weak earnings growth from a global perspective, the non-magnificent 68% of S&P 500 companies nonetheless trade at a significant premium to their non-U.S. peers. Going forward, unless these companies can produce greater earnings growth than those in other regions, their relatively elevated valuations are not fundamentally justified. Moreover, there are several reasons to suspect that that U.S. companies will fail to grow their earnings faster than those in other regions.

Firstly, the U.S. administration’s imposition of tariffs on its trading partners will inevitably raise costs for American companies and reduce the global competitiveness of goods produced in the U.S. Even in rare instances where U.S. companies are successful in passing through these increased costs to their customers, their profits will nonetheless suffer from lower volumes. In addition, recent developments in U.S. immigration policies will reduce the supply of labour, which will hinder economic growth. Lastly, continued policy uncertainty is likely to engender a “wait and see” mode among CEOs, thereby leading to lower levels of investment.

The Magnificence is Evolving

Even if the non-magnificent majority of U.S. stocks fail to deliver the superior earnings growth that is required to justify their relatively high valuations, there is always a possibility that the magnificent minority could save the day by delivering earnings that exceed expectations. At an aggregate valuation of 30 times forward earnings, magnificence does not come cheap. However, if these companies can continue growing their earnings at their historic pace, their valuations are sufficiently reasonable to allow for strong gains in their stock prices. Conversely, if their growth reverts to less magnificent levels, the ensuing capital losses could be substantial.

One of the key drivers of the magnificent Six’s success has been their ability to grow their earnings at a breakneck pace with far smaller amounts of investment than what has been required of past behemoths. However, they have been aggressively ramping up investment in response to the current AI gold rush. While it is possible that these investments will produce strong returns, the fact remains that the low investment/high growth dynamic which has been a key element of the magnificent six’s magnificence may be a thing of the past.

Have I got a Deal for You

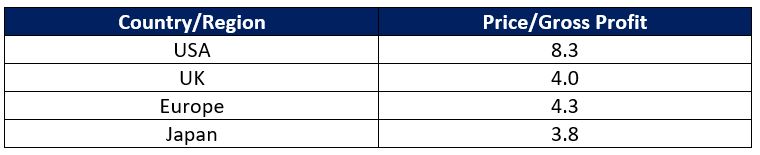

Given that U.S. companies have experienced similar earnings growth as their global peers, it follows that the former’s outperformance has been driven primarily by greater multiple expansion, which has resulted in U.S. P/E ratios that currently stand in the 90th percentile of their historical range. Relatedly, the earnings yield on U.S. stocks is close to an all-time low relative to Treasury yields. In contrast, international stocks are currently valued at a historically large discount to their U.S. counterparts.

Price/Gross Profit by Region

Admittedly, it is possible for valuations to become even more stretched in the short term, and timing markets perfectly is an exercise in futility. However, history strongly suggests that higher valuations foreshadow below average returns over the medium-to-long term. Moreover, in the absence of any compelling argument that future profit growth of U.S. vs. non-U.S. companies will be meaningfully different, the latter appear to be a relative bargain. Continue Reading…

Retirement income management and Required Minimum Distributions (RMDs) can be complex topics for many Americans. This article presents effective strategies to help readers navigate these financial challenges. Drawing on insights from financial experts, the following tips offer practical approaches to optimize retirement income and manage RMDs efficiently.

Purchase Annuity for Guaranteed Retirement Income

Leverage Qualified Charitable Distributions for RMDs

Optimize Asset Location for Tax-Efficient RMDs

Consider Annuities for Steady Retirement Income

Use Trusts to Manage RMDs Strategically

Convert to Roth During Market Downturns

Implement Bucket Approach with Beneficiary Designations

Start Home-Based Business to Offset RMDs

Purchase Annuity for Guaranteed Retirement Income

It is important to always consider broader planning needs, but one strategy that can be useful for generating retirement income and managing required minimum distributions (RMDs) is purchasing an annuity. This annuity would be purchased within an IRA and would create a level stream of guaranteed income for the rest of one’s retirement. This will not only satisfy one’s RMDs, but it can also lower taxes by stretching income across many years. In particular, it could help avoid large, irregular distributions that might push one into higher tax brackets. — Aaron Brask, Retirement planner, Aaron Brask Capital LLC

Leverage Qualified Charitable Distributions for RMDs

The obvious choice is to find a part-time job that aligns with your passion. This way, you can generate income and get paid to enjoy your favorite hobby. For example, if you love golfing, getting a part-time job at a golf course may give you discounts or even free games.

As far as managing RMDs, the amount that you must distribute is not determined by your income. It is based on the value of your Traditional IRA at the end of the year and the IRS Uniform Lifetime Table or Joint Life and Last Survivor Table.

This doesn’t include Roth IRAs. There are no RMDs in these accounts.

The best way to manage the increase in income, which can lower benefits such as Social Security or Medicare Part B (which are based on annual income), is to leverage Qualified Charitable Distributions (QCDs) for those who are philanthropic or give to a 501(c)(3) religious institution such as tithing.

When you reach the age to take RMDs, you can directly give to your favorite charity without incurring the tax implication or the increase in income that comes with RMD distributions. In 2025, you can donate up to US$108,000.

This will eliminate the RMD from being counted in your gross income and, at the same time, qualify for satisfying your annual distribution requirement.

I think this is useful because their favorite cause still receives donations, they satisfy their RMD, and they don’t have to pay the taxes up to that amount.

After 15+ years managing corporate finances and helping businesses with cash flow optimization, I’ve seen how asset location strategy can be a game-changer for Required Minimum Distribution (RMD) management. The approach involves strategically placing different types of investments across taxable, tax-deferred, and tax-free accounts to minimize the tax impact when RMDs hit.

I worked with a client in the software technology space who had accumulated significant wealth through stock options and 401(k) contributions. We repositioned his bond holdings and REITs into his traditional IRA while moving growth stocks to his Roth accounts. When his RMDs started, he was pulling from bond interest and dividend income rather than forcing the sale of appreciating assets.

The key insight from my Financial Planning and Analysis (FP&A) background is treating this like portfolio optimization: you’re maximizing after-tax income rather than pre-tax returns. His RMD tax bill dropped by 18% because we were distributing lower-growth, income-generating assets instead of his high-performing tech stocks.

This works especially well for anyone with diverse investment types across multiple account structures. The planning needs to start at least 5-7 years before RMDs begin, but the tax savings compound significantly over time. — Michael J. Spitz, Principal, SPITZ CPA

Consider Annuities for Steady Retirement Income

Although annuities are often a source of debate and critique, they are still a functional and conservative way to generate income in retirement. If set up early enough, the steady income can often account for Required Minimum Distributions (RMDs) across all Individual Retirement Account (IRA) assets since the withdrawal rates are higher than the often quoted 4-4.5%. — Pedro Silva, Financial Advisor, Apex Investment Group, LLC

Use Trusts to Manage RMDs Strategically

After 25 years of helping clients navigate estate planning and witnessing countless families deal with Required Minimum Distribution (RMD) challenges, I’ve discovered the most effective strategy: creating an offshore Asset Protection Trust that feeds into a domestic charitable remainder trust for your RMDs. While this may sound complex, it’s incredibly powerful for the right situation.

Here’s how it works: I had a client with US$2.3 million in retirement accounts who was facing substantial RMDs that would push him into the highest tax brackets. We transferred a portion of his Individual Retirement Account (IRA) into a charitable remainder trust, which allowed him to take his RMDs as annuity payments over 20 years at a much lower effective tax rate. The added benefit? The remainder goes to charity, providing him with immediate tax deductions that offset other income. Continue Reading…

I enjoy posting retirement income case studies on this site, so let’s jump right in: can my readers retire using a 60/40 portfolio?

I believe they can.

Can you retire using a 60/40 portfolio?

As mentioned on this site many times over the years, retirement income planning is a puzzle for some. Not all retirees will have more income generated from their portfolio than what their annual expenses are … although that is probably ideal for some.

That said, it is possible (although rare) to save too much for retirement – if you rely on general assumptions to calculate how much you’ll need.

A good example is your retirement income replacement rate.

The replacement rate is the percentage of the pre-retirement income you need to maintain your standard of living in retirement. I believe overestimating this rate can cause you to save more than what you need for retirement spending.

A general rule shared by some experts is you’ll need between 70-80% of your current income to maintain a comfortable lifestyle in retirement. This is because once saving for retirement is done, and paying off any debt prior to retirement, those pre-retirement expenses drop off.

Spending 50% of your pre-retirement income is likely a MUCH different number for you and I, vs. 80%.

Retirement rules of thumb are interesting for back-of-the-napkin fun but they have no value in any detailed income planning work. Which makes the following simple but essential IMO in your retirement income planning steps:

Step 1: What are your spending goals?

Step 2: What are your investment savings and income sources to meet those needs?

Step 3: What is the bare minimum lifestyle that you’re ready to live off?

My reader, Olin (name changed) is single and wants to semi-retire this summer at age 55. He has no children or dependants. He’s had a good paying job over the years as a graphic designer but wants to take more of his artistry on the road in the coming years… He performs at various music gigs during the year for hobby/travel income.

After reading my site, including some MoneySense Best ETFs in Canada editions over the years, he’s landed on a comfortable 60/40 stock/fixed income portfolio across his accounts: that matches his tolerance for investing risk but also seeks to simplify how he invests for his retirement: in a single low-cost all-in-one ETF.

Olin appreciates and respects the dividend income journey by many bloggers but Olin doesn’t have enough money saved up to generate tens of thousands in dividend or distribution income from his portfolio without taking on higher risk bets: so he wants to rely on more of a total-return approach. This should work out well for him based on some historical research and trending.

As a student of market history, Olin is well aware instead of living off dividends or distributions, he could simply sell-off assets as he ages to meet his lifestyle needs. While that approach has some risks as well, depleting your capital over time, Olin is also very confident he could scale-up or scale-down discretionary spending in semi-retirement at will: he will spend more in “good years” and curtail some spending in “bad years.” Being variable with his spending should allow for even greater financial flexibility since he remains out of debt and mortgage-free.

Leveraging some Vanguard research I presented at an Ottawa Share Club meeting in May, 60/40 stock/fixed income portfolios have been very reliable, pension-like constructs for years.

While the financial future is always uncertain, there is nothing to suggest a global mix of stocks + a decent weight of fixed income shouldn’t deliver similar results: balancing risk and reward in the decades ahead.

Can my reader Olin retire using a 60/40 portfolio?

Here are Olin’s inputs and assumptions as part of this case study:

Olin, single, age 55 later this year – wants to semi-retire summer 2025. He makes $80,000 (gross).

He wants to spend > $50,000 after-tax starting this summer.

He loves travel, and will take his guitar with him! He has determined he wants some “go-go” spending years between ages 55-79 and will have “slower-go” spending years after age 80.

Olin has no workplace pension.

He has no debt. He owns his townhome in Ottawa worth about ~ $750,000. Continue Reading…

Some investors do just fine on their own. But what if that is not you, and you are only realizing it now?

Canva Custom Creation: Lowrie Financial

By Steve Lowrie, CFA

Special to Financial Independence Hub

Let us get something out of the way upfront.

Many do-it-yourself (DIY) investors do not need an advisor. They enjoy the process. They understand the risks and they successfully meet their needs over time.

Also true: many people who work with an advisor could probably manage their investments on their own but choose not to. They are looking for structure, coaching, planning strategies, process with structure, and a buffer between their emotions and their money.

And then there is a third group. These are investors who began managing their own portfolios, sometimes successfully, sometimes not, but are now questioning whether they are still on the right track. Complexity has crept in. Time is limited. Markets feel more confusing. They are not failing, but they are starting to wonder whether they are optimizing what they are doing and beginning to feel overwhelmed.

There is also a fourth group. These are investors who are managing their own portfolios but do not realize they are making mistakes. They are not actively questioning their approach because they believe everything is fine. Often, they are unaware of the behavioural traps, tax inefficiencies, or investment risks they have unknowingly taken on. It is only when a serious mistake occurs, one that threatens their financial future, that they start to seek advice. Even then, they may not ever realize or fully acknowledge where they went wrong.

If the third or fourth groups sound familiar, read on because this blog is for you.

When Smart Investors Recognize the Limits of Going it Alone

Some of my best clients have at one point self-managed a portion or all their investments. Many had built portfolios that were perfectly reasonable. Some described their results as poor, some average, others felt they had done well. But all of them eventually reached a point where they realized something was missing. They were spending too much time second-guessing decisions. They were reacting to market news more than they cared to admit. And they began to realize they craved the structure and behavioural coaching that professional advice can provide.

In his view, only a very small percentage of the population is truly equipped to succeed as DIY investors over the long term. To do so, he argues, you need to possess four rare qualities:

An interest in the investment process. Not just in the outcomes, but in the work itself. Like how a gardener must enjoy digging in the dirt.

Sufficient mathematical skill. This does not mean advanced calculus, but it does require comfort with probability, statistics, and the often-counterintuitive nature of compounding and risk.

A strong grasp of financial history. Understanding past market cycles and common behavioural traps helps prevent repeated mistakes.

Emotional discipline. The ability to remain committed to your strategy even when markets are volatile or unsettling.

Bernstein estimates that only a tiny fraction of people possesses all four. Not because people are not smart or motivated, but because successful investing is as much about temperament and consistency as it is about knowledge. It is no wonder that so many capable individuals eventually seek professional guidance. Not because they cannot do it, but because they realize the cost of getting it wrong can far exceed the cost of getting help.

Personally, I believe Bernstein misses an important point. In my experience, even when someone does check all four of Bernstein’s boxes, the biggest limiting factor is often time, energy, and focus. Personally, many of my clients are highly capable individuals who could manage their portfolios themselves. But they choose not to. Not because they are unable, but because they would rather devote their time and energy to running their business, pursuing their careers, or enjoying other priorities in life. Delegating the day-to-day investment work and high-level financial planning is a strategic decision that allows them to stay focused on what matters most to them.

Most Investors do not get the Returns of the Funds they own

In your day-to-day life, you get feedback quickly. You make a decision, and usually that decision, especially if it is a business decision, you see results right away. You work hard in your career and earn recognition. But investing plays by different rules. You can make the right decision and still lose money. Or the wrong decision and still come out ahead. The feedback is delayed, noisy, and often misleading.

That is what makes investing such fertile ground for overconfidence bias. Most people believe they are better-than-average investors, just as most drivers believe they are better-than-average drivers. But that math does not add up.

In reality, most investors underperform the very investments they hold. Morningstar has tracked this phenomenon for years, as referenced in The Big Picture’s Mind the Gap article. Investors in mutual funds and ETFs often earn significantly less than the funds themselves deliver. The problem is not the products. It is the behaviour. Investors buy when markets feel good and sell when they feel scary. Put another way, they get caught in investment fads in up markets, and panic in a down markets. Either way, they let emotions and behavioural biases interfere with execution. Even when they pick good investments, they struggle to stick with them.

The result is a silent drag on performance. Not from bad investments, but from poorly timed decisions.

Revisiting Hidden Costs of DIY Investing

In my earlier post, The Hidden Costs of DIY Financial Planning, I discussed how emotional decisions and inefficient implementation, whether through poorly chosen products or tax mistakes, can quietly erode long-term results. Those risks remain very real. Continue Reading…