By Michelle Allen, BMO ETFs

(Sponsor Blog)

Canadian investors have increasingly been turning to all-in-one ETF solutions that offer built-in diversification and periodic rebalancing. BMO is proud to deliver on our commitment to make our Asset Allocation ETFs even more accessible to Canadian investors. To deliver even greater value, we recently announced a reduction to the annual management fee from 0.18% to 0.15% for our most popular Asset Allocation ETFs.

Now we’re Splitting to serve you Better

It’s important for us to continually evolve and support Canadian investors in reaching their unique financial goals.

With lower fees, and now, a stock split beginning on August 18, you can put more of your money to work in the portfolio that fits you best. Stock splits reduce the price per unit, making it easier to invest smaller amounts, rebalance with precision, and build diversified portfolios over time.

This change was inspired by feedback from our do-it-yourself investors and reflects our ongoing commitment to offering one of the lowest-cost, most accessible all-in-one ETF solutions in Canada.

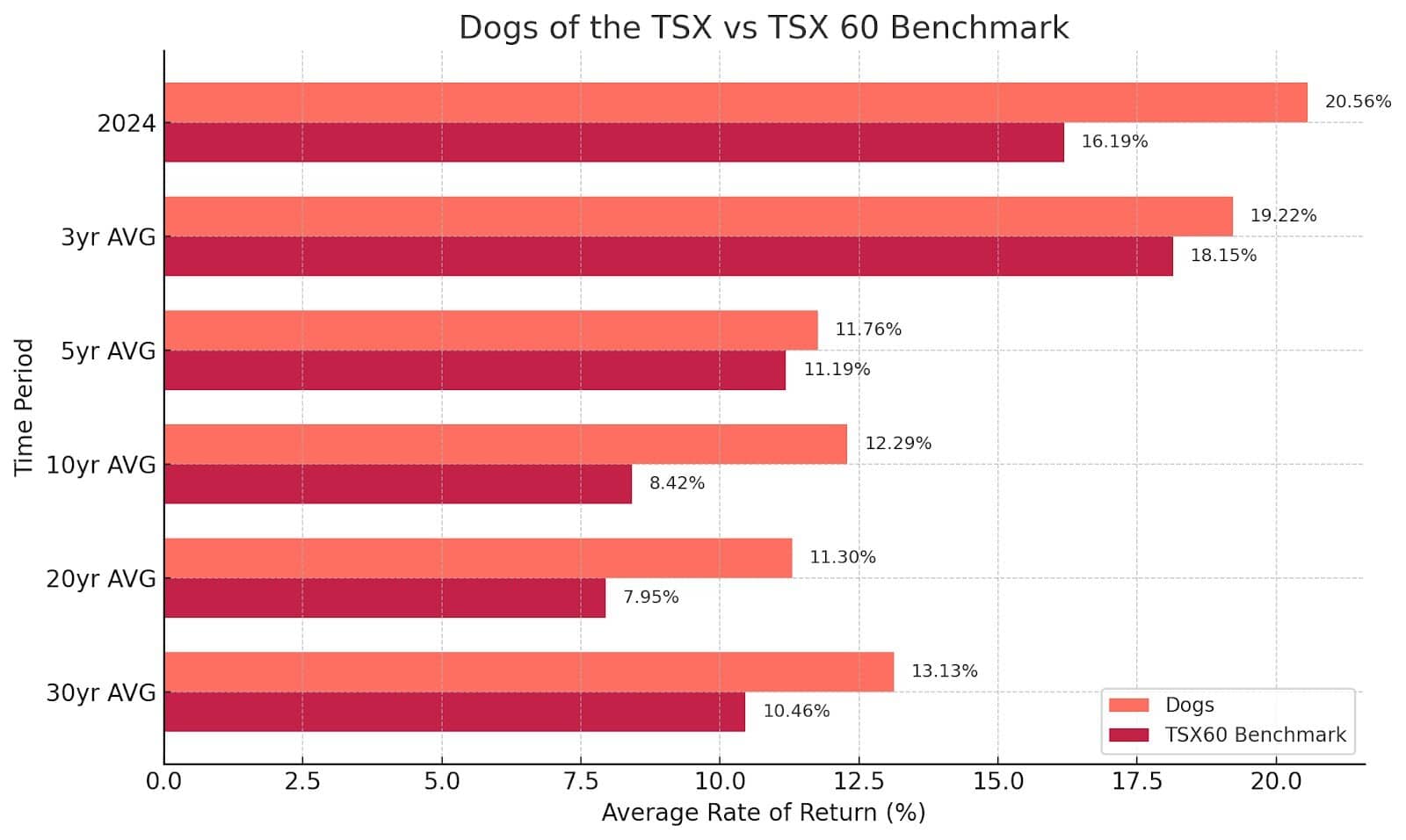

Consider ‘Zed’ instead with solutions like ZEQT (BMO All Equity ETF), ZGRO (BMO Growth ETF), ZBAL (BMO Balanced ETF) and ZCON (BMO Conservative ETF).

Learn more in our press release here.

Q: What is a stock split in the context of an ETF?

A stock split occurs when an ETF increases the number of its units outstanding by issuing additional units to existing unitholders. In a 3-for-1 split, each unitholder receives two additional units for every unit they already own: tripling the number of units while reducing the price per unit to one-third of its original value. This makes it easier to invest smaller amounts and manage portfolios with greater precision.

Q: Does a stock split change the value of my investment?

No, a stock split does not change the total dollar value of your investment.

If you owned 10 shares at $90 each before a 3-for-1 split, you would own 30 shares at $30 each after the split.

The total value remains $900.

Q: Why do ETF providers do stock splits?

Stock splits are typically done to:

- Lower the Net Asset Value (NAV) per unit, making the ETF more affordable and accessible to a broader range of investors.

- Improve liquidity by increasing the number of units available for trading.

- Encourage participation from newer or smaller investors who may be deterred by high unit prices.

Q: What are the benefits of a lower NAV for investors?

- Affordability: Lower NAVs make it easier for investors to buy full units without needing large amounts of capital. Continue Reading…