Investment properties have long been a cornerstone of wealth creation, offering a tangible asset that can provide both ongoing income and long-term appreciation. For individuals mapping out their financial future, the allure of real estate lies in its potential to generate passive revenue streams, act as a hedge against inflation, and build substantial equity over time. Navigating the world of property investment requires careful consideration of market trends, financing options, and management responsibilities, but the rewards can be significant for those who approach it strategically.

Adobe Stock image

By Dan Coconate

Special to Financial Independence Hub

The financial benefits of owning investment properties are multifaceted, primarily stemming from consistent rental income and the gradual increase in property value.

Rental payments from tenants can cover mortgage obligations, property taxes, and maintenance costs, often leaving a surplus that contributes directly to an investor’s cash flow.

Beyond this regular income, the potential for capital appreciation means the property itself can become a more valuable asset over the years. This combination of steady revenue and growth in underlying value makes investment properties a compelling option for diversifying an investment portfolio and securing a more robust financial footing for the future.

Deciding how to secure financial stability during retirement can feel overwhelming, especially when considering long-term strategies. Among the options, investment properties are worth exploring. Whether investment properties can benefit your financial future depends on many factors, but they can offer distinct advantages when managed wisely. Read on to uncover how real estate investments might support your retirement goals and gain key insights into the potential risks and rewards.

Maintaining steady Income through Rental Returns

By renting out an investment property, you can generate monthly cash flow that supplements your retirement savings. This income could cover living expenses or fund unexpected costs in your retirement, creating a layer of financial security. However, you must account for costs like maintenance, management fees, and property taxes so potential rental income remains profitable.

Building Long-term Equity

Real estate allows you to build equity over time when the value of your property increases. Unlike traditional savings or stock investments, properties provide a tangible asset that grows in value as you pay down your mortgage. Equity represents your ownership stake, which you can leverage for financial needs, reinvestment, or even retirement travel plans. Consider the area’s housing market trends before purchasing, which impact a property’s appreciation potential.

Diversifying Retirement Savings

Concentrating all your savings into one type of investment is risky, particularly as you near retirement. Real estate is like a diversification tool, reducing dependency on market-dependent ventures like stocks or bonds. This balance may shield you from financial losses if another investment market fluctuates. Keep in mind, though, that real estate isn’t immune to market downturns. Confirm that the candidate areas and property types you consider align with your financial goals. Continue Reading…

In his book Tightwads and Spendthrifts, marketing professor Scott Rick promises advice for “financial aspects of intimate relationships.”

What got my attention early is that his guidance “is rooted in rigorous behavioral science.” Applying the scientific method to human interactions is challenging, but it is generally better than relying on opinions. The book gives useful insights into how people think about spending money.

The introduction gives a four-question quiz designed to place the reader on a scale from 4 to 26. Those at the low end of the scale are called tightwads, and those at the other end are spendthrifts. Roughly half the respondents fell in the middle third of the range and are called “unconflicted consumers.” Most of the book deals with tightwads, spendthrifts, and their interactions; little is said about unconflicted consumers.

Demographic differences

Extensive surveys revealed some interesting demographic differences between tightwads and spendthrifts. “Tightwads are slightly older than spendthrifts,” but it’s not clear why. Do people become tighter with money over time (perhaps from getting burned by debt), or are there differences between generations?

“Women were somewhat more likely than men to be spendthrifts, and somewhat less likely than men to be tightwads. Tightwads were somewhat more likely to be highly educated, and they tended to opt into more mathematical majors, such as engineering, computer science, and natural science. The most popular college majors among spendthrifts were social work, communication, and humanities.”

How tightwads think

Being a tightwad is not the same as being frugal; “the highly frugal love to save, and tightwads hate to spend.” “The highly frugal are generally much more at peace in their relationship with money than are tightwads.”

It might seem intuitive that people are the way they are because of how much income they have available to spend, but “in survey after survey, we find no income differences between tightwads and spendthrifts.” However, “tightwads have far more money in savings and significantly better credit scores than spendthrifts.”

Having higher savings “offers no guarantee that tightwads feel financially comfortable. Subjective feelings of financial well-being are only loosely related to objective aspects of financial well-being.” For many tightwads, financial “anxiety stems from economic conditions early in life.”

Tightwads tend to think in terms of opportunity costs when considering spending some money. In one experiment where some participants had opportunity costs highlighted to them and others didn’t, “spendthrifts were twice as likely to buy the cheaper option” when opportunity costs were highlighted. “This framing did not influence tightwads.”

While tightwads spend less than spendthrifts in almost every area, “the amount of money both types had donated to charity was the same.”

How spendthrifts think

“Spendthrifts report high susceptibility to shopping momentum and what-the-hell effects. They commonly report going to buy one thing, then getting carried away.” “Spendthrifts are significantly more impatient than tightwads.” Interestingly, spendthrifts tend to understand these facts about themselves, and are not surprised when they later regret their purchases.

“Spendthrifts and compulsive buyers might spend similarly on any given shopping trip, but their underlying psychology differs significantly. Spendthrifts do not appear or report to be driven by anxiety management or mood repair.”

“Spendthrifts score slightly lower than tightwads on a financial literacy quiz.” However, Rick says that this is not a defining difference between tightwads and spendthrifts.

Is “spendthrift” an oxymoron?

The word “spendthrift” appears to blend contradictory elements: spending and thriftiness. However, “thrift here is used as a noun — meaning ‘savings ’— as it was in the seventeenth century. So spendthrifts are traditionally defined as people who recklessly spend their savings.”

Compensating for financial tendencies

Rick offers ways for tightwads and spendthrifts to compensate for their feelings about money. The first is to change “payment salience.” The book offers ways for tightwads to feel the pain of paying money less, and for spendthrifts to feel it more (e.g., by using cash more often).

Tightwads can reframe high-end purchases to think of them as a means to get high quality items. They can add a line item for indulgences into their budgets to make spending a “to-do” item. They can also reexamine their finances to confirm that all is well and, hopefully, reduce financial anxiety.

Spendthrifts can be mindful of opportunity costs, try to delay spending (e.g., sleep on it), and set saving reminders for themselves. Interestingly, spendthrifts might understand “better than tightwads” that “the excitement that comes with a new product usually fades over time,” but this knowledge doesn’t appear to help them reduce spending.

Relationships

When we consider marriages among tightwads and spendthrifts, but not including any “unconflicted consumers,” 58% are between a tightwad and a spendthrift, and only 42% are between two people at the same end of the tightwad-spendthrift scale. “We tend to marry people who share characteristics that we like in ourselves. However, a key insight about tightwads and spendthrifts is that they do not particularly enjoy being tightwads and spendthrifts.”

Although some prominent people who advise their followers on personal finance topics consider any money secrets between spouses to be “financial infidelity,” Rick thinks there is room for a small amount of secrecy as long as it’s not the cause of financial shortfalls. How much secrecy is desirable or tolerable probably varies from one couple to the next.

“Latte factor myth”

Rick adds his two cents to the endless debate on whether we should engage in small indulgences by siding with those who say it’s fine to buy expensive coffee. Like most others, Rick approaches this debate as a binary choice: lattes are either universally good or universally bad. Continue Reading…

Investing in companies that sustain and/or increase their dividends through different economic cycles is widely regarded as a prudent investing strategy, as sustainable dividend policies typically serve as a proxy for identifying high-quality businesses.

Companies with a track record of dividend growth often exhibit strong, reliable cash flows, disciplined capital allocation, and a clear commitment to returning value to shareholders. Such an investing approach can provide a steadily rising income stream to help offset inflation and enhance total returns over time.

We are excited to unveil the HAMILTON CHAMPIONS™ ETFs: built for long-term growth from exposure to blue-chip Canadian and U.S. companies with consistent track records of growing dividends (CMVP/SMVP). The suite also includes two Enhanced HAMILTON CHAMPIONS™ ETFs that utilize modest 25% leverage to further enhance long-term growth potential (CWIN/SWIN).

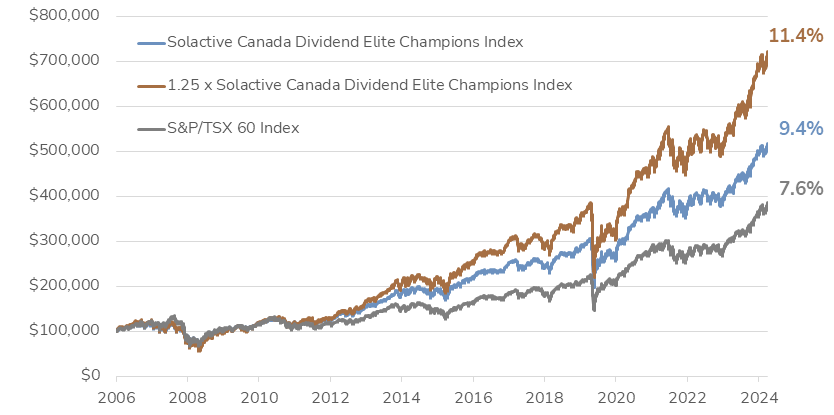

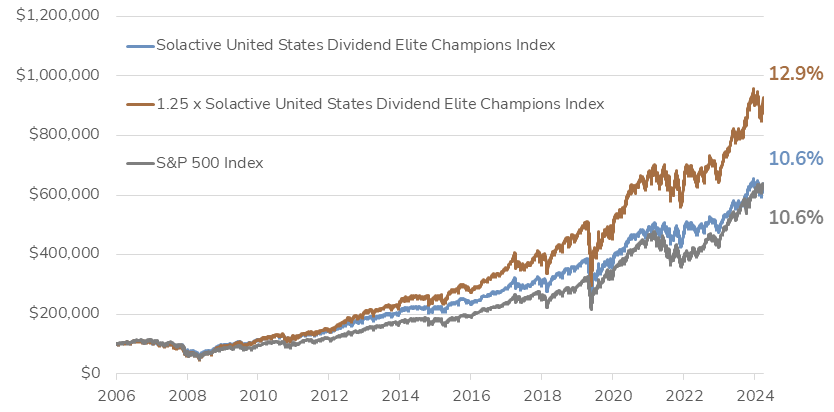

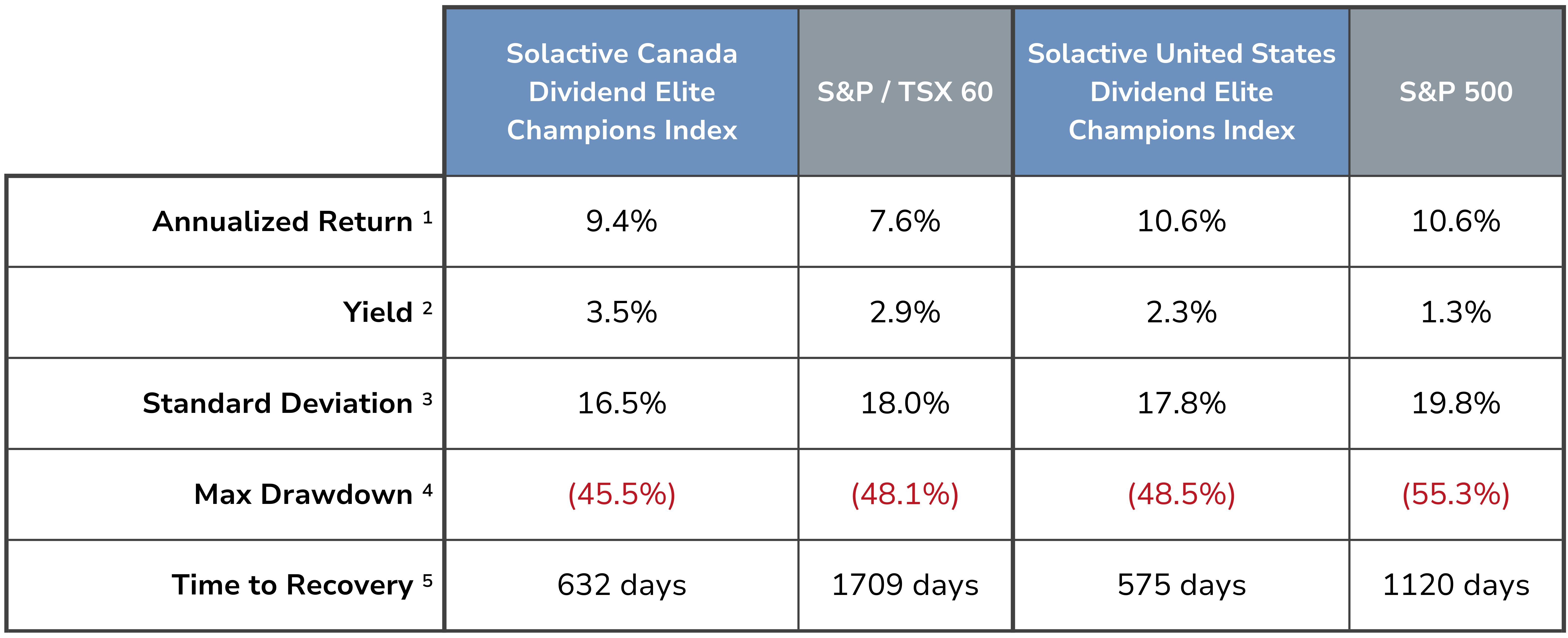

The HAMILTON CHAMPIONS™ ETFs are designed to track the Solactive Dividend Elite Champions Indices[7]. Boththe Canadian and U.S. indices have demonstrated strong performance and low volatility historically relative to the S&P/TSX 60 and the S&P 500, respectively.

Canadian HAMILTON CHAMPIONS™ — Growth of $100K [8],9]

U.S. HAMILTON CHAMPIONS™ — Growth of $100K [8, 10]

The Canada Dividend Champions Index and U.S. Dividend Champions Index are designed to provide equal-weight exposure to blue-chip stocks, listed in their respective countries, with a long history of dividend growth/sustainability. The result is a Canadian and a U.S. index with favourable performance and risk profiles vs. the S&P/TSX 60 and S&P 500, respectively. In addition, both indices have demonstrated (i) lower relative volatility; (ii) lower relative drawdowns; and (iii) faster relative time to recovery.

DISCLAIMER: see footnotes 1-5 below

Proven Winners, Rising Dividends

The Solactive Dividend Elite Champions Indices are focused on delivering diversified portfolios of companies with a long history of increasing dividends. The resulting portfolios have the following important characteristics: Continue Reading…

Inspiration for this post arrived from attending a few retirement parties of late with work colleagues, another one as recently as yesterday and a few more to attend this spring.

Is age 50 too young to retire?

What about age 55? Age 60?

After talking to some work colleagues who submitted their retirement letters and who are now moving on, I know their ages. The celebration yesterday was for someone in their early 60s. They talked and yearned about more time at their cottage, doing small home reno projects, and leaving early morning Microsoft Teams calls in the rearview mirror.

They also talked about their desire to retire now since they “had enough” both mentally and financially: support from the latter after working with their financial advisor or planner and doing some retirement math on their own to bridge the gap between spending needs now and when their pension benefits would kick in, at age 65, including their firm intention to take CPP and OAS at that age too.

Although I’m leaping to lots of assumptions here, this makes me believe that the personal retirement savings of some work colleagues (the sum of RRSPs, TFSAs, non-registered investments or other assets) is likely small to modest beyond a workplace pension: in that they needed to work to ensure they were not sacrificing their personal portfolio too much, too soon. I get that. After decades of raising a family, buying a cottage, paying down a mortgage or two along with other expenses I’m sure, it seems my colleague was more than ready to permanently slow down; cut the cord from work and enjoy their time more while they still have decent health. Good on them. 🙂

This individual is however not the first person to mention the following to me:

“Oh, I can’t afford to retire yet but thinking age 63 or so should be fine since that’s when I can get my full OAS and decent CPP income.”

And my work colleague is hardly alone …

In looking at some stats (Source: StatsCan) the average age of retirement is hardly for anyone in their 50s:

These are also not easy times to retire…

Rising general inflation, uncertain tax rates, and higher healthcare costs could very well impact many retirees at any age. Myself included. Certainly, starting to save for retirement early and often and getting out of debt faster than most would be enablers – and I hope they have been for us.

You are too young to retire – is early retirement right for you?

Although many Canadians seem to expect to retire between the ages of 60 and 70 above, there is absolutely no hard and fast rules about when you need or must stop working of course.

Your retirement timeline will depend on many factors, I’ve highlighted some milestone ideas below:

Somewhere between 3-5 years before retirement, it’s probably wise to get some retirement details in order. Accuracy isn’t overly important IMO but the process of planning is.

I recall focusing on our desired lifestyle and spending habits to go with it: what early retirement or semi-retirement or full retirement might look like:

We started estimating our retirement spending levels, our income sources, and inflation factors.

We started evaluating our portfolio returns over the last 5- or 10-years.

We looked seriously at our sustainable cashflow from our portfolio (passive dividend and distribution income since we’d be too young to accept any workplace pension or any CPP or OAS government benefits).

We started tracking our spending in more detail to challenge those spending assumptions.

1-2 Years Before Retirement

As recently as early 2024 for us, things got more serious.

In the year or so leading up to any big decisions, more detailed planning kicked into higher gear:

We spent more time as a couple talking about how to put some travel dreams into reality – multi-week vacations in the coming years away from icy/cold Ottawa winters.

We started to explore ways at work to test some semi-retirement assumptions; the desire but also the financial flexibility to work part-time vs. full-time (i.e., could we still make ends meet).

We started to look into post-retirement healthcare insurance options, where needed.

We started to talk about our purpose (if not working at all) – what would we do with our time?

Although we might be in this timeline, not sure, since part-time work is now occurring with our solid employer (this could continue for both of us??) but this is where the real retirement countdown calendar probably begins for most people…as you strike full-time working days off your calendar: Continue Reading…

Discover unconventional paths to Financial Freedom that go beyond traditional advice. This article presents surprising strategies, backed by expert insights, that can transform your approach to wealth-building. From maintaining your lifestyle despite income increases to investing in non-financial assets, these innovative methods offer fresh perspectives on achieving financial success.

Maintain Lifestyle Despite Income Increases

Access High-Value Real Estate Through Syndications

Build Wealth with Niche Websites

Invest in Non-Financial Assets for Growth

Profit from Surplus Business Equipment Sales

Turn Discarded Inventory into Profitable Ventures

Monetize Legal Downtime with Tech Solutions

Transform Teaching into Wealth-Building Opportunity

Generate Passive Income by Renting Unused Space

Leverage Prop Trading Firms for Capital Growth

Maintain Lifestyle despite Income Increases

One unconventional yet effective method I tried to grow wealth and become financially independent is strategically managing lifestyle deflation in alignment with income changes. In simpler words, this means continuing to maintain the same lifestyle and budget even when your income increases, instead of adjusting your expenses alongside it.

I learned to prioritize this in my younger years after seeing people around me struggling to maintain their lifestyles despite rising income. I noticed they were increasing their expenses as their income grew. Most of these expenses were smaller differences that usually go unnoticed but compound to a bigger sum when you see them in total. Examples include subscribing to more services than before, buying more expensive items because they can now afford them, etc. Seeing all this, a thought nagged me often: “What would happen if they saved the raise they got instead of spending it immediately?”

As I learned more about personal finance, budgeting, etc., I started making a conscious effort to maintain the same lifestyle as always even as my salary grew. I funneled the extra sum into various investments instead. Over the years, this habit helped my net worth increase without compromising my quality of life.

Here are some tips I will offer others in this regard:

Automate the transactions into specific accounts: Immediately redirect your extra amount into another savings account for debt repayment and investments. This will help you avoid impulsive spending.

Understand wants vs needs: Take a broader look at your budget, including things you spend on usually. List all the expenses you make and consider which are important and which you can postpone for later since there is no immediate need. Doing this will help you stay focused.

Track net worth monthly: Make sure to track your investments frequently. Seeing your net worth grow will keep you motivated to continue your habit and avoid unnecessary purchases. — Lyle Solomon, Principal Attorney, Oak View Law Group

Access High-value Real Estate through Syndications

One unconventional way I’ve built wealth that surprised me on my journey to Financial Independence is through the strategic use of real estate syndications. While many focus on buying individual properties, I discovered that pooling resources with other investors allowed me to access high-value opportunities I wouldn’t have been able to tackle alone.

This method allows you to invest in larger commercial properties with a group of people, benefiting from economies of scale and shared risks. I first came across this approach through networking with experienced investors and learning about the power of group investment.

My advice to others would be to build a solid understanding of how syndications work and start small with reputable groups. It’s a unique way to scale wealth while minimizing individual risk, and it’s often overlooked compared to traditional property purchases. Collaborating with experienced partners can unlock doors to lucrative projects that wouldn’t be accessible otherwise. — Jonathan Ayala, Licensed Real Estate Salesperson | Founder, Hudson Condos

Build Wealth with Niche Websites

One unconventional way I’ve built wealth that really surprised me was by doubling down on building tiny niche websites. Early in my career, I thought the only path to success was creating huge, authority-style blogs. But after some experimentation, I realized that smaller, hyper-focused sites could generate a steady income without requiring a massive team or overhead.

I stumbled onto this by accident while testing out ideas that didn’t quite fit my main business. A few of these small projects started making a few hundred dollars a month each, and when you scale that up across multiple sites, it becomes something compelling. The magic is in finding a narrow topic where you can be the absolute best resource online, even if it’s something super specific.

For anyone interested, I suggest thinking smaller, not bigger. Find those underserved niches where competition is low, but passion or need is high. Focus on genuinely helpful content, optimize it properly, and be patient. It’s not a get-rich-quick strategy, but it is an incredibly reliable way to build passive income streams.

This approach allowed me to diversify without putting all my eggs in one basket and played a big part in reaching Financial Independence sooner than I expected. — James Parsons, CEO, Content Powered

Invest in Non-Financial Assets for Growth

One unconventional way I built wealth was by keeping a “no-market” year. For twelve months, I chose to remove myself from investing in anything that required speculation, interest, or growth. Instead, I focused on building non-financial assets: time, skill, energy, and relationships. I tracked it like a portfolio: hours of learning, time saved by simplifying routines, days reclaimed from overcommitting, and people I could count on for collaboration. That “quiet compounding” brought in far more than my typical quarterly gains ever did. I walked into the next year with three new paid projects, two solid partners, and almost double the free time.

I discovered it accidentally after turning down a contract that would have pulled me out of integrity. I gave myself permission to step back and see what kind of return I could build without putting money anywhere. I suggest trying this as a 90-day experiment. Track the non-financial gains as seriously as you would your net worth. Value created in learning, trust, and creative space often turns into money later. The catch is, you have to believe it is real before anyone else does. Once you see it, it is hard to go back. — Adam Klein, Certified Integral Coach® and Managing Director, New Ventures West

Profit from Surplus Business Equipment Sales

Purchasing and selling surplus business equipment was much more profitable than previously thought. Initially, it was just a game of turning what companies didn’t want into something useful. But as time went by, I learned what had actual value was an awareness of where the demand was: what buyers were searching for but couldn’t be found easily. That gap became an opportunity.

I became interested in it on a whim when assisting someone with liquidating their lab, and saw its inefficiency. So we built a system around it. My advice? Identify supply chain omissions or inefficiencies in industries that people do not pay much attention to. The more untrendy it sounds, the more opportunities you’ll have if you’re willing to master it inside out. — Joe Reale, CEO, Surplus Solutions

Turn Discarded Inventory into Profitable Ventures

I started buying leftover inventory from failed event suppliers. Half the time they were happy just to offload it for $0.10 on the dollar. I mean, we once picked up $35,000 worth of LED wall panels for $2,800, stacked them in our warehouse, and rented them out per gig for $650 a pop. In under four months, they paid for themselves, and we have since generated over $48,000 in revenue from those same panels. Everyone wants to build wealth from stocks or SaaS. I just bought junk others walked past and turned it into profit. Continue Reading…