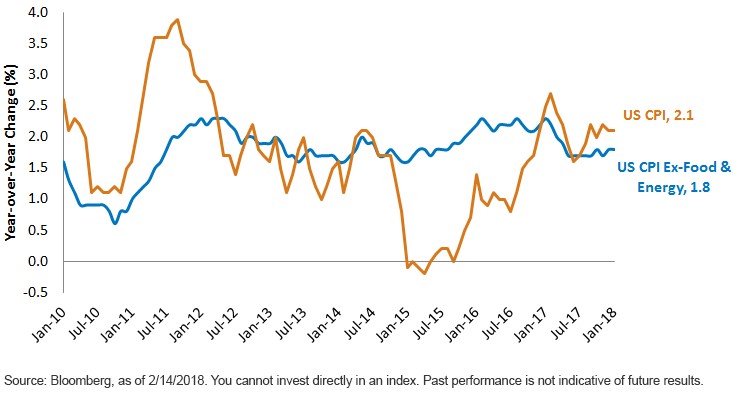

Bitcoin, blockchain, initial token offerings … yikes! As financial headlines dedicate an increasing amount of coverage to this relatively new area, it’s left many investors scratching their heads. What is bitcoin? Do I need to know about this? Am I missing out on an opportunity? Below we present a question and answer that we hope investors might find helpful.

Bitcoin, blockchain, initial token offerings … yikes! As financial headlines dedicate an increasing amount of coverage to this relatively new area, it’s left many investors scratching their heads. What is bitcoin? Do I need to know about this? Am I missing out on an opportunity? Below we present a question and answer that we hope investors might find helpful.

From a curious investor:

So what do you make of bitcoin? I am interested in your views on it as both an ‘investment’ and as a game changer. Much to my annoyance, although I believe the world banks are inflating the money supply and the price of hard assets, this has not shown up in the price of gold.

I do not understand it at all. A friend of a friend has become a millionaire and yes he sold enough to make it real money …

Our response

While we’re by no means experts, we’ve thought about this and where we’re at with bitcoin is that while it may be a game changer, we wouldn’t invest in it as an asset in its own right.

Let me back up a bit.

The underlying technology that allows for the creation of bitcoin and other crypto-currencies , blockchain, is complex but the concept is not complex. Essentially, rather than having a centralized system such as an accounting system or bank where the data is all held and processed centrally, blockchain allows for the data and processing to be decentralized.

They refer to it as distributed ledger technology. It’s out there on the web, accessible to anyone but encrypted and secure. Digital or crypto-currencies are just a really interesting application of this blockchain distributed ledger technology. Up until now, it’s really only been national central banks that have been able to issue currencies and lots of middlemen (banks, brokers, other lenders) have developed to help manage the system and they all take a little off the top to help keep the system running. Digital currencies can be huge disrupters of this status quo, cutting out middlemen and removing the central banks from the process entirely (maybe).

Bitcoin just happens to be the leading crypto-currency at this point. There are lots of other ones as well as what’s referred to as crypto-tokens which not only serve as a medium of exchange but also have some other utility attached to them like they allow you to buy something or to receive a service (loyalty programs are a bit like this). It’s still very early days in terms of any of these being a reliable medium of exchange. For example for bitcoin the average transaction settlement time is around 45 minutes and often can be days. Imagine being at the grocery store and wanting to pay with bitcoin from your digital wallet and you have to stand there for 6 hours before the grocer gets confirmation that you have sufficient bitcoin and can transfer it to the grocer’s digital wallet. Your ice cream would have melted by then. People also want a medium of exchange to be stable. Bitcoin and other crypto currencies are wildly volatile.

Blockchain is a game changer

That said, I do believe the people that say blockchain and the application of it to crypto-currencies is a game changer. I don’t know where it ends up or even if bitcoin will remain as the main crypto-currency but this could be a massive change. Continue Reading…