Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

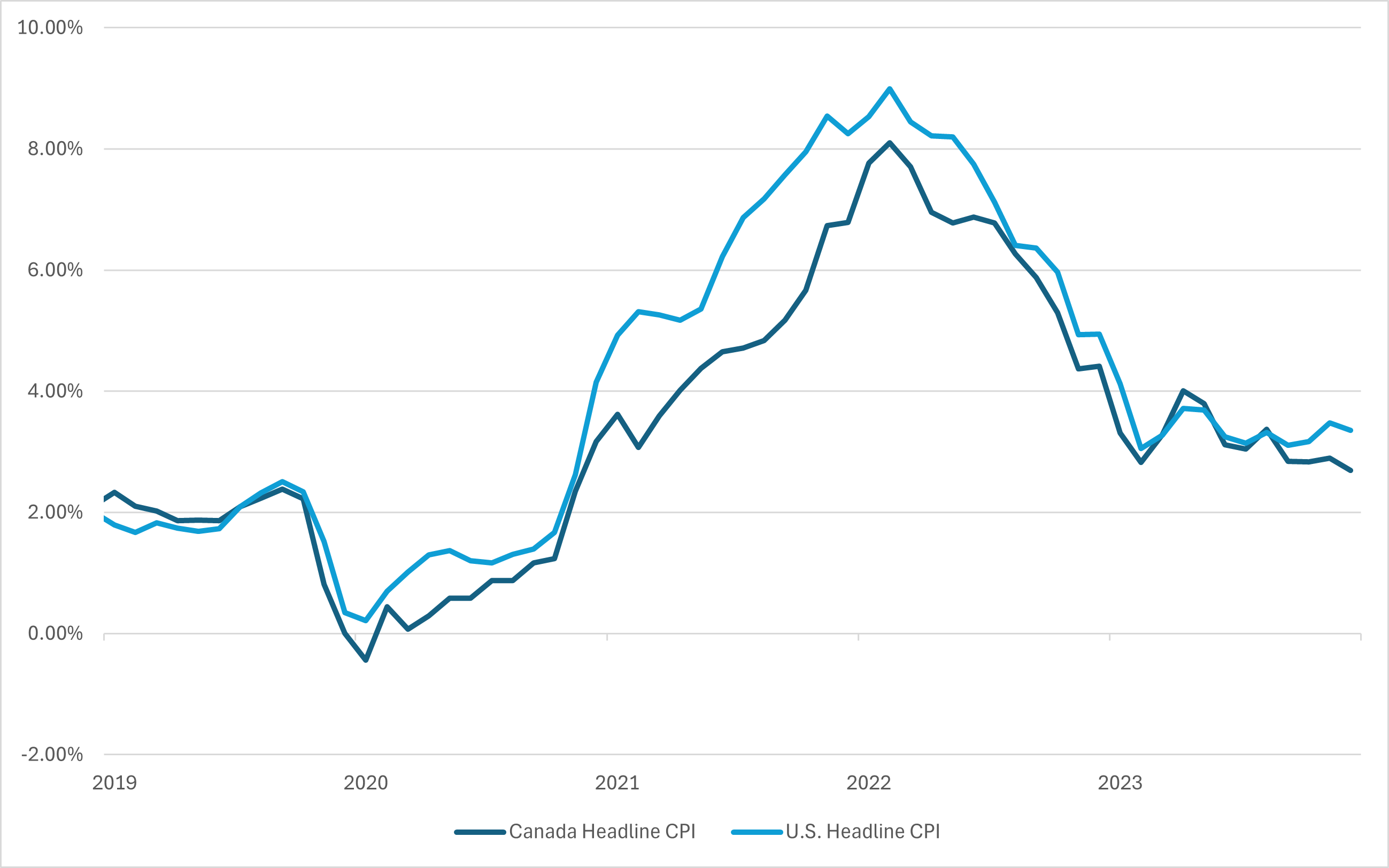

Inflation continues to be the biggest near-term driver for equity markets, given its influence on central bank decision-making regarding interest rates. Inflation rates have moderated from their peak levels; however, they remain above the 2% targets set by the Bank of Canada (BoC) and the U.S. Federal Reserve (Fed).

U.S. and Canada Inflation

As of April 30, 2024

Equity markets entered 2024 with six to seven U.S. interest rate cuts priced in over the course of 2024, with the first cut expected in March. Clearly, that did not happen. Both central banks have remained on hold, which has contributed to higher rates across the yield curve. That number has since moderated to only three cuts, and the timing of the first cut has now been pushed out to June in Canada and even later in the United States.

The effect of “higher for longer” interest rates has been particularly painful for interest rate-sensitive market sectors such as utilities and communication services. Nonetheless, pockets of the market that were expected to continue to grow have continued to advance, undeterred by the yield curve shifts.

Buoyed by hopes for a pivot in monetary policy as inflation trended closer towards the central banks’ targets, Canadian equities had a strong start to the year, although they paled compared to the ongoing boom in U.S. equities, where a large portion of the gains were derived from mega-cap information technology and related names with less representation in Canadian markets.

Mind the lag

Although decelerating, the economy continues to show sufficient resilience, with customer spending remaining robust since the reopening of economies after the global pandemic-induced shutdowns. Fiscal stimulus has moderated since the immediate aftermath of the pandemic outbreak; however, fiscal policy continues to operate at odds with monetary policy. Labour strength and wage gains have further reinforced this view, fuelling fears of lingering inflation and the potential for a higher-for-longer rate environment. Continue Reading…

The term “wellness” — including emotional, physical, and mental wellness — is finding its way into more and more conversations these days. However, there’s one aspect of general wellness that is often overlooked despite its significant impact: financial wellness.

Given the current economic environment, financial concerns among Canadians are one of the largest sources of stress. According to a recent study by FP Canada, forty-nine per cent of Canadian adults have lost sleep because of financial worries, which may impact their overall wellness.

Just like physical and mental wellness, there is no one formula to create financial wellness for everyone.

Luckily, there are strategies we can all take to improve our financial wellness. It starts with acting in the present while planning for the future. The path to financial wellness is a personal journey, and a qualified financial advisor can help you take the first step and make important progress.

Prioritizing financial wellness for today

Before working on your financial wellness, it’s important to ask, “What does financial wellness look like for me?”

It can be as simple as creating (and sticking to) a budget or making a realistic and actionable plan to pay off your current debts. Your path to financial wellness can even begin by getting a better understanding of a familiar term: tax.

Whether we like it or not, tax is inevitable, and it impacts nearly every financial decision we make. Therefore, gaining an understanding of your tax situation can provide you with confidence and can help improve your financial wellness.

Depending on your circumstances and stage of life, contributing to your Registered Retirement Savings Plan (RRSP) or First Home Savings Account (FHSA) are two options that may help you prepare for your future, while also reducing your taxable income, meaning you’ll get taxed less come tax season.

Being knowledgeable about the different types of accounts (including RRSPs, FHSAs and Tax-Free Savings Accounts), as well as tax deductions and tax credits available to lessen your tax liability, can also help build financial knowledge and reduce financial stress.

Planning financial wellness for the future

Part of financial wellness is proactive planning so you can feel comfortable and confident in your future. Saving is an important part of building a strong financial future, but financial wellness goes beyond that. Continue Reading…

In the quest for financial stability amidst major life milestones, we gathered wisdom from Finance Experts to CEOs, compiling twelve diverse strategies.

From establishing a safety net to applying the 50-30-20 budgeting rule, these professionals share how they’ve successfully built and maintained emergency funds while pursuing family formation and homeownership.

Establish a Safety Net

Adopt Frugal Living Practices

Set Achievable Saving Goals

Automate Savings Allocation

Implement Disciplined Saving

Live Below Your Means

Reduce the Temptation to Spend

Diversify Income with Side Hustles

Maintain Emergency Fund While Home Owning

Strategize with Automatic Transfers

Manage Spending, Build Runway

Apply the 50-30-20 Budgeting Rule

Establish a Safety Net

As a seasoned finance expert, I understand the critical importance of establishing and maintaining emergency funds, especially when navigating major life milestones like family formation and homeownership. Here are some strategies I recommend for achieving financial security while pursuing these goals:

Building the Safety Net: We suggest a reserve that equals three to six months’ worth of living costs, which acts as a buffer for matters like falling sick, fixing a car, or losing employment. You can begin by making small deposits into a high-interest savings account and then building on it gradually. Save everything!

Goal-Oriented Saving: After setting up an emergency fund, the next step is to save towards your dream house. Consider putting money into Fixed Deposits or Recurring Deposits, as they have guaranteed returns and help inculcate discipline, too. Remember to stay consistent! — Arifful Islam, Finance Expert, Sterlinx Global LTD

Adopt Frugal Living Practices

My husband and I have built and maintained emergency funds by continuing to employ financial tactics we had to use early on in the pandemic, when COVID-19 lockdown-related issues resulted in his salary being temporarily reduced and my hours being cut back.

We were adamant about the need to continue adding even a small amount to our emergency fund since we had purchased a home only the year before. Thanks to friends’ and family’s experiences, we were well aware of the ever-present chance of a home-related emergency.

We decided on a two-pronged approach: We lived beneath our means by greatly curtailing our travel, cultural, and dining-out budget, finding free and low-cost alternatives to enjoy closer to home, as well as cooking new items at home.

We also became savvy consumers. We started comparison shopping for budget items, both big and small. Our biggest savings came from comparing car and home insurance companies: When we switched to a new company, we saved over $700 a year.

The strategy I followed for building my emergency fund took a decent amount of time. My plan was to cover three to six months of living costs. I was well aware that saving that much money would take time. So, I started with simple goals like saving $10 a day.

I somewhat understood that the savings goal depends on income and expenses. So, I tried to cover essential expenses first, rather than transferring all my income to savings. I paid off costs such as housing, utilities, transportation, food, and credit-card/loan payments before anything else. Then, I added up my monthly spending and multiplied it by six months. I got the estimated total amount I need to save as an emergency fund.

I decided to keep my funds in a high-yield savings account. These types of accounts are convenient to access and offer good interest rates. As a result, your funds will grow gradually. However, I suggest choosing banks and credit unions insured by the National Credit Union Administration (NCUA) or the Federal Deposit Insurance Corporation (FDIC).

Last but not least, it is better to use a direct deposit service to transfer your money into your bank or savings account. Contact your bank and activate the direct deposit service. It would be wise to split direct deposits and put a certain amount in your emergency fund and the rest in your checking account. — Loretta Kilday, DebtCC Spokesperson, Debt Consolidation Care

Automate Savings Allocation

I’ve always prioritized building an emergency fund because it’s crucial for my family’s financial security and peace of mind. Early in my career, I adopted a simple yet effective strategy: automate and allocate.

I set up automatic transfers from my business income to a separate high-yield savings account every month. Initially, I aimed to save at least six months of living expenses, which I gradually expanded to cover an entire year.

Treating this fund as untouchable for everyday expenses became a safety net that allowed my wife and me to comfortably pursue family goals like buying a home. To balance this security with growth, I also invested in low-risk, highly liquid bonds and money market funds for a portion of the emergency fund. — Michael Sena, CEO and Lead Analytics Consultant, Senacea Ltd.

Implement Disciplined Saving

Building and maintaining an emergency fund has been a cornerstone of ensuring my family’s financial security, especially as we pursued significant goals like family formation and homeownership. From my experience, the key has been a disciplined, proactive approach to saving, paired with a clear understanding of our financial priorities and potential emergencies.

Initially, I established a strict budgeting process where setting aside money for an emergency fund became a non-negotiable monthly expense, similar to mortgage or utility bills. I targeted saving at least three to six months’ worth of living expenses, a common benchmark that provided a safety net capable of covering unexpected events such as medical emergencies or job loss.

To stay disciplined, I automated the transfer of funds from our checking account to a high-yield savings account specifically designated for emergencies. This automation ensured that the savings occurred without requiring active management on my part each month, reducing the temptation to skip or divert these funds toward other uses. Choosing a high-yield account also helped the fund grow faster through interest, maximizing the efficiency of our savings.

As our family grew and our financial situation evolved with goals like buying a home, we reassessed our emergency fund needs regularly. For example, when planning for homeownership, we increased our emergency savings target to account for potential home repairs and maintenance, which are typically more costly than many renters anticipate. This adjustment was crucial in maintaining our financial security after transitioning to homeownership.

Throughout these phases, maintaining open communication about our financial goals and progress has been vital. Regular discussions with my spouse ensured that we were both aligned on our savings goals, understood the reasons behind them, and could track our progress together. — Michael Dion, Chief Finance Nerd, F9 Finance

Live below your Means

The secret to building wealth is living below your means. You need to be clear on the income coming in and the expenses going out. Pay yourself fi rst. The results of compound interest are powerful.

As your income increases, lifestyle inflation creeps in. Lifestyle creep occurs when an individual’s standard of living improves as their discretionary income rises and former luxuries become new necessities.

Avoid the urge to spend more as you make more. Instead, save more. Invest the difference. As you get a raise, give yourself a raise. Increase your 401(k) contribution. Add to your emergency fund. Your future self will thank you. — Melissa Pavone, Director, Investments CFP, and CDFA, Oppenheimer & Co. Inc. Continue Reading…

Index investing, a strategy adopted by cost-conscious investors and passive investing aficionados, is continuing to gain in popularity across individual investors, advisors and institutions alike.

The S&P 500 Index is widely regarded as a gauge of the overall large-cap U.S. equities market. The index, which dates back to the 1920s, includes 500 leading companies and covers approximately 80% of available market capitalization.1 Other popular indices for U.S. equities include the Dow Jones Industrial Average (covering a smaller number of companies: ~30), and the Nasdaq 100 Index (tracking the largest 100 companies listed on the Nasdaq Stock Market).

ETFs make index investing more efficient, helping investors save time and money relative to holding all the constituents of their favorite market index. Take the S&P 500, for example. Not only would you need to buy 500 companies, you would need to make sure they maintain the appropriate weight in the portfolio over time: requiring a lot of time, and money in trading those securities.

ETF units are primarily bought and sold between different investors. This means there are typically fewer realizations of capital gains and losses with ETFs than with other investment products. Similarly, as passive ETFs track the performance of a specific benchmark, they tend to have lower overall portfolio turnover. Fewer transactions within the ETF again means fewer realizations of capital gains and losses that may flow through to ETF holders.

Investing in the S&P 500 Index has been made simple with ZSP2 – BMO S&P 500 Index ETF. Also available in hedged and USD (ZUE/ZSP.U)2, these ETFs give you exposure to this broad market index at a low cost of 0.09% 6(MER – Management Expense Ratio) and can be used as a core in your portfolio. Index based ETFs like ZSP provide broad market exposure and diversification across various sectors and asset classes according to their underlying index. It’s not about timing the market with index-based ETFs, it’s about time in the market and these solutions provide a long-term strategy for investors.

What does the research show?

Another reason index-based investing is becoming a staple in investors’ portfolios is the increase in available research showing passive outperforming active over the long term. The best known of this research, the SPIVA report, which coming from S&P Dow Jones Indexes research division has been looking at this phenomenon for 20 years, measuring actively managed funds, against their index benchmarks worldwide.

Looking at the data as of Dec 31st 2023, and focusing on Canadian Equity Funds, 96.63% of active fund managers underperform the S&P/TSX Composite over 10 years. Put another way just 3.37% of funds outperformed the S&P/TSX composite over that time period.3 This research holds across time periods and geographies, with the numbers changing year to year but the story remaining compellingly in favor of passive. While there are active managers that out-perform their benchmark, this can be challenging to do consistently over time, even for the professionals.

Innovation in Index Investing

“Losses loom larger than gains.” – Daniel Kahneman & Amos Tversk4

Famed researchers in behavioural finance, Daniel Kahneman and Amos Tversky, once hypothesized the psychological pain of loss is about twice as powerful as the pleasure of gaining. After strong performances from U.S. stocks over the past two quarters, some may find themselves dusting off the pair’s work and asking, is now the time to lock in gains and take some downside insurance?

We have seen a remarkable run from stocks such as Nvidia, lifting the S&P 500 Index to all-time highs. This may cause some valuation concerns among investors. The S&P 500 is currently trading at a price-to-earnings ratio9(P/E) of about 25 times, which from a historical perspective can be considered rich relative to the average of 17.5 Continue Reading…

Imagine waking up to new horizons each day, with the promise of adventure and luxury at your fingertips. For many, retiring and spending their golden years exploring the world from the comfort of a cruise ship is the ultimate dream, and some are turning it into a reality.

Citing data from the Cruise Lines International Association, MoneyDigest highlights that 50% of the 20.4 million people who took a cruise in 2022 were over the age of 50, while 32% were over 60. However, it’s also important to note that this lifestyle is not attainable for everybody.

A poll conducted by the National Institute on Retirement Security finds that more than half of Americans (55%) are concerned that they cannot achieve financial security in retirement, much less afford to live on a cruise ship. That’s where the FIRE (Financial Independence, Retire Early) movement comes into play. In this article, we’ll explore why so many are drawn to retiring at sea and how the FIRE strategy can help folks achieve enough financial security to live out their cruise ship retirement dreams.

The Appeal of Cruise Ship Retirement

Image by Pexels

Retiring on a cruise ship is an attractive option for those who seek adventure, comfort, and a unique globetrotting lifestyle, but its biggest draw is that it can be more affordable than retired life on land.

According to an article from CNBC, the average annual cost to retire comfortably in the U.S. can be anywhere between US$55,074 and $121,228, depending on which state you choose to live in. These numbers factor in living costs, including groceries, healthcare, housing, utilities, and transportation.

Meanwhile, the 2021 national average for a private room in a nursing home was estimated to cost $108,405 per year. By contrast, Business Insider reports that cruise ship companies looking to capitalize on the retirees-at-sea trend now offer fully furnished homes aboard their ships for roughly US$43 a day or less. Continue Reading…