Guess who just got back today

Them wild-eyed boys that had been away

Haven’t changed, had much to say

But man, I still think them cats are crazy

The boys are back in town, the boys are back in town

- The Boys Are Back in Town, by Thin Lizzy

By Noah Solomon

Special to Financial Independence Hub

Government Bonds: The Gift That (Usually) Keeps on Giving

Historically, bonds have provided investors with two main benefits. Firstly, their yields have provided a reasonable, if unspectacular return. Secondly, they have offered diversification value, muting overall portfolio losses during bear markets. By owning high-quality bonds, you got paid for protecting your portfolio during times of market turmoil, which is akin to receiving (rather than paying) a premium for fire insurance: a remarkably sweet deal indeed!

However, these benefits have historically ranged from significant to nonexistent, depending on the investment environment. Given this fact, Investors should alter their bond exposure as conditions warrant, both in terms of their aggregate allocation to the asset class as well their bond portfolios’ exposures to changes in interest rates and credit conditions.

A Bear Market Sedative

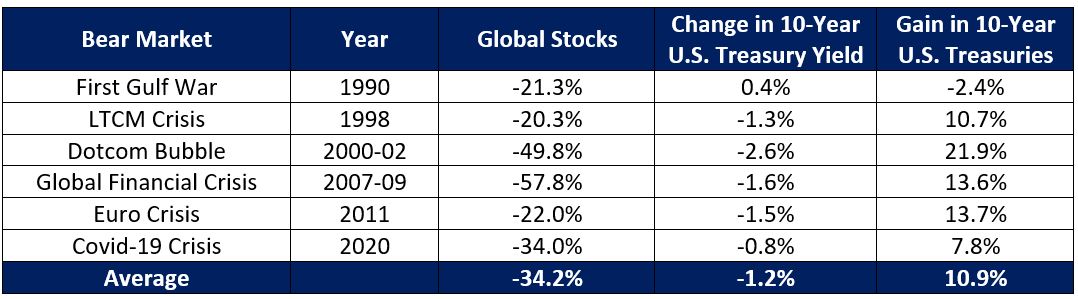

As the following table illustrates, in five of the six equity bear markets before that of 2022, bonds provided investors with much needed gains, thereby mitigating the overall damage to their portfolios.

During the tech wreck of the early 2000s, a balanced portfolio that was 60% weighted in the S&P 500 and 40% weighted in 7–10-year U.S. Treasuries declined 16.41%, as compared to a fall of 42.46% for the all-stock portfolio. In the global financial crisis (GFC) of 2007-2009, the balanced portfolio lost 23.92% vs. a loss of 45.76% in equities.

The ZIRP Era and the Erosion of Bond Powers

During the GFC, central banks entered hyper-stimulus mode to stave off a collapse of the global financial system and avoid a worldwide depression. ZIRP (zero interest rate policy) stances became the norm for monetary authorities around the world, with rates remaining at historically low levels for the next 14 years.

Bonds eventually became a victim of their own success. Although stimulative policies were successful in making the great recession less severe than would have otherwise been the case, they also robbed bonds of their two key attributes. Firstly, high-quality bonds ceased to offer reasonable yields. Secondly, ultra low rates also limited the ability of bonds to provide capital gains during times of equity market turmoil, thereby hindering their diversification value.

In 2016, PIMCO Co-Founder and “Bond King” Bill Gross commented that to repeat the bond market’s 7.5% annualized return over the past 40 years, yields would have to drop to negative 17%: the math just didn’t work!

A Clear Warning Sign

As the saying goes, “Hindsight is 20/20.” It is easy to understand what should have been done after an event has already happened, even if it was not obvious at the time. However, market behaviour during the Covid crash offered a clear warning that all was not well in bond land.

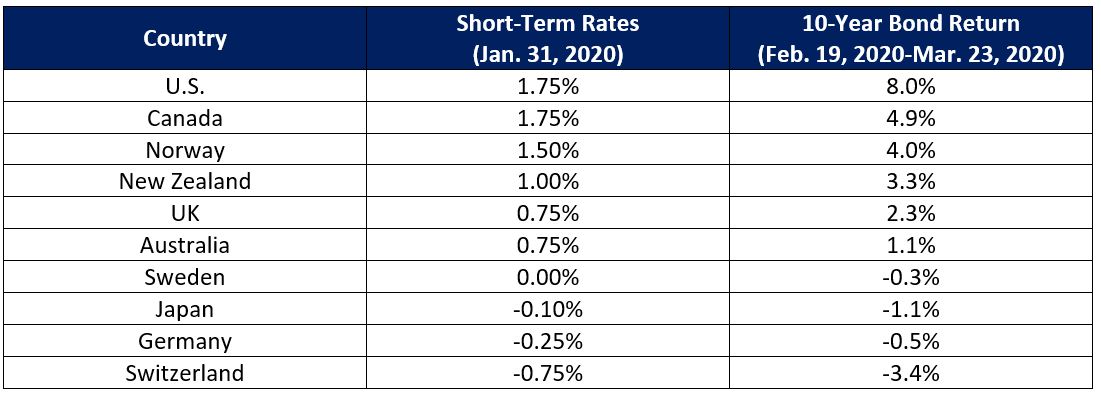

The following table compares countries by their pre-pandemic short-term rates and the returns of their 10-year government bonds during the subsequent bear market.

There is a near perfect relationship across countries in terms of where their short-term rates stood prior to the pandemic and the subsequent return of their 10-Year bonds.

- In the countries that initially had relatively high short-term rates, such as the U.S. Canada, and Norway, 10-year bonds produced substantial gains and mitigated the damage caused by the vicious decline in stocks.

- In countries that started with rates that were neither relatively high nor low, such as the UK and Australia, 10-year bonds provided some, albeit lower amounts of protection.

- Lastly, in countries which started with the lowest rates, such as Sweden, Japan, Germany, and Switzerland, not only did government bonds fail to mitigate stock losses but actually declined.

Given the strong correlation between where pre-Covid rates stood in different countries and the subsequent ability of their bond markets to offset stock market losses, it was clear that there was little, if any, gas left in the tank in the post-Covid world of zero rates, leaving investors largely unprotected.

From Hedge to Texas Hedge

Post-Covid, not only did ultra-low rates obliterate the insurance value of bond holdings, but the unprecedented amounts of monetary and fiscal stimulus that had been injected into the global economy left bonds particularly vulnerable to capital losses. Against this backdrop, when the rubber of stimulus hit the road of inflation in early 2022, central banks were forced to raise rates at a clip not seen since the Volcker era of the 1980s, resulting in painful declines in bond prices. Continue Reading…