By Dale Roberts, CutTheCrap Investing, Retirement Club

Special to Financial Independence Hub

The following is a special to Findependence Hub. This post is derived from a newsletter from Retirement Club for Canadians, re-shaped and enhanced for this audience.

In the Globe & Mail Norm Rothery offered an article with the title – With today’s market, investors close to retirement face precarious times (sub required). Norman Rothery, PhD, CFA, is the founder of StingyInvestor.com.

Retirees typically face the greatest risk in the first few years of retirement. A severe market correction or bout of inflation can permanently impair retirement plans. In fact, the risk for retirees starts several years before the retirement start date, they’re already in the retirement risk zone.

Norm suggested …

“Planning for retirement is tricky at the best of times because it is beset by uncertainties both known and unknowable. High valuations are one of the known problems but that doesn’t make them easy to deal with.”

While a severe market correction early in retirement is a great risk for retirees who will rely extensively on balanced or growth-oriented portfolios, a longer period of low returns can also create risk. The U.S. stock market is trading at worrying levels based on a variety of value factors.

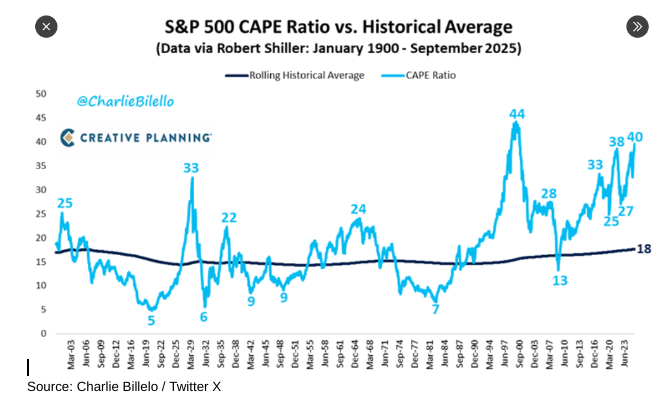

Norm demonstrated that the S&P 500 Index is trading at a cyclically adjusted price-to-earnings ratio near 39, which is approaching the 44 level that we saw in late 1999 as we approached the dot com crash.

Source: Charlie Billelo / Twitter X

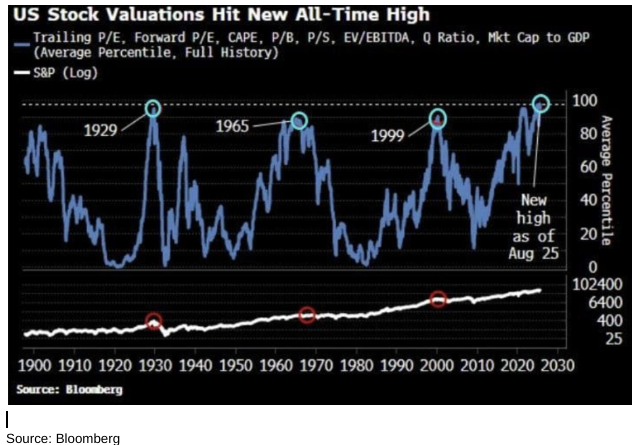

The price-to-sales ratio is approaching its 1999 high.

This ‘everything metric’ says we have the most expensive U.S. market – EVER!

Source: Bloomberg

Dale’s related read: The lost decade for U.S. stocks.

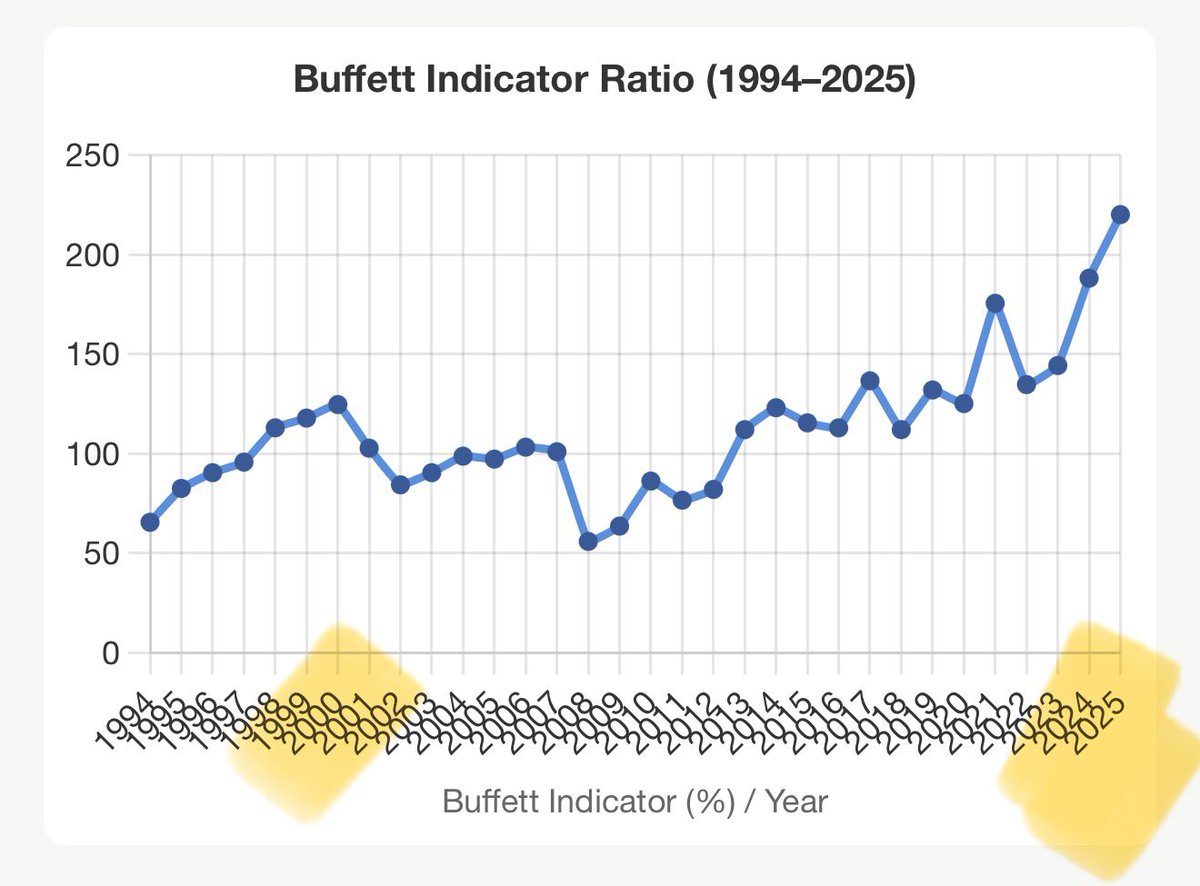

And we can pile on with the Buffett Indicator …

We certainly can’t just step aside and wait for the next recession. Valuation metrics provide no market-timing opportunity. Nothing provides any market timing opportunity. Valuation tends to be a poor near-term market predictor, but it can ‘predict’ the potential returns over the next several years to decade. The data suggest returns for U.S. stocks could be very low in the range of 1-4% annual or even negative in real dollar (inflation-adjusted) returns.

And keep in mind that Canadian stocks (after a very healthy run) are expensive as well. After their big run-up this year, Canadian stocks now trade for nearly 29 times their average inflation-adjusted earnings of the past decade, according to Citigroup, the historical average is 16, TSX returns over the next several years might be challenged as well.

So, there is a risk of a major correction inspired by the lofty levels. And low returns in the first decade can put a strain on the spending plans.

Let’s take a look at how you can address this valuation issue, if you choose to do so.

And in the National Post but via Yahoo!Finance so that you can get a free read …

‘Today, the Shiller ratio is a bit less than 40. The only time it was more than 40 was in 1999 and 2000. It peaked at 44 in December 2019.

Why does this ratio matter for your stock returns? If we compare 40 years of the Shiller P/E ratio and the subsequent 10-year annualized return on the S&P 500, it shows that if the ratio is 32 or higher when you buy, then the likelihood is that the 10-year return ahead will be in the range of minus five per cent to six per cent. If you bought the S&P 500 when the ratio was 20, the likely 10-year returns would be in the five per cent to 15 per cent range.’

Managing the risks in retirement

In a recent Retirement Club newsletter I offered …

‘Of course, this risk can be managed. A global balanced portfolio might still do the trick, but we can also add a U.S. value tilt to the U.S. portfolio. We can reduce our U.S. exposure and use more of the markets that offer better value: Canada and Europe and Asia for example. That said, it is still likely prudent to keep some exposure to the very growth-oriented U.S. market and / or U.S. growth stocks or ETFs.

As we’ve discussed in our risk sessions we can add more cash and bonds and gold. We can desrisk completely if we like, as we pay attention to the long-term growth needs of the retirement cash flow plan. You can build a big cash pile. You can look at defensive equities.’

We’ll explore some options below.

Embrace a variable withdrawal strategy

Continually address your retirement plans and retirement cash flow models.

One of the best strategies is a variable withdrawal strategy. We spend more in the good times and cut back during recession. Even cutting spending by 10% during a market correction can go a long way to securing your longer term spending plans and estate value.

Adaptability is a big reason why retirees should consider adopting variable withdrawal strategies, like the “variable percentage withdrawal” method suggested by Prof. Étienne Gagnon, where the withdrawal rate is updated over time.

Reduce your spend rate in retirement?

In the Globe & Mail piece, Norm pointed to why PWL Capital’s Ben Felix suggests that an initial retirement withdrawal rate somewhere between 2 and 3 per cent, depending on the circumstances, is more reasonable than 4 per cent.

I would disagree with that, because it always depends on the personal circumstances and the retirement cash flow plan. That said, if one retired very early and they are relying on the portfolio almost exclusively, a 3.0 to 3.5% spend rate might be prudent.

You might save more than that you might need according to your cash flow plan.

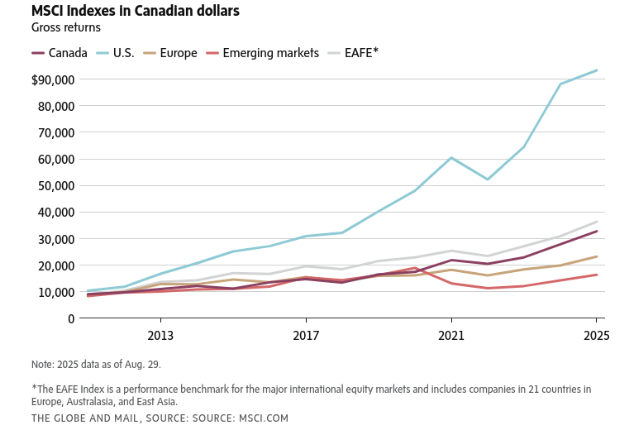

The global portfolio is a tech play?

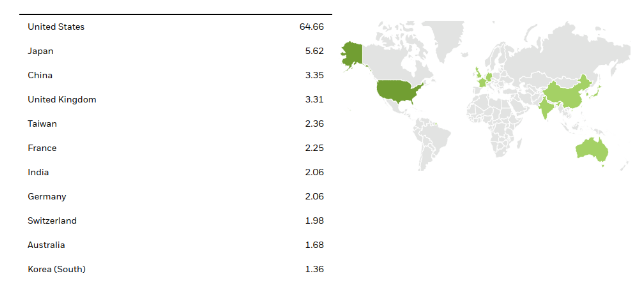

The U.S. stock market represents about 65 per cent of the world’s market by market capitalization based on its weight in the MSCI All-Country World Index at the end of August.

If the U.S. stock market flops, it’ll likely take the rest of the world with it: at least temporarily.

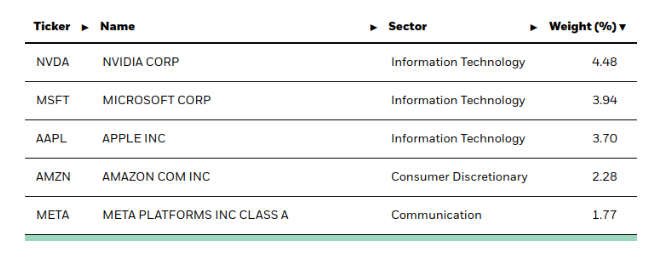

If we look at the popular iShares Global Ex-Canada XAW-T …

You’re holding the U.S. market where technology is by far the largest weighting. Here’s the top 5 …

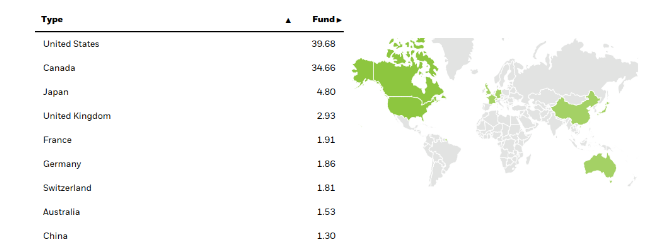

A simple move can be to an asset allocation ETF. And perhaps look at the Balanced Growth models that hold about 20% bonds. Here’s iShares XGRO.

A simple move can be to an asset allocation ETF. And perhaps look at the Balanced Growth models that hold about 20% bonds. Here’s iShares XGRO.

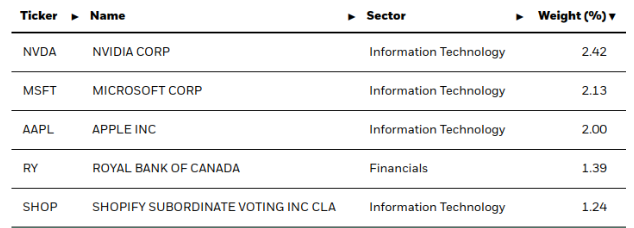

We’re down to 40% U.S. And the top holdings look like this …

We now have two Canadian holdings in the top 5 and we’ve almost cut the top tech holdings weightings in half. XGRO takes some incredible gains and ‘stores them’ in bonds and addresses some of the U.S. overweighting issues.

Add a value tilt to your portfolio

Howard Marks is another billionaire investor whose advice carries great weight in financial circles.

In his latest newsletter, Mr. Marks said it’s time to move to INVESTCON 5, which is a six-point scale of investment risk similar to the military readiness system used by the Pentagon.

“If you lighten up on things that appear historically expensive and switch into things that appear safer, there may be relatively little to lose from the market continuing to grind higher for a while,” he wrote.

Bonds are well-suited as defensive investments, Mr. Marks added.

We can sell some of our U.S. markets or high-valuation growth stocks and ETFs and move the proceeds to U.S. value equities. Pay attention to capital gains and taxation in taxable accounts of course.

We can hold value plays in U.S. Dollar accounts or in Canadian Dollar accounts. About 18 months ago I moved a good slice to iShares Quality U.S. Dividend ETF: XDU-T. At the time the P/E ratio was in the 17 range. The current P/E is still below 20. I’m happy to chip away at that ETF. The sector arrangement is much more conservative. Tech is at a 12.5% weighting, and the fund holds none of the Mag 7.

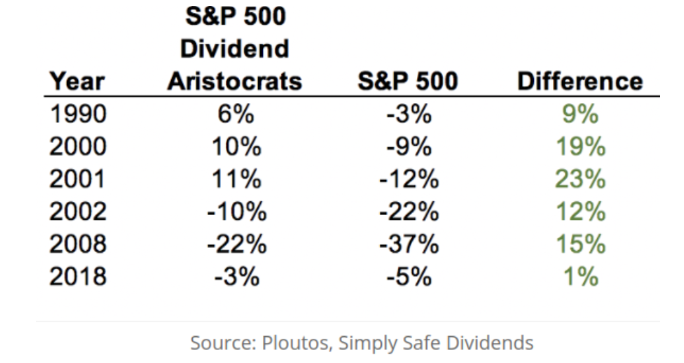

Here’s an example of a Quality Dividend Index during the dot com crash …

In our U.S. Dollar accounts I have trimmed the high-valuation stocks and moved the funds to bonds and stocks that offer sensible valuation levels. For example, building up the Berkshire Hathaways (BRK.B), Pepsis (PEP), RTX Corps (RTX) and Lowe’s (LOW) in the U.S. portfolios.

I am also a big fan of using defensive equities in retirement. They can work in concert with bonds, cash and gold. More weapons = more better ;)

We can use annuities, as a slice of fixed-income bucket to pensionize more of our income. It’s a popular notion to pensionize all of our core spending needs. The pension bucket would include employment pension, CPP and OAS and annuities. You might also look at the Purpose Longevity Pension Fund for a slice of that bucket.

Continue holding some of the market

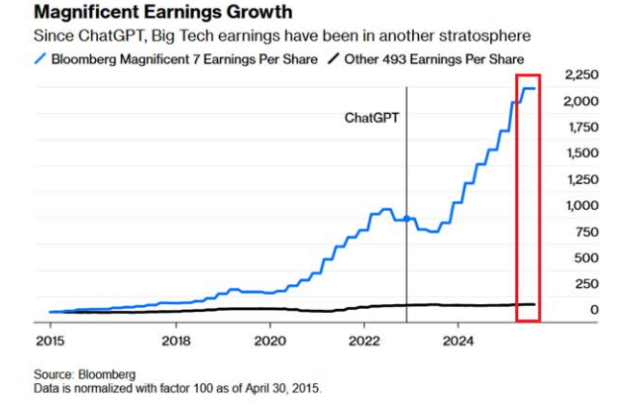

On my blog I’ve long suggested that the U.S. is where they keep most of the best companies in the world. That truth and U.S. advantage has perhaps accelerated in the AI age. It is where they keep the growth, in the U.S. and in AI.

Of course you want to keep a piece of the outrageous growth machines …

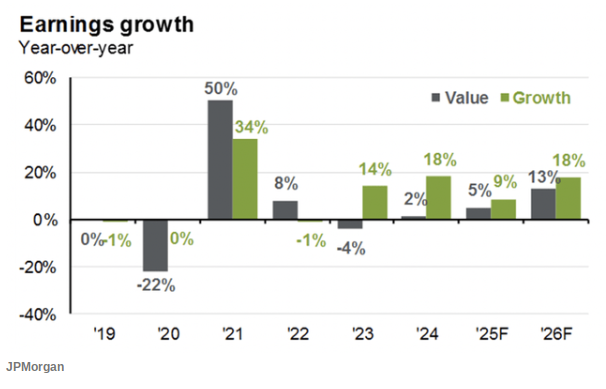

AI is predicted to share the wealth, or create more wealth that is. That could provide a nice tailwind for more value-oriented stocks and index ETFs.

And this chart suggests that value stocks might have an earnings boost tailwind.

That’s why I suggested for many many months, that we don’t bail on U.S. indices and growth indices, but we embrace a global portfolio.

Semi-FIRE / Semi-retirement

Working part time is an option. Yes, it’s called semi-retirement. It can be a wonderful strategy as it provides some money and purpose, and it keeps the brain sharp. It potentially keeps you moving as well if your job has you on your feet mowing lawns or fixing stuff or stocking shelves.

Norm wrapped up his Globe & Mail post with …

‘Unfortunately, investors on the cusp of retirement should be prepared for the possibility of unusually hard times over the next several years and some difficult lessons likely lie in store for all of us. Good luck out there.’

I would add that the key is to be aware and manage risk as you see fit. That said, there is no need to panic. I’ll remind everyone that a balanced portfolio has served retirees very well over the many decades and through troubling times. We can make simple moves that address stretched valuation. We can add inflation protection. In essence we are creating an all-weather portfolio.

As always the above is not advice, but ideas for consideration. Should we consider the valuation of U.S. markets? Have you managed this risk? Please add your thoughts in the comment section for this post. I’ll be sure to stop in to answer all questions or concerns.

Retirement Club

It is a series of monthly Zoom Presentations, newsletters, plus a secure and private online space where we learn, share ideas and chat.

Make sure you’re doing retirement right. It’s also suitable for those who are approaching retirement. Use Contact Dale on his blogs’ home page if you’d like more info, or to sign up. The fee is $250 per year.

Dale Roberts is a former advertising writer and creative director and long time index investor. In 2013, he followed his passion to become an investment advisor, and then trainer at Tangerine Investments. He won Advisor of the Year in his first year. He left Tangerine in 2018 to start Cut The Crap Investing, where he helps investors learn how to use ETFs, simple stock portfolio models and Robo Advisors to full advantage in the accumulation stage, and especially in retirement. A ‘hyper-focuser’ Dale has spent thousands of hours studying retirement – from the financial planning aspects to the portfolio models that make it happen. Early in 2025 he co-founded Retirement Club for Canadians, described in this Findependence Hub blog. Keep in mind Dale is not a financial planner. Retirement Club provides ideas and learning for consideration. As we know, self-directed investors are responsible for their own investment decisions.

Dale Roberts is a former advertising writer and creative director and long time index investor. In 2013, he followed his passion to become an investment advisor, and then trainer at Tangerine Investments. He won Advisor of the Year in his first year. He left Tangerine in 2018 to start Cut The Crap Investing, where he helps investors learn how to use ETFs, simple stock portfolio models and Robo Advisors to full advantage in the accumulation stage, and especially in retirement. A ‘hyper-focuser’ Dale has spent thousands of hours studying retirement – from the financial planning aspects to the portfolio models that make it happen. Early in 2025 he co-founded Retirement Club for Canadians, described in this Findependence Hub blog. Keep in mind Dale is not a financial planner. Retirement Club provides ideas and learning for consideration. As we know, self-directed investors are responsible for their own investment decisions.

Very good article, Dale. I am also a Howard Marks and Norm Rothery fan so perhaps it is my confirmation bias kicking in. My wife had me derisk her RRSP this summer from 100% equities to 80% fixed income. Her RRSP contributions had grown by 11x but it has been been difficult for me to watch the opportunity cost of this move as the market moved higher. She said her RRSP balance was more than enough and already a tax planning challenge. We retired in Sept 2008 but got through the GFC well by using variable consumption, dividends vs selling and using our pre-retirement cash reserves to buy the drop. It wasn’t easy watching our holdings drop ~40% but we kept buying until the reserves were gone. I think taking some cash (10 – 15%) off the table right now could be a good move and your article’s advice is solid.

Hi Colin, sorry I missed your comment. Glad to hear things worked out for you in a very tough correction and recession. I think it will be easy to dodge the next one as well. I continue to rebalance to more defensives including defensive equities.

Thanks for dropping by.

Dale