By Penelope Graham, Zoocasa

By Penelope Graham, Zoocasa

Special to the Financial Independence Hub

When the federal government announced in March that it would be wading into the shared equity mortgage market in efforts to improve home buyer affordability, it stirred up some controversy.

The program, called the First-Time Home Buyer Incentive (FTHBI), was teased in the budget as a ground-breaking approach to helping buyers get into the market by providing interest-free down payment loans of 5% for resale homes, and up to 10% on brand-new builds.

In exchange for the upfront funds, which are designed to reduce the overall size of the mortgage and monthly payments, the Canada Mortgage and Housing Corporation (CMHC) will take an equity percentage the homes’ value, which must be paid off when either the mortgage matures, or the home is sold.

This paid-back amount fluctuates along with appreciation and depreciation in the market. For example, let’s say the CMHC provides a 5% loan of $25,000 for a home purchase of $500,000. The homeowner sells the home several years later, and its value has increased to $550,000. The homeowner would then need to pay the CMHC back $27,500 to reflect 5% of the increased value of the home.

Critics say FTHBI too restrictive to be effective

Mortgage analysts have called the effectiveness of this equity sharing program into question, as the total amount owed to the government could be significantly more than what was loaned in the first place, especially in a market that experiences rapid price growth.

However, the most contested features of the FTHBI are its mortgage and purchase price restrictions, which critics say render the program useless in markets like Toronto and Vancouver where home buyers arguably need the most help.

Buyers who intend to use the FTHBI must satisfy the following requirements to be eligible:

- They must have a combined household income of no more than $120,000

- The mortgage they take out cannot exceed four times their total household income, including the portion provided by the CMHC

- They must qualify for an insured mortgage and have at least a 5% down payment saved

Based on these criteria, a home buyer with the maximum income of $120,000 and a 5% down payment would be limited to a home purchase price of $505,000; that’s not going to have much traction in Canada’s hottest markets, as the benchmark and average prices for both Toronto and Vancouver homes for sale exceed $900,000.

Incentive could only be used to purchase average condo

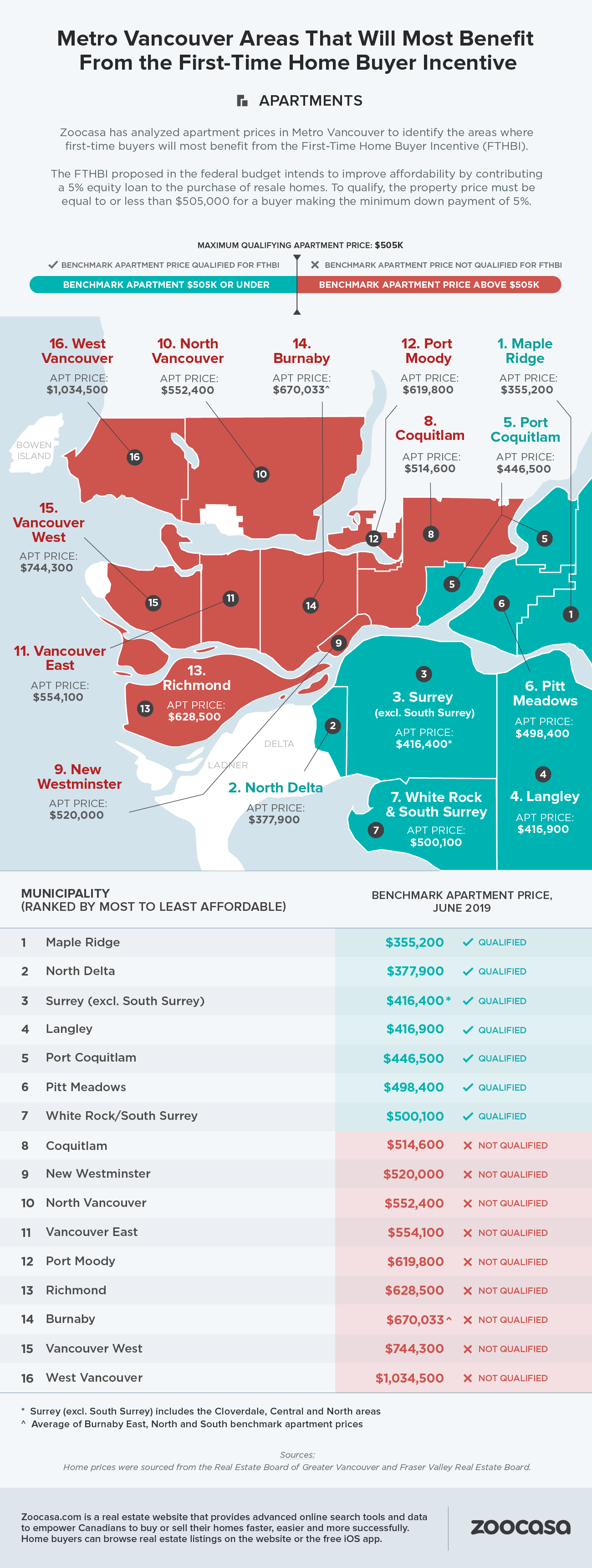

In fact, according to data crunched by Zoocasa, only purchasers of condos located well outside the cities’ cores could hope to utilize the FTHBI; average and benchmark house prices in both locales exceed the $1 million mark, which disqualifies them from both the program and from an insured mortgage perspective.

In fact, according to data crunched by Zoocasa, only purchasers of condos located well outside the cities’ cores could hope to utilize the FTHBI; average and benchmark house prices in both locales exceed the $1 million mark, which disqualifies them from both the program and from an insured mortgage perspective.

According to the data, which analyzed June sale prices reported by the Real Estate Board of Greater Vancouver and the Fraser Valley Real Estate Board, those hoping to use the FTHBI to purchase Vancouver condos have options in just seven out of the 16 municipalities studies.

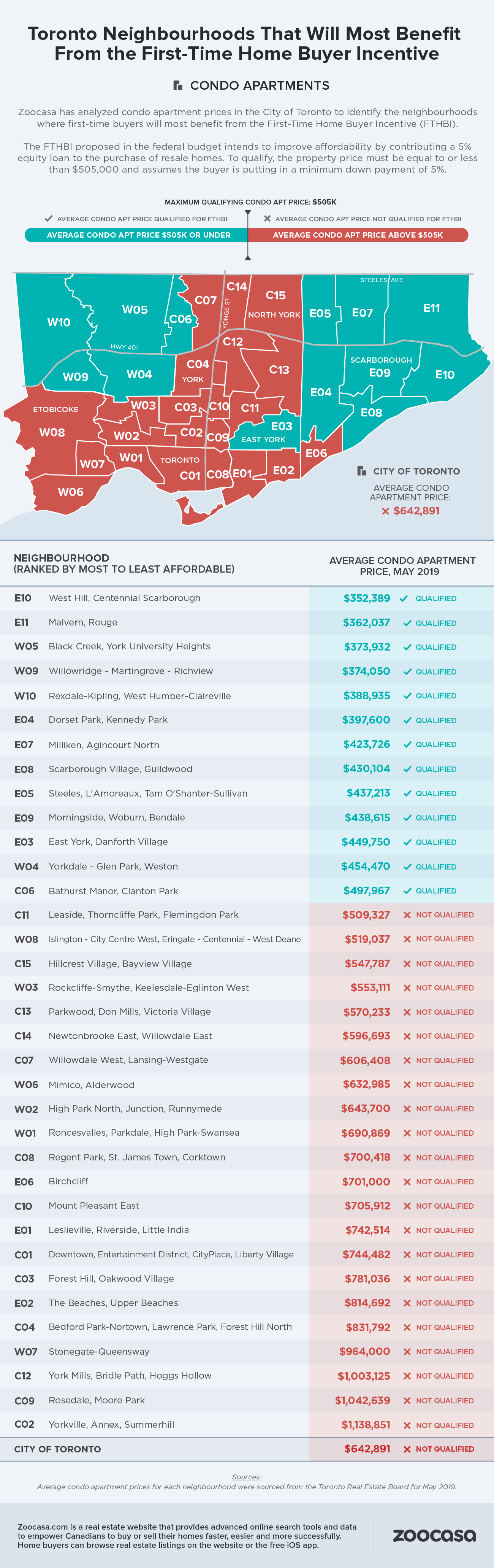

Given Toronto’s larger geographical scope, buyers have a larger selection of neighbourhoods with eligible housing stock; qualifying condos can be found in 13 out of the city’s 35 municipalities, at an average below the $500,000 price point. Sold home prices were sourced from the Toronto Real Estate Board for the month of May.

Check out the accompanying infographics to see where the FTHBI could be feasibly used in Toronto and Vancouver.

Penelope Graham is the managing editor of Zoocasa.com, a real estate resource “that uses full brokerage service and online tools to empower Canadians to buy or sell their home faster, easier and more successfully.”

Penelope Graham is the managing editor of Zoocasa.com, a real estate resource “that uses full brokerage service and online tools to empower Canadians to buy or sell their home faster, easier and more successfully.”