By Dale Roberts, Retirement Club/Cutthecrapinvesting

Special to Financial Independence Hub

It has been more than two weeks since the U.S. attacked Iran. And while the U.S. was quick to knock out much of Iran’s traditional military capability, Iran has turned to asymmetric war and has also weaponized oil, fertilizers and other materials that pass through the Hormuz Strait. With threats and some strategic attacks on shipping, Iran has essentially closed the Hormuz Strait. About 20-25% of the world’s oil and a third of the world’s fertilizer needs flow through the Strait. We now face a potential energy shock and there are rumblings that we might experience a period of stagflation. In the 1970s an energy crisis created the conditions for stagflation. How do we defend against stagflation?

As always, the following is not advice.

First off, and as always, no one knows what will happen. No one knows how this war will proceed and what it will mean for investment assets and the economies of the world. Trump could announce today that he’s packing up and heading home or this could continue for years. That said, history does teach us how assets react. History teaches us how to hedge most any threat.

What is Stagflation?

Stagflation happens when several factors combine to create an especially difficult economic environment. To get stagflation, three things must occur together:

- Slow economic growth

- High inflation

- A high unemployment rate

Stagflation is an economic double-whammy where stagnant growth and high unemployment collide with rising inflation. This rare, painful cycle is difficult to fix because traditional policies to lower inflation often worsen unemployment, and vice versa.

In Canada’s case we’d say we are economically up Schitt’s Creek. Investopedia does a decent job of explaining what is stagflation and why it is nasty.

Here’s a very good overview from RBC: On the horns of the stag.

Wars and the portfolio

Market strategists have been quick to point out that rarely do conflicts have any long-lasting impact on stock prices. In 20 major episodes since the Second World War compiled by analysts at RBC Wealth Management, the S&P 500 index fell by an average of just 6 per cent.

The outliers in that list, however, involve major oil market disruptions, like the Arab oil embargo in 1973 and the Iraqi invasion of Kuwait in 1990. We had more significant drawdowns.

For accumulators, they should stick to the investment plan. We should always be compounding.

At Retirement Club for Canadians and in our secure online community space, I shared this message …

It has been the most common message on this blog: get an investment plan and stick to it like glue. Here’s the full graphic that was shared at Retirement Club (and on X (Twitter).

War is something we can ignore like every other risk, when we have our stock-solid investment plan and retirement plan.

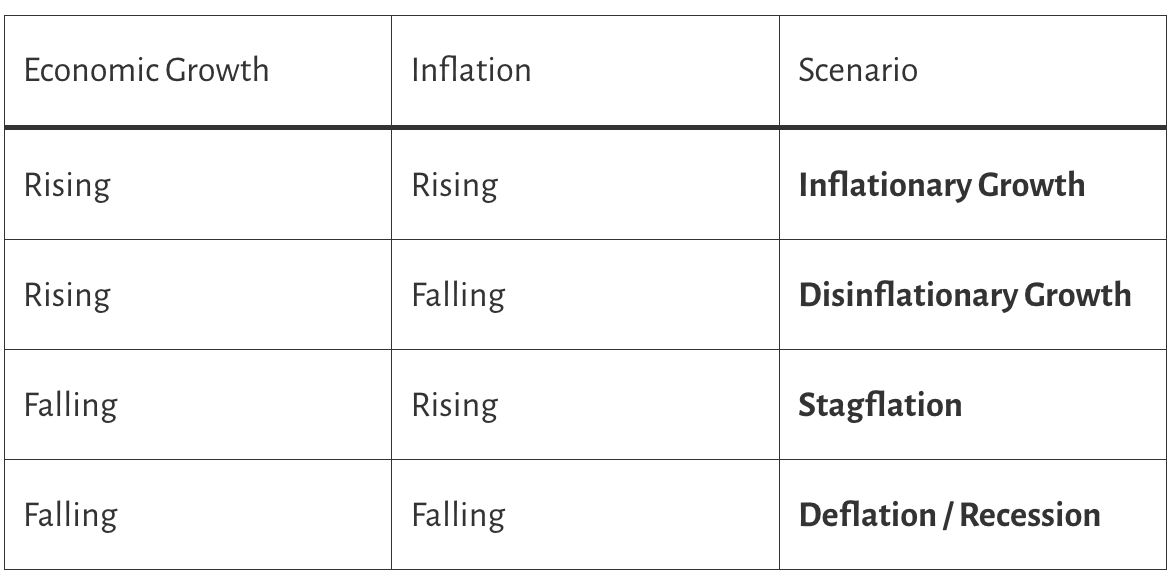

The 4 economic scenarios

The economy can shift along two axes:

- Economic growth (rising or falling)

- Inflation (rising or falling)

Combining them gives four possible economic scenarios:

1. Inflationary Growth

Growth ↑ + Inflation ↑

- Economy expanding strongly

- Demand pushes prices higher

- Often occurs during late expansions

Assets that tend to do well

- Commodities

- Real estate

- Some stocks

Example period: parts of the global economy during the early 2000’s commodity boom.

2. Disinflationary Growth

Growth ↑ + Inflation ↓

- Economy grows but inflation stays low or falls

- Considered the best environment for stocks

Assets that tend to do well

- Stocks

- Growth companies

- Corporate credit

- Bond market

Example: much of the period after the Global Financial Crisis recovery.

3. Stagflation

Growth ↓ + Inflation ↑

- Economy slows but prices keep rising

- Very difficult for policymakers

Assets that tend to do well

- Commodities

- Gold

- Inflation-protected assets

- Oil and gas stocks

Classic example: the 1970’s Oil Crisis.

4. Deflation / Recession

Growth ↓ + Inflation ↓

- Demand collapses

- Prices and wages fall

- Debt burdens become heavier

Assets that tend to do well

- Government bonds

- Cash

- Defensive assets

Example: the Great Depression and recessions

Fortunately we are almost always in scenario 2 and some of scenario 1. High inflation and stagflation is rare. Deflation or a Depression is rare and market recessions shown in scenario 4 is why many will embrace bonds and cash to create a balanced portfolio that is lower risk.

Most investors are not prepared for stagflation or extended periods of high inflation. They have a portfolio hole, they do not hold an all-weather portfolio that covers all 4 economic quadrants. In that all-weather post you’ll find charts such as …

But gold ruled during stagflation. From the beginning of this blog I have shown you that gold makes the balanced portfolio better.

Déjà vu all over again? Here’s now markets have performed during the recent oil shock and stagflation fears.

You might look to small-cap value as well.

More on types of stocks during stagflation

Equity assets – –

Prepared for oil wars and shocks

When I asked you again in October of 2025 if – You got oil and gas stocks? I began with …

This post is not a reaction to the rising political tensions in the Middle East, with the U.S. targeting Iranian nuclear sites on the weekend. Mostly, ‘got oil and gas stocks’ is a common question on this blog. You’re then ready for an oil shock.

And here we are today, potentially facing an oil shock. With XEG-T, you’d be up about 40% from the time of that post. The markets think ahead of course and moved up as the Iran military operation threat increased as the U.S. moved military assets into The Middle East.

Building the all-weather portfolio

Most portfolios do not include inflation-fighting assets (in a meaningful way). Thanks to ETFs you can easily bolt on dedicated inflation fighters. In fact you can do that by way of one ETF.

The Purpose Investments one-stop stagflation fighting ETF, PRA-T.

PRA was up 2.8% last week, and up 18.8% in 2026. It’s doing its thing. The fund performed very well during the inflation scare that we experienced in 2021 and 2022. The following is a price-only chart, not including dividends.

You could bolt on PRA to your existing portfolio.

We can also see that PRA was a weak performer from 2013 and into 2021. That’s to be expected. We were in a low-inflation environment. Inflation levels bounced around in modest fashion, but remained low. That’s ordering up a Number 2 from the economic quadrant listed above. That’s the time for stock markets to shine, and they did. VT is global stocks in U.S. Dollars. That said, inflation made a modest move higher in 2018 and stocks ‘didn’t like it.’ Rates then fell into 2020, stocks followed the script and moved higher.

With dividend reinvestment PRA did tread water over the period offering a minuscule 5% return. Bonds provided solid performance as expected, during a falling rate environment.

Do you need a stagflation hedge?

In the accumulation stage, the goal is simple. Make the most money while investing within your risk tolerance level. Given the penchant for inflation-fighting assets to lag during periods of low inflation and disinflation, you might take a pass. We are usually experiencing inflationary growth or low inflation / disinflation. We know that equities thrash inflation over time because we are usually in these environments. Your weapons are time and the ability to buy equities as they go on sale.

It’s my opinion that retirees and those in the retirement risk zone should consider a dedicated stagflation / high inflation hedge. Inflation is a massive risk in retirement.

In retirement your Asset Allocation decisions will be addressed account by account, and based on your retirement cash flow plan. Each account will have different marching orders.

Be sure to understand the risks on all fronts. It’s your decision to make.

Building a simple all-weather portfolio

It could be as easy as adding PRA-T to an asset allocation ETF.

For example:

- 80% XBAL / 20% PRA

- 85% XBAL / 15% PRA

You can certainly use individual inflation assets such as:

- Gold: KILO-T

- Energy: XEG-T / PPLN-T / XUT-T

- Commodities (equities): XMA-T

A Canadian Dollar All Weather Portfolio Example

Once again, this is not advice but:

- 20% XIC-T

- 17.5%% XUS-T

- 17.5% XEF-T

- 10% CBIL-T

- 10% XFLB-T

- 5% KILO-T / 5% XEG-T / 5% PPLN-T / 5% XMA-T / 5% XUT-T

Defensive equities can do double duty, offering lesser drawdown (or positive returns) during a recession / deflation, plus there’s the potential of a benefit during high inflationary periods as well. Canadian consumer staples are available by way of iShares XST-T. We can put the pipelines and utilities (used above) in the defensive camp.

For U.S. Dollar Accounts here’s the Ray Dalio All Weather Portfolio.

Here’s an interesting look at the performance history …

I have penned and Tweeted on our personal approach.

My Canadian RRSP shows similar performance. It’s nice to know we have no energy shock or stagflation risk. We use or have recently used gold, PRA-T and commodities ETFs. I like some bitcoin in the mix as well in my accounts.

I also shared the asset mix – My energy portfolio is $CNQ $SU $IMO $TOU $ENB $TRP $HUTS (yes Telcos are in that mix via HUTS).

Quick resolution?

The futures market (the experts) are predicting a relatively quick resolution with oil prices coming down over the next several months. Let’s hope they are right.

All-weather portfolios won’t care much on how that turns out. I will not be sweating it this Spring and Summer. If we’re paying $2 a litre at the pumps, I’ll be cashing in.

Join Cut The Crap Investing

You can follow this blog, it’s free. Newsletters, plus other free content and ‘ideas’ will be delivered to your email inbox. Enter your email in the subscribe area, or ‘join us today’ on the home page.

ETF Portfolios / Stock Portfolios / Retirement Strategies / Wealth Creation/ Retirement Club

Join Retirement Club 2026

Do retirement right. … a series of monthly Zoom Presentations, newsletters, plus a secure and private online space where we learn, share ideas and connect with members. Here’s the Retirement Club overview page. There are just a few spots remaining for the 2026 retirement-changing sessions. You can join us for a Zoom Tour of Retirement Club this coming week. We’ll offer a couple of time slots.

Hit Contact Dale at top right of this page for details.

We’ll take you through the three pillars of Retirement Club.

Make sure you’re doing retirement right. It’s also suitable for those who are approaching retirement, we need to prepare in advance and understand what we’re ‘getting into’.

While I do not accept monies for feature blog posts please click here on the mission and ‘how I might get paid’ disclosures. Affiliate partnerships help me (try to) pay the bills for this site. But they don’t, ha. That will allow me to keep this site free of ads and easy to read.

Dale Roberts is a former advertising writer and creative director and long time index investor. In 2013, he followed his passion to become an investment advisor, and then trainer at Tangerine Investments. He won Advisor of the Year in his first year. He left Tangerine in 2018 to start Cut The Crap Investing, where he helps investors learn how to use ETFs, simple stock portfolio models and Robo Advisors to full advantage in the accumulation stage, and especially in retirement. A ‘hyper-focuser’ Dale has spent thousands of hours studying retirement – from the financial planning aspects to the portfolio models that make it happen. Early in 2025 he co-founded Retirement Club for Canadians, described in this Findependence Hub blog. Keep in mind Dale is not a financial planner. Retirement Club provides ideas and learning for consideration. As we know, self-directed investors are responsible for their own investment decisions. This blog originally appeared on his site on March 17, 2026 and is republished with permission.

Dale Roberts is a former advertising writer and creative director and long time index investor. In 2013, he followed his passion to become an investment advisor, and then trainer at Tangerine Investments. He won Advisor of the Year in his first year. He left Tangerine in 2018 to start Cut The Crap Investing, where he helps investors learn how to use ETFs, simple stock portfolio models and Robo Advisors to full advantage in the accumulation stage, and especially in retirement. A ‘hyper-focuser’ Dale has spent thousands of hours studying retirement – from the financial planning aspects to the portfolio models that make it happen. Early in 2025 he co-founded Retirement Club for Canadians, described in this Findependence Hub blog. Keep in mind Dale is not a financial planner. Retirement Club provides ideas and learning for consideration. As we know, self-directed investors are responsible for their own investment decisions. This blog originally appeared on his site on March 17, 2026 and is republished with permission.