And it’s whispered that soon if we all call the tune

Then the piper will lead us to reason

And a new day will dawn for those who stand long

And the forests will echo with laughter

- Stairway to Heaven, by Led Zeppelin

By Noah Solomon

Special to Financial Independence Hub

At the end of last year, the S&P 500 Index was valued at about 23 times estimated earnings over the coming year, which was significantly above its historical average. By mid-March of this year, the index had declined by roughly 10%, driven by unspectacular economic growth, inflation rates that remained stubbornly high, and related concerns that valuations reflected unwarranted optimism.

These growing concerns morphed into widespread panic on April 2nd, when the U.S. imposed tariffs on imported goods that were more severe than had been anticipated. Broad-based fears that tariffs would cause higher inflation, slower growth, or perhaps even a recession spurred a sharp drop in stock prices, with the S&P 500 falling another 5%, bringing its year-to-date loss to 15% at its low point on April 8th.

Fast forward to the present, and all is once again right in the world. The U.S. administration delayed many tariff deadlines, and those tariffs that have been imposed are below the levels that were initially announced. In addition, the feared inflationary impact of tariffs has not yet materialized. These better-than-expected developments have soothed markets, with the S&P 500 advancing 35% from its low point of the year, leaving its year-to-date gains at nearly 15% as of the end of September.

The trillion-dollar question is whether markets are currently reflecting realistic expectations. To the extent that sensible assumptions regarding risk and reward are embedded in current security prices, investors should stay the proverbial course. Conversely, portfolio adjustments are warranted if expectations are unreasonably optimistic.

Not all FOMO is Created Equal

Emotions and behavioral biases have exerted and will always exert a huge influence on investors’ decisions. Perhaps one of the most common among these is fear of missing out (FOMO), which is “the anxiety or apprehension that one is missing out on rewarding experiences, information, or events that others are having.”

Whereas FOMO can often be irrational, thereby leading to poor decisions and results, at times it can be a positive force, spurring investors to act in ways that can bolster returns.

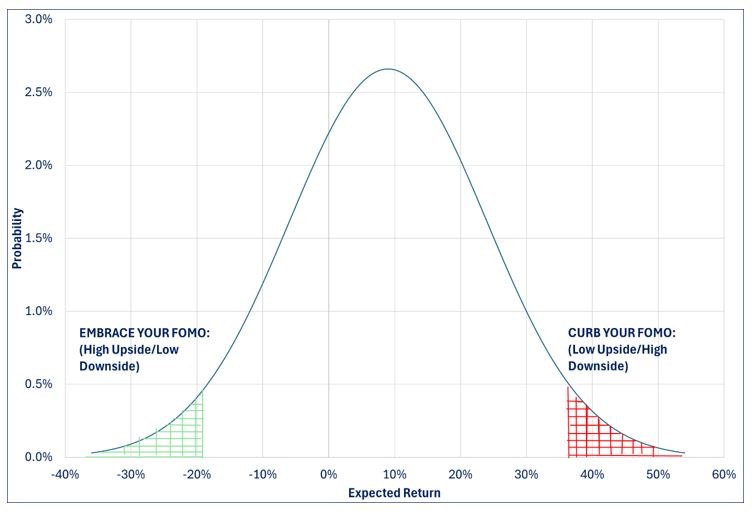

Embracing vs. Shunning FOMO: It’s all about the Odds

Historically, when markets have been saturated with a “nothing can go wrong/it can only go up” mindset, returns over the ensuing several years have fallen somewhere between subpar and negative. In such environments, those who have tempered their FOMO have achieved better returns than those who have not. Conversely, when markets have been replete with a “things can only get worse/the sky is falling” mentality, returns over the next few years have been significantly higher than average. In such circumstances, investors who have embraced their FOMO have reaped significant rewards.

If only things were so simple

Clearly, you can achieve better than average results from taking less risk when prospective returns are below average and from taking more risk in environments where prospective returns are above average. Unfortunately, there is no precise gauge (or collection of gauges) that offer any degree of certainty or precision with respect to either of these extremes.

However, history strongly suggests that there is a reasonable proxy for estimating future returns and risks over the medium to long-term. At times when valuations have stood well below average levels, returns over the next several years have tended to be well above average. Conversely, at times when multiples have been materially above average, returns over the next several years have ranged from below average to negative.

Notwithstanding the historical track record and economic rationale of having a higher allocation to stocks when they are “on sale” and tempering your allocation to equities when they are expensive, doing so can be challenging from a behavioural perspective.

Abnormally high valuations tend to be both the result of and accompanied by the most pronounced instances of FOMO. On the other hand, equities tend to go on sale during the tail end of bear markets, when feelings of despondence prevail and investors are generally concerned with preserving capital rather than missing out. In other words, FOMO is most likely to be embraced when it should be avoided and is most likely to be shunned at times when it should be embraced.

This paradox is arguably the single greatest cause of bubbles and busts. It is also perhaps the greatest source of opportunity for those who can control or embrace their FOMO accordingly.

Buffett best described investors’ reticence to check their FOMO as follows:

“The line separating investment and speculation, which is never bright and clear, becomes blurred still further when most market participants have recently enjoyed triumphs. Nothing sedates rationality like large doses of effortless money. After a heady experience of that kind, normally sensible people drift into behaviour akin to that of Cinderella at the ball. They know that overstaying the festivities — that is, continuing to speculate in companies that have gigantic valuations relative to the cash they are likely to generate in the future — will eventually bring on pumpkins and mice. But they nevertheless hate to miss a single minute of what is one helluva party. Therefore, the giddy participants all plan to leave just seconds before midnight. There’s a problem, though: They are dancing in a room in which the clocks have no hands.”

He also describes the benefits of embracing FOMO when excessive fear and pessimism create opportunities, stating, “Cash combined with courage in a time of crisis is priceless.”

You are almost Certain to be Wrong … But Good is NOT the Enemy of Great

There are no sure things in markets. However, one thing of which I am confident is that if you alter your equity exposure in response to either excessively high or low valuations, you are almost certain to be wrong … at least over the short term.

Nobody can time markets perfectly. This typically necessitates some regret when prices rise after you reduce your equity exposure in response to overly optimistic markets. Similarly, it almost always entails feelings of remorse when prices fall after you increase your stock holdings to take advantage of environments where stocks go on sale.

However, you need not have perfect timing to achieve better than average returns by making portfolio adjustments in response to extreme events at either end of the valuation spectrum. Good is not the enemy of great: you don’t need to pick exact tops and bottoms to add significant value through market cycles over the long term.

There are no Bargains … But there are some Relative Ones

At the end of 2024, U.S. stocks stood near their highest valuations over the past 25 years, save for the peak of the dotcom bubble of late 1990s/early 2000s. From 1987-2014, whenever valuations were at levels approximating those that currently prevail, average annual returns over the subsequent ten years were between plus 2% and minus 2%, without exception.

Although earnings expectations have risen over the past several months, prices are up more, thereby leaving valuations even higher than the already elevated levels that prevailed at the beginning of the year. Buffett’s favorite indicator – the ratio of aggregate market capitalization of U.S. stocks to U.S. GDP – recently surged above 200%, a level he once warned is like “playing with fire.”

Paradoxically, higher valuations have coincided with an investment environment that I believe is less hospitable than that which prevailed when the year began. While tariffs have not been as bad as initially feared, it is nonetheless likely that current U.S. trade policies have had a deleterious impact on the multi-year trajectory of the economy. Corporate profits will on balance be hindered by lower margins, less demand for their products, or some combination of both. U.S. equities, which began the year at precarious levels, have become even more expensive in the face of what I believe to be a less favourable growth backdrop, which does not bode well for future returns.

While stocks outside the U.S. are by no means a bargain, nor are they unreasonably valued. Canadian, Eurozone (including the UK), and Japanese equities are currently valued at levels which are normal from a historical perspective. However, they are a bargain relative to U.S. stocks. While non-U.S. developed stocks have typically been valued at a 10% discount to their U.S. peers, their current discounts are far greater. Canadian companies are currently priced at a 26% discount, while Eurozone and Japanese stocks are even more of a bargain, trading at 40% and 36% discounts, respectively.

Putting these discounts into perspective, Canadian stocks stand in the 16th percentile in terms of their relative valuations to U.S. stocks over the past 25 years, while Eurozone and Japanese equities stand in the 5th and 6th percentiles, respectively. Although these historically wide discounts may prove meaningless over the short term, historical patterns strongly suggest that they foreshadow significant outperformance over the next several years.

Noah Solomon is Chief Investment Officer for Outcome Metric Asset Management Limited Partnership. From 2008 to 2016, Noah was CEO and CIO of GenFund Management Inc. (formerly Genuity Fund Management), where he designed and managed data-driven, statistically-based equity funds. Between 2002 and 2008, Noah was a proprietary trader in the equities division of Goldman Sachs, where he deployed the firm’s capital in several quantitatively-driven investment strategies.Prior to joining Goldman, Noah worked at Citibank and Lehman Brothers.

Noah Solomon is Chief Investment Officer for Outcome Metric Asset Management Limited Partnership. From 2008 to 2016, Noah was CEO and CIO of GenFund Management Inc. (formerly Genuity Fund Management), where he designed and managed data-driven, statistically-based equity funds. Between 2002 and 2008, Noah was a proprietary trader in the equities division of Goldman Sachs, where he deployed the firm’s capital in several quantitatively-driven investment strategies.Prior to joining Goldman, Noah worked at Citibank and Lehman Brothers.

Noah holds an MBA from the Wharton School of Business at the University of Pennsylvania, where he graduated as a Palmer Scholar (top 5% of graduating class). He also holds a BA from McGill University (magna cum laude). Noah is frequently featured in the media including a regular column in the Financial Post and appearances on BNN. This blog originally appeared in the September 2025 issue of the Outcome newsletter and is republished here with permission