Eight years ago, I bought 15 U.S. dividend growth stocks as a real-life portfolio demonstration. More than a demonstration, it was the total value of our U.S. holdings in our retirement accounts. The strategy was to create a more defensive and retirement-ready portfolio. The portfolio slants to quality, profitability and business moats. The 15 stocks were added to three companies that were already held – we’ll call those stock picks. The portfolio mix beat the S&P 500 by 3.2% annual while delivering better risk-adjusted returns.

Here’s the link to my recent Seeking Alpha article – the dividend growth portfolio 8 years later. You might be able to get one of three free reads for that post on Seeking Alpha. But just in case you can’t I will share a few of the key details.

And keep in mind the post and stocks that I mention is not advice. Do your own research, and know why you do what you do.

The U.S. dividend growth, plus picks portfolio

I sold my VIG, and purchased 15 individual holdings from the top 20-25 of the index. The 15 companies that I added are 3M (MMM), Pepsi (PEP), CVS Health Corporation (CVS), Walmart (WMT), Johnson & Johnson (JNJ), Qualcomm (QCOM), United Technologies (UTX), Lowe’s (LOW), Walgreens Boots Alliance (WBA), Medtronic (MDT), Nike (NKE), Abbott Labs (ABT), Colgate-Palmolive (CL), Texas Instruments (TXN) and Microsoft (MSFT).

I also have 3 U.S. stock picks by way of Apple (AAPL), Berkshire Hathaway (BRK.B), and BlackRock (BLK). For the record, these stocks are held in my wife’s accounts and my own accounts.

United Technologies merged with Raytheon (RTX) and then spun off Carrier Global Corporation (CARR) and Otis Worldwide (OTIS). We continue to hold all three and they have been wonderful additions to the portfolio. In fact, from the time of the spin-off, the 3 stocks have greatly outperformed the market (IVV) and the dividend achievers. Given that the United Technology stocks are not available for evaluation from 2015, I have run the performance update with the remaining 14 dividend achievers. Continue Reading…

One of the most agreed-upon financial planning concepts is the importance of an emergency fund. Having quick access to money to pay for an unexpected expense or job loss can prevent unwanted credit card debt and can lower stress levels.

Not everyone is on board though. Some people feel that keeping money in cash instead of investing it means you’re sacrificing too much potential growth. This might be a particularly true for people who are targeting financial freedom. Since investing is an important component of reaching financial goals, it’s understandable that you don’t want to drag down your overall rate of return by holding cash.

Having access to money for unexpected expenses, though, is important for pretty much everyone. So do you need an emergency fund and if you do, how much should it be?

Do you need an emergency fund?

If you have a home equity line of credit (HELOC), you might not need funds sitting in a savings account. Whether it’s a good idea to depend on your HELOC as an emergency fund depends on two main factors: if you had to borrow from it, how long would it take you to pay if off and what is the rate of interest you’re paying?

Generally, as long as the rate of interest on the line of credit is below what you could expect to earn in the stock market, and assuming you’re able to pay down the line of credit within a reasonable time period, then using your line of credit isn’t a bad idea. The key is to make sure you are disciplined in paying down the line of credit quickly, otherwise the interest cost will outweigh what you could earn in the market.

How much do you need?

For those who don’t have a HELOC or who prefer to have a safety net in cash, determining the right amount of money to keep in an easy-to-access, low-return account is important.

There are really two kinds of emergency funds: one that will pay your expenses if you lose your job or can’t work for a period of time, and one that will pay for the large, unpredictable expenses that crop up in everyday life.

The job loss emergency fund

Job loss can mean you were laid off or that you can’t work due to illness, an accident, or a personal/family crisis. You might have heard the standard advice that says you need 3-6 months’ worth of living expense to protect against a job loss. Like all personal finance shortcuts, this isn’t necessarily helpful. How much you need in an emergency fund is highly dependent on your situation.

Here are the main factors that influence how much you should have set aside in your job loss emergency fund:

Do you have job stability? If your industry is known for sudden layoffs or if your role might be considered non-essential to an organization, you have a higher risk of losing your job and it might take you longer to find a new one. It would be wise to have a bigger cushion than someone who works in a stable industry or performs an essential role.

Do you have disability insurance? If you have an accident or get really sick, you’ll receive some kind of payment while you have to take time off work. It won’t necessarily be enough but it will help and you’ll need a smaller emergency fund. If you expect to receive no pay if you need to take time off work, you need a bigger emergency fund.

What kind of lifestyle do you want to maintain? If you are laid off, you’ll need to pare back your spending. But to what extent? What do you consider to be “essential”? Are the kids’ swimming lessons essential? What about your gym membership? Understanding what essential means to you will help you decide how much to set aside.

Do you have a partner or spouse? If you have a partner or spouse with whom you share the financial responsibilities of running a household and they are employed, would they be able to cover the essentials if you lost your job? How would your lifestyle be impacted? What is their job stability like? Do they work in the same industry as you do? If so, there might be a higher risk of both of you being laid off at the same time.

Do you have savings in a TFSA or a non-registered account? If all of your money is in RRSPs or your pension, you don’t have any good options for withdrawing money in an emergency. However, you could choose to rely on your TFSA or non-registered funds for a portion of your needs.

The large expense emergency fund

For your large expense emergency fund, the amount you want to have available depends on how many opportunities for unexpected expenses you are exposed to and what other resources you could draw on. Continue Reading…

Central banks across the globe are likely to continue with their attempts to tame inflation by hiking interest rates, crushing the hope that markets will return to normality any time soon.

With the unemployment rate at a historically low level, inflation remains a top concern for the Bank of Canada (BoC) and the Federal Reserve (Fed), who are also dealing with looming risk of a recession and uncertainty regarding the impacts of the recent bank turbulence. The BoC and the Fed appear to be ahead of global peers in their attempt to slowdown inflation – raising the question around whether we have seen the peak in rates in North America.

The rapid tightening cycles by policy makers are reinforcing the appeal of owning high-

quality ultra-short bond, and money market ETFs. A series of recent rate hikes by the Bank of Canada and the Federal Reserve gave a boost to yields for these products, making the saying “cash is king” true to a certain extent, as investors who are worried about higher inflation and slowing growth prefer investing in these cash alternatives to ride out the market volatility. In today’s market, you can earn an attractive yield while taking less risk – earning while you wait for volatility to subside.

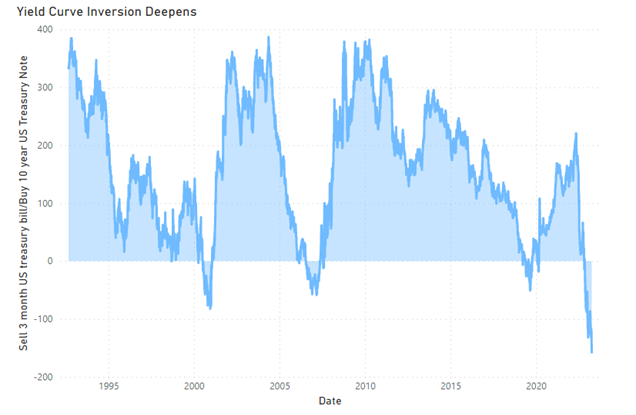

Yield curve[1], are we in love with the shape of you?

Normally, the yield curve is upward sloping, meaning longer-term bonds yield more than shorter-term bonds as investors often demand higher yields for locking their money up for a longer period. However, at present, the shape of the yield curve is inverted, which means shorter-term securities are yielding more than longer-term ones. This inversion is largely owing to the Central Bank’s quest to reduce inflation by hiking the interest rates.

Due to historically low interest rates in the last few years, investors were compelled to take more duration[2] risk by adding exposure to longer-term bonds and higher credit risk[3] by investing in lower credit quality segments such as high-yield or emerging markets bonds. However, due to the current yield curve inversion, the tables have turned now, offering a unique opportunity for fixed-income investors looking to earn higher yields.

Source: Bloomberg USYC3M10 Index (Sell 3 Month US T-bill & Buy 10 Year US Bond Yield Spread) Sep 1992 to April 2023

Why stash cash in money market & ultra-short-term bond ETFs?

The front-end of the yield curve (0-1yr) offers an attractive asymmetry and opportunity to capture yield between 4-5% + with limited duration and credit risk. This allows investors to earn the highest yields we’ve seen in more than a decade on fixed income and build a more stable high-quality fixed-income portfolio by adding exposure to ultra-short investment grade bonds and money market securities. Based on the current interest-rate volatility, hugging the front-end of the curve seems a more prudent and consistent way to preserve capital in a fixed-income allocation. BMO ETFs offers solutions such as BMO Money Market Fund ETF Series (ZMMK), BMO Ultra Short-Term Bond ETF (ZST) and BMO Ultra Short-Term US Bond ETF (ZUS), which are a great way to get exposure to the front end of the curve.

These money market & ultra short-term bond ETFs invest in high credit-quality instruments that provide a great degree of safety and capital preservation. Firstly, by investing in securities that mature in less than one year, the duration risk is minimal, which results in lower interest rate sensitivity in your portfolio. Secondly, these ETFs offer high liquidity[4] due to the nature of their underlying securities, which means they can be bought and sold easily with minimal market impact. Continue Reading…

Portfolio Manager explains why US banks have struggled, where opportunities might appear, and how investors can benefit from short-term volatility.

Image from Pixabay: Wendy Soon

By James Learmonth, Senior Portfolio Manager, Harvest ETFs

(Sponsor Content)

The US banking sector is facing uncertainty. In the wake of the collapse of Silicon Valley Bank in March of 2023 — and deposit liquidity issues at other regional banks — the whole US banking sector has suffered some significant stock market setbacks.

In those setbacks, however, investors may see opportunities, especially when we consider the scale and importance of the US banking sector. Of the 30 banks included in the global list of systemically important financial institutions, colloquially referred to as “too big to fail,” eight are based in the United States.

With those titans as ballast, investors may be able to find growth opportunities in US banking, if they understand why the sector is struggling now, where the upside could come from, and find a strategy suited to short-term volatility.

For someone seeking to take advantage of the dislocation we’ve seen in the US banking sector, a diversified approach is absolutely something you may want to look at. Adding a covered call strategy would give the opportunity to monetize the high volatility we’re seeing on the market now. It’s hard to say when the upside might come in US banks given all this uncertainty. But, there’s an argument to be made for someone who wants exposure to these US banks that a covered call strategy could make sense.

Struggles and risks in US banking today

The US banks’ stock market setbacks are due in part to a fear reaction from bank-specific failings at institutions like Silicon Valley Bank, but also reflect some structural headwinds for the sector.

The systemic issue comes down to deposit costs. As market-based interest rates rose sharply in 2022 and into 2023, the rates offered by banks to their depositors remained relatively low. Depositors, especially larger businesses, have begun to demand higher interest rates on their accounts, raising the cost of funding for many banks. Some of those depositors started transitioning some capital into other interest-bearing vehicles, such as money market mutual funds, which offered a higher interest rate as well. The whole banking sector is now facing some challenges to profitability growth due to the rising costs of deposits.

Those deposit costs can be more accurately described as a structural headwind, rather than an existential risk. While deposit costs contributed to the fall of Silicon Valley Bank, it’s notable that a range of company-specific factors played a role: Silicon Valley Bank’s high proportion of business clients, meaning its depositor base was concentrated and held high average account balances. When word spread across social media of venture capitalists sounding alarm bells to their investment companies, withdrawals cascaded. Continue Reading…

By Winnie Jiang, Vice President, Portfolio Manager, BMO ETFs

(Sponsor Content)

Little about the current economic cycle has conformed to historical norms. With divergence in employment data and leading economic indicators, recent data released sent mixed signals that left investors perplexed about the near-term economic outlook.

On one hand, the job market remains overwhelmingly strong, with ISM (Institute for Supply Management) Services bouncing back from extreme lows in December and retail sales also rebounding. The re-opening of the Chinese economy will likely provide a breather on global supply chain issues while boosting demand. Consumer credit remains well retained as default rates stay low with no warning signs of near-term upticks.

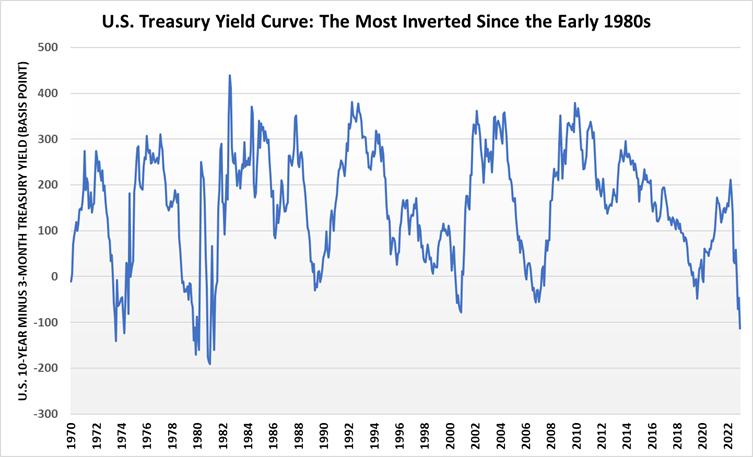

On the other hand, yield curve inversions, a precedent of most recessions, continue to worsen. 3-month U.S. Treasury yields are pushed above 10-year yields by the widest margin since the early 1980s. ISM Manufacturing PMI (purchasing managers’ index) and housing data also point to a gloomy outlook. Corporate sentiment and capital expenditure showed little signs of recovery, and housing permits have rolled back to pre-pandemic levels after surging strongly during Covid.

Source: Bloomberg, January 31st, 2023

The Outlook

While robust job markets and consumer data keep inflation well above the Fed’s long-term target, recent CPI (Consumer Price Index) announcements indicate things are steadily, albeit slowly, moving towards the right direction. The inversion of the yield curve caps the magnitude of further rate increases that could be absorbed by the economy before it slips into a recession.