Worried you’re behind the “Magic 8 Ball” when it comes to investing in retirement savings? If your retirement fund is a bit anemic (or nonexistent), there’s no time like the present to get started! It’s never too late to invest your money but do you know where to start? Will explore active, passive, and wise investment options in this quick guide to your financial freedom.

Adobe image courtesy Logical Position

By Dan Coconate

Special to Financial Independence Hub

Investing is often seen as a young person’s game. But the truth is, it’s never too late to start investing your money.

This is especially relevant for retirement planners and seniors. Whether you’re planning ahead or looking to make your savings work harder, investing can play a crucial role in your financial future. Below, we take a closer look at why you should start investing, what to look for when you invest, and how to prepare your family for the future with this wise financial decision.

Is it really never too late to Invest?

Many people think investing is only for the young. But countless success stories prove otherwise. Take Colonel Sanders, for example. He started Kentucky Fried Chicken (KFC) at the age of 65. Another prime example is Ray Kroc, who expanded McDonald’s in his 50s. These stories highlight that it’s possible to achieve financial success later in life, including when you think it’s time to retire.

Certain investments work for different age groups, which makes it easier for seniors to start investing. For instance, dividend-paying stocks offer a steady income. Bonds provide low-risk options suitable for conservative investors. Even real estate is a lucrative investment at any age.

Starting later can be just as rewarding as investing early. The key is finding the right opportunities. By doing so, you can make your money work for you, irrespective of your age and stage in life.

Active vs. Passive Investments

Active investments require regular attention. Examples include actively managed mutual funds and day trading. These investments aim to outperform the market. They need more effort but can offer higher returns.

Passive investments, on the other hand, are more hands off. Index funds and ETFs are good examples. These options track market indexes and require less management. They are ideal for those who prefer a simple approach.

Understanding the differences between active and passive investments is important. By knowing your options, you can choose the one that suits your lifestyle and risk tolerance. Whether you prefer to be hands-on or hands-off, there’s an investment strategy for you.

Benefits of Investing at a Later Stage

Investing later in life offers long-term financial security. It helps grow your money and secures enough funds for retirement. A well-planned investment can provide a steady income stream and offer peace of mind. Continue Reading…

Over the years of running this site, I have received numerous requests to share everything in my portfolio. For today’s post, I will reveal a bit more to help other DIY investors out since they are curious: what are my top-5 stocks?

Read on for this update including what has changed over the last year in this pillar post!

My Top-5 Stocks

As I approach 15 years as a DIY investor, a hybrid investor no less, we inch closer to our semi-retirement dream. Long-time subscribers will know we’ve always had two major financial goals to achieve as part of that journey:

2.Beyond two workplace pensions, beyond our future CPP or OAS benefits, beyond any future part-time work – another big goal was for us to own a $1 million dollar investment portfolio for retirement.

Well, we accomplished that as well a few years ago.

Our investing goals have been accomplished using a hybrid investing approach – something that might appeal to you as well:

Approach #1 – we own a number of Canadian dividend-paying stocks for income and growth. We have essentially unbundled a Canadian dividend ETF for income and growth – and built our own ETF – without any ongoing money management fees.

Approach #2 – we own a few low-cost ETFs that focus on growth. We believe it is wise to invest beyond Canada for growth/diversification and so we do via a few low-cost ETFs like XAW and QQQ in particular. Our U.S. stocks are down to a handful now and potentially less over time in favour of those ETFs above.

A bias to getting paid – my top-5 stocks

With a bias to getting paid and getting more raises over time as a shareholder, we own a few stocks in particular. Before sharing my top-5 stocks, some highlights why DIY investing works for me.

1. Fees are forever.

With investing you usually get what you don’t pay for.

Based on all the information available today, to buy an index fund in particular, I don’t believe you need a money manager to perform indexing work on your behalf. That decision is up to you of course.

2. I/we control the portfolio.

Ultimately nobody cares more about your money than you do.

I run my site to help pay forward my successes but also share what’s not working. I have no problems admitting I am not perfect. I make investing mistakes. Most people do. Via my site, I share those lessons learned so you don’t have to make them. While there is no perfect portfolio you can design a portfolio that should meet many of your needs over time. Many DIY investors, readers here, have learned that sustainable dividend and distribution income is one such path to financial independence. In some cases, these DIY investors have been investing long enough that their portfolio income now exceeds their expenses – some of them earning over $100,000 per year from their portfolio after decades of investing. They’ve learned that the power of compounding is an incredible force if left uninterrupted. These DIY investors manage their investments based on their income objectives.

I simply hope to follow the same formula. 🙂

Given I control our portfolio, I feel I can manage our investments aligned to our objectives. A reminder about my free e-book below:

Chapter 1: Spend less than you make and invest the difference. Invest in mostly low-cost products. Strongly consider diversifying your investments including stocks from different sectors and countries that pay dividends and offer growth.

Chapter 2: Avoid active trading. Celebrate falling stock prices – buy more when they fall in price.

Chapter 3: Disaster-proof your life with insurance, where needed, to cover a catastrophic loss. Otherwise, keep investing and just keep buying.

Book conclusion: Read Chapters #1-3 and rinse and repeat for the next 30 years. Retire wealthy.

That’s the basics within 80,000+ personal finance books in just four bullets. 🙂

As a DIY investor I believe you have some powerful decisions most money managers will never possess:

A money manager has to demonstrate value by trading. Otherwise, why use them when you can buy your own quality stocks or indexed funds instead?

Money managers usually need approval for their transactions. Instead, you can decide when to celebrate lower prices to get your stocks on sale without another manager, director or VP-scrutiny involved.

To paraphrase the index investing community, with no way to consistently identifying manager performance ahead of time, there is very little chance of finding any money manager who after fees charged to clients can consistently best a basic index fund performance over the long-haul.

There are simply too many low-cost, diversified, easy-to-own ETF choices to build wealth with. As a DIY investor, you don’t ever have to pay someone else to do your work for you.

In the spirit of going it alone, doing it yourself and being accountable for your own results, I feel my hybrid approach offers the best of both worlds:

In Canada, we own many of the top-listed stocks in the TSX 60 index for income and growth.

Beyond Canada, beyond a few U.S. stocks, we use indexed ETFs for extra diversification.

We fired our money manager years ago and have never looked back … that approach might work for you too.

Without further delay, here are our top-5 stocks in our portfolio by portfolio weight current to the time of this post.

My Top-5 Stocks

1. Royal Bank (RY)

Since publishing the original post in fall of 2023, I can share that Royal Bank of Canada (RY) remains our largest single stock holding. About 4-5% of the total portfolio. We’ve owned RY for many years – profiled here.

Here are the returns compared to one of my favourite low-cost ETFs (XIU) for comparison:

All images/sources with thanks to Portfolio Visualizer.

2. TD Bank (TD)

While the management team at TD is certainly due for some changes, I will disclose that TD is our second largest stock position at the time of this post. Like RY, we’ve owned TD for many years – profiled here – as early as 2009.

Again, returns for comparison purposes:

3. Fortis (FTS)

Banking is just one important sector in our Canadian economy. Fortis owns and operates multiple transmission and distribution subsidiaries in Canada and the United States, serving a few million electricity and gas customers.

Last time I checked, just like people need to bank or borrow money (see the desire for us to own banks!) folks love electricity and power.

I own Fortis for steady dividend income and some capital gains. I started my ownership in Fortis also back in 2009. You can read about that here.

Again, historical returns for context:

4. Telus (T)

Our Canadian stock market operates in an oligopoly, meaning there are a few dominant players controlling the market. We see this in banking, utilities, and it continues with our telco industry. As a shareholder, Telus has been focused on expansion in recent years but in doing so has also taken on some debt in the process. The share price has lagged. With interest rates due to come down further over the coming 24 months, I believe Telus is a great buy to add more to my portfolio.

Move over Bell Canada, Enbridge, Bank of Montreal, Emera and other stocks competing for the top-5 position: Canadian Natural Resources (CNQ) is now firmly in the top-5 as of summer 2024.

Following the stock split and rise in share price, CNQ continues to be a stock on the rise in my portfolio.

Before we dive into this article, let’s play a quick game: a word association game. I’ll bet you a crisp $5 bill, or a shiny loonie for the more risk averse out there, that with three chances, I can guess the first word that pops into your head. Now, it has to be the first word, so no cheating. Ready, set… the word is ‘Retirement.’

If you said ‘Retirement Income,’ ‘Retirement Savings’ or ‘Retirement Home,’ I’ll come to collect my winnings. If you said anything like ‘Travel,’ ‘Hobbies’ or ‘Exploration, then good on you; I’ll send along an IOU.

The reason I felt so confident taking that bet is because when I tell people that I work in retirement planning, 99 out of 100 times, they assume that I work in financial services. The other time, people ask about senior living. Retirement has become so synonymous with financial planning, and so associated with ‘old age,’ that they’re practically inseparable. Yet, in reality, retirement is a stage of life, not a date on the calendar, an amount in your bank account, and is certainly not a death sentence. One of our primary goals when creating our startup, RetireMint, was to reframe the national conversation around “what it means to retire,” which, at its core, requires redefining how Canadians prepare for retirement.

Now, I am not discounting the importance and necessity of a sound financial plan. After all, you are reading this in Financial Independence Hub … Yes, financial planning is the keystone of retirement preparation, as you won’t even be able to flirt with the idea of retiring without it. Yet, retirement planning must adopt a much wider definition and break free from the tethered association of solely financial planning.

Retirement should really be a time to enjoy the fruits of your hard labour: a chapter that will hopefully span decades, fuelled by leisure, exploration, discovery and meaning.

Answering the ‘what, where and how’ of everything you want to see, do and accomplish in this next chapter requires conscious preparation in areas far beyond spreadsheets and bank statements.

The industry paradigm is that you have about 8,000 days in retirement, or around 22 years. In each of those years, you will have more than 2,000 hours of new-found free time that would have been spent working throughout the majority of your life. Filling these thousands of hours with meaningful and purposeful activity is much more easily said than done.

The common approach to retirement planning (yes, we are now using the wider definition) has been to ‘punt the ball down the field’ and ‘cross that bridge when you get to it.’ Yet, we see time and time again that those who leave their lifestyle planning to their first day of retirement are the ones who have the hardest time transitioning into this next chapter.

The people who say, “I’ll never get tired of sipping Piña Coladas on a beach,” face the same fate as the ones who say “I can’t wait to golf every day.” While these may be dream activities for retirees, they ultimately see diminishing returns if they’re your only activities, because humans are funny creatures: we need meaning and variation.

Despite its innocent demeanour, retirement has some dark, inconvenient truths:

Ages 50-64, 65-84 and 85+ have the three highest suicide rates in North America, and in the last five years, we’ve seen a 38% increase in suicides among Baby Boomers.

Canadians over 65 have a divorce rate three times the national average.

Over 25% of older Canadians are socially isolated, which causes a 50% increased risk of dementia.

And, 77% of older Canadians live with at least two chronic illnesses or conditions.

It’s statistics like these that starkly highlight the importance of planning for your lifestyle, wellness and purpose, as well as the need for trusted resources to help with this planning. This was the a-ha moment that sparked our urgency to develop RetireMint.

RetireMint stemmed from empirical evidence showing that once people’s finances are at least on the right track, their primary concerns and conversations with their financial advisors shift far beyond the scope of their meetings. “What am I going to do with the grandkids?,” “Where am I going to travel?” “What happens when I lose my work insurance coverage?,” are just a few of the plethora of questions that popped up time and time again.

It’s fantastic that Canadians have this level of trust and comfort with their advisors, but the truth is that financial advisors are not equipped to answer all of these broader retirement inquiries, and they’ll be the first to admit it. It’s clear that this undue burden falls on the shoulders of financial professionals, but if not for them, who is going to provide the answers? Continue Reading…

As an engineer by education & training and an analytical person, it shouldn’t come as a surprise to readers that I ponder a lot. I like to think about something carefully before deciding or reaching a conclusion. Although this approach may not work in all situations, I enjoy being analytical on major life decisions.

The other day I woke up with this interesting idea in my head. The idea simply wouldn’t escape from my head and I ended up thinking about it for the entire day.

The interesting idea is simple: Should we go all in on QQQ with our RRSPs?

Since this is an interesting idea, I thought I’d turn it into a blog post, analyze the idea thoroughly, and hopefully come to a conclusion.

Things to consider

A few things before we dive into the analysis.

An RRSP is a tax-deferred account. When you contribute to one, you get a tax deduction for 100% of your contributions. If you contribute $10,000 to your RRSP, it will reduce your net income by $10,000, and potentially bring you down to the lower tax bracket.

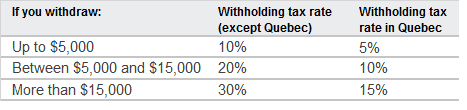

When you withdraw money from your RRSP, you will be subject to withholding tax. The amount of withholding tax is based on how much you take out.

The net amount after the RRSP withholding tax is then taxed at your marginal tax rate.

You also must convert an RRSP to a retirement income option such as a RRIF by the end of the year that you turn 71. Although there are no mandatory withdrawal requirements in the year you set up your RRIF, you must start withdrawing money the year after setting up your RRIF (effectively at age 72). Furthermore, there’s a minimum withdrawal rate for RRIF. The withdrawal rate increases as you age.

Note: You can convert your RRSP before age 71. If you do, there’s a minimum withdrawal rate starting at age 55.

Just like the RRSP, money withdrawn from an RRIF is taxed like working income, or at 100% of your marginal tax rate.

In other words, it doesn’t matter whether the money is from capital gains or dividend income, money withdrawn from an RRSP and an RRIF is taxed at 100% of your marginal tax rate. You don’t get any preferential dividend tax treatment like in non-registered accounts.

When we do start living off our investments (aka live off dividends), our withdrawal strategy is very similar to Mark from My Own Advisor – NRT. This means drawing down some non-registered (N) assets along with registered assets (R), leaving TFSAs (T) for as long as possible.

More details:

N – Non-registered accounts – we most likely will work part-time to keep ourselves engaged and live off dividends to some degree from our non-registered accounts. The preferential dividend tax credits will come in handy.

R – Registered accounts (RRSPs) – we plan to make some early withdrawals from our RRSPs slowly. We may collapse our RRSPs entirely before age 71. We may also convert our RRSPs to RRIFs. This is not entirely decided (if we do convert to RRIFs, we want to make sure the dollar amount is relatively small). Early withdrawals will help us from having a large amount of money in our RRSPs and having a big tax hit when we start withdrawing. In other words, this will help smooth out our taxes.

T – TFSAs – since any withdrawals from TFSAs are tax-free, we intend not to touch our TFSAs for as long as possible so they can compound over time.

Note: if you’re interested in this retirement projections service, mention TAWCAN10 to Mark and Joe to get a 10% discount.

We may also do an RNT (Registered, Non-Registered, then TFSA) withdrawal strategy but will need to crunch some numbers. Whether it’s NRT or RNT, the important part is that we plan to slowly withdraw money from our RRSPs.

Current RRSP Holdings

Although RRSPs are best for holding U.S. dividend stocks to avoid the 15% withholding tax, we hold U.S. and Canadian dividend stocks and ETFs inside our RRSPs.

At the time of writing, we hold the following stocks and ETFs inside our RRSPs:

Our RRSPs consist of 18 U.S. dividend stocks, 10 Canadian dividend stocks, and 2 index ETFs.

In terms of dollar value, my RRSP makes up about 70% while Mrs. T’s RRSP (spousal RRSP) makes up about 30%. Ideally, it would be great if our RRSP breakdown were 50-50 (I’m ignoring my work’s RRSP so in reality the composition is more like a 25-75 split).

Because we started Mrs. T’s RRSP a few years later than mine it hasn’t had as much time to compound. Furthermore, I converted over $120,000 worth of CAD to USD in my RRSP when CAD was above parity. Over time, this gave my self-directed RRSP an automatic 30% performance boost.

In addition, because the exchange rate hasn’t been as attractive, the only U.S. holdings Mrs. T has are Apple and QQQ. The rest of her RRSPs are all in Canadian dividend stocks.

We purchased QQQ earlier this year inside Mrs. T’s RRSP. Dollar-wise, it makes up a very small percentage of our combined RRSPs.

Some info on QQQ

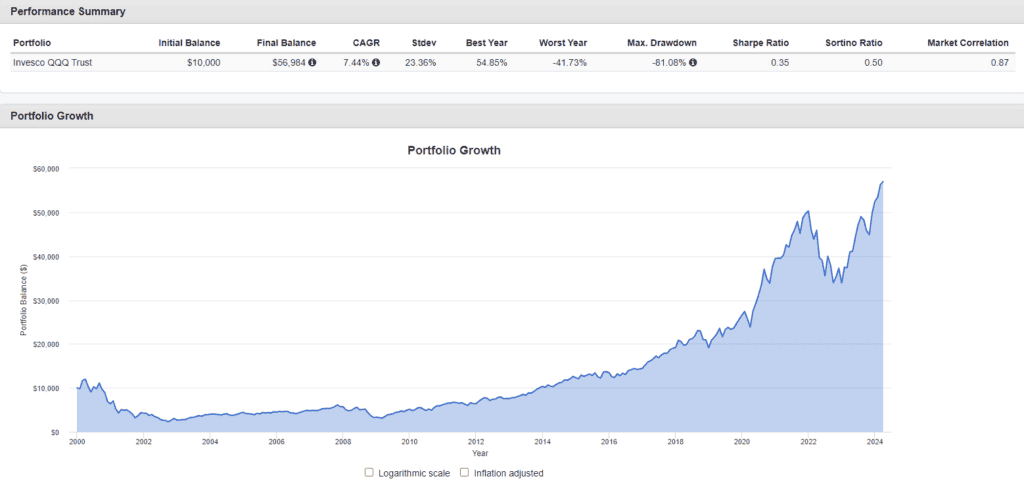

For those readers who aren’t familiar with QQQ, it’s an ETF from Invesco. Since launching in 1999, the ETF has demonstrated a history of outperformance compared to the S&P 500.

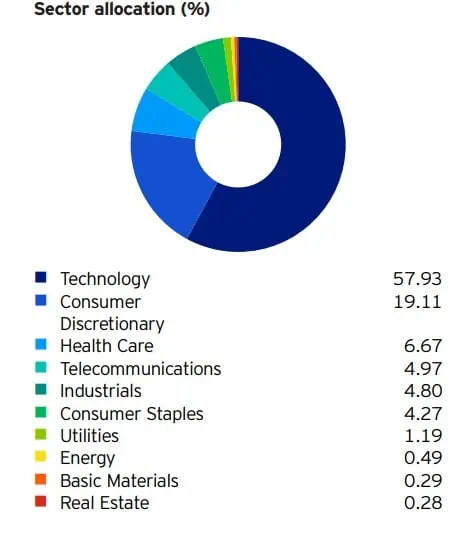

QQQ tracks the Nasdaq 100 Index. The fund is rebalanced quarterly and reconstituted annually. At the time of writing, QQQ holds 101 stocks with the top 10 holdings being Microsoft, Apple, Nvidia, Amazon, Meta, Broadcom, Alphabet Class A & C, Tesla, and Costco. The top 10 holdings make up 47.01% of the fund.

The top 11 – 20 holdings for QQQ are AMD, Netflix, PepsiCo, Adobe, Linde, Cisco, Qualcomm, T-Mobile US, Intuit, and Applied Materials. These holdings make up 15.71% of QQQ.

Due to the nature of the Nasdaq 100 Index, QQQ is heavily exposed to technology and consumer discretionary sectors.

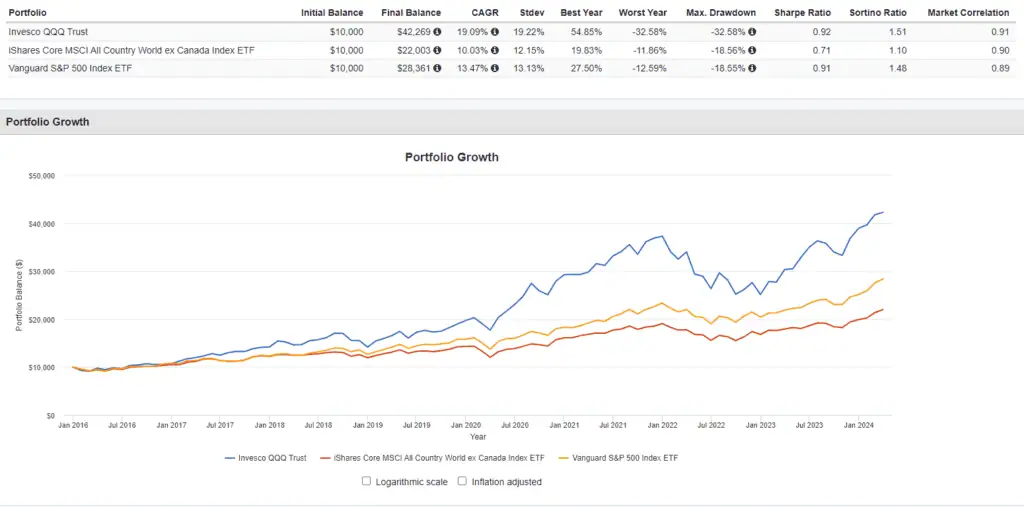

As you can see from below, it also outperformed XAW and VFV significantly. This is the key attraction of QQQ, as the fund has historically outperformed many major indices.

Source: Portfolio Visualizer

As you can see from above, $10,000 invested in QQQ in 2016 would result in over $42,000 in 2024 whereas the same amount invested in XAW and VFV would result in less than $30,000.

Case for going all-in on QQQ

Why would we consider going all in on QQQ?

Because QQQ has done very well historically compared to the major U.S. and Canadian indices.

Per the chart above, QQQ had an annualized return of 19.09% since 2016. In the last 20 years, QQQ has had an annualized return of 14.03% and an annualized return of 18.12% in the last 10 years.

Assuming we invest $150,000 in QQQ and enjoy an annualized return of 15% for the next 10 years, we’d end up with $606,833.66, assuming no additional contributions. On the flip side, if we have the same money and have an annualized return of 10% (long-term stock return), we’d end up with $389,061.37. This means investing in QQQ would result in more than $217.7k of difference in return on capital or 56%. This is a pretty significant difference.

Yes, historical returns don’t guarantee future returns. However, the high exposure to technology stocks should allow QQQ to continue the superior return for years to come.

Due to the fact that RRSP and RRIF withdrawals are taxed 100% at our marginal tax rate, it makes sense to attempt to maximize the total return inside of RRSPs/RRIFs instead of a mix of dividend income and capital return.

Case against going all in on QQQ

The biggest case against going all in on QQQ? Our dividend income would take a big hit.

Our RRSPs contribute about 30% of our annual dividend income. With our 2024 target of $55,000, selling everything in our RRSPs and holding QQQ only would reduce our total dividend income to about $38,500 (ignoring QQQ distributions completely).

But focusing on dividend income alone is a bit silly when we should be considering total return and the total portfolio value.

Out of the 18 U.S. stocks that we hold in our RRPS, QQQ holds 9 of them already. The stocks that QQQ doesn’t hold are:

Abby

Johnson & Johnson

Coca-Cola

McDonald’s

Procter & Gamble

Target

Visa

Waste Management

Walmart

These 9 stocks make up about 25% of our RRSP in terms of dollar value. Since we purchased these stocks many years ago, they have all done very well, with a few of them being multi-baggers. I would hate to sell the likes of Visa and Waste Management.

Investing in QQQ does mean that when we start to live off our investment portfolio, rather than withdrawing mostly from dividends inside our RRSPs in the first few years (to increase our margin of safety), we’d need to sell QQQ shares and touch our principal.

If there are a few years of poor returns at the beginning of our retirement, this could cause a significant reduction in our portfolio value. Essentially, selling shares may not have as much margin of safety compared to relying on withdrawing dividends only.

Another case against going all in on QQQ is that QQQ is currently highly concentrated in technology stocks so it’s not all that diversified compared to other index ETFs like XAW. The latest AI hype has significantly bumped up the share price of many technology stocks. Would we see a Dot Com type of bubble in the future and hamper the return of QQQ? That’s certainly possible.

QQQ historical return

As you can see from the chart above, QQQ didn’t recover from the Dot Com bubble for about 14 years. This is a risk we would take on if we were to go all in on QQQ.

Potential Alternatives to going all-in on QQQ

Instead of going all in on QQQ, there are some potential alternatives.

First, we can simply add more QQQ shares in the next few years to have QQQ make up a larger percentage of our dividend portfolio. This is already our plan of record but we stay focused on this goal instead of purchasing more dividend paying stocks in our RRSPs.

Second, since we hold QQQ inside of Mrs. T’s RRSP and she holds mostly Canadian dividend stocks in her RRSP, we can consider closing out these positions and using the money to buy QQQ shares.

If we were to do that, we’d only lose about 12% of our forward annual dividend income, going from $55,000 to $48,400. Assuming QQQ continues the superior performance over other indices, holding only QQQ and Apple in Mrs. T’s RRSP and continuing to contribute to her RRSP only may mean that we have a higher chance of ending up with a 50-50 RRSP split down the road.

Some additional logistics to consider

The second option mentioned above is quite intriguing. But there are some logistics to consider if we were to forward with this option.

The first thing to consider is that we’d need to sell all 9 stock holdings in Mrs. T’s RRSP. At $4.95 per trade at Questrade, this would cost us $44.55. Not a significant amount of money but it would be cheaper if we were to transfer her RRSP to Wealthsimple.

Second, we’d need to convert CAD to USD and take a hit on the exchange rate. Utilizing Norbert’s Gambit would allow us to save on the additional current exchange fees. The alternative solution would be to journal as many of the holdings to the U.S. exchange, close the positions, and end up with USD.

Another option is to consider the Canadian equivalents, like XQQ, ZQQ, HXQ, or ZNQ to avoid currency conversion. As many of you know, I’m all for simplicity and straightforwardness, so it makes sense to hold the original ETF QQQ instead of other alternatives.

Conclusion – Should we go all in on QQQ?

So, have I reached a decision after all the considerations?

I’ll admit, the second option mentioned (holding only QQQ in Mrs. T’s RRSP) is very intriguing to me. But I am going to sleep on it for a bit and discuss the idea with Mrs. T before making any major decisions. In the meantime, we will continue to add more QQQ shares in Mrs. T’s RRSP so QQQ makes up a bigger percentage of our dividend portfolio.

Readers, what would you do? Would you go all in on QQQ?

Hi there, I’m Bob from Vancouver, Canada. My wife & I started dividend investing in 2011 with the dream of living off dividends in our 40’s. Today our portfolio generates over $2,700 in dividends per month. This post originally appeared on Tawcan on July 15, 2024 and is republished on the Hub with the permission of Bob Lai.

So you have been reading Million Dollar Journey (MDJ) for years, have used your Canadian online broker account to DIY-invest your way to a solid nest egg.

You’ve got a TFSA, and RRSP, and maybe even a non-registered account – full of good revenue-generating assets.

Kudos!

Now comes the tough part: How do you turn that nest egg into a usable stream of money that you can spend as you enter retirement?

Surprisingly, when it comes to discussing Canadian safe retirement withdrawal rates, and talking to folks who have retired at all ages, spending their retirement savings represented a massive mental strain for them. I guess (as someone who has never retired or sold investments to pay for retirement) that I always thought that saving for retirement would be the hard part.

Isn’t spending supposed to be more fun than squirreling away?

It turns out that once you get into that savings mindset, it can be hard to flip the switch back to enjoying spending the fruits of your labour. This is especially true for folks who are looking at strategies for an early retirement because they are much more likely to have been super-aggressive savers during their time in the workforce.

I didn’t go into the topic of safe withdrawal rates for retirement expecting the topic to be so deep and full of variables! Afterall, the concept seems simple enough right?

How much can I take out of my investment portfolio each year, if I need that nest egg to last for 30, 35, 40, or even 50 years?

Ok, so let’s maybe start with the rule of thumb that advisors have used when looking at retirement drawdown plans for a while now.

Back in 1994 a financial advisor named William Bengen looked at the last 80 or so years of markets and retirement, did a bunch of math, and arrived at a concept we now call “The 4% rule.”

The basic idea of the 4% retirement withdrawal plan is that someone could safely withdraw 4% of their investment/savings portfolio each year and – assuming a 60/40 or 50/50 split of bonds/stocks in their portfolio – they would never run out of money. This idea of withdrawing a certain percentage of your portfolio to fund your retirement is called the Safe Withdrawal Rate (SWR). The math behind this magic 4% figure means that if you have the nice round $1 Million investment portfolio that we all dream of, you could safely pull out $40,000 the first year, and then adjust for inflation and withdraw 4% plus inflation after that. (So if there was 2% inflation between year one and year two, you could now withdraw $40,800.)

Bengen, and another highly influential study took their rule and retroactively applied it to retirees from every single year from 1926 to 1994. They found that nearly 100% of the time (depending on what was in the investment portfolio) people could retire, and withdraw 4% of their portfolio for 30 years of retirement – and not run out of money. In fact, a large percentage of the time, if retirees followed the 4% rule, they not only didn’t run out of money, they finished life with more money than when they started retirement!

Keep in mind, these authors didn’t worry about OAS or CPP, or a workplace pension, or even the tax implications of different types of withdrawals. They were simply trying to come up with a useful rule of thumb for how much a person could safely withdraw from their retirement portfolio.

What the 4% Rule means for your Magic Retirement Portfolio Number

If you can safely withdraw 4% of your portfolio to fund your retirement, then the simple math tells us that if you can accumulate 25x your annual retirement budget, you no longer have to work.

Here’s the breakdown:

Jane looks at her budget and realizes that once she retires she will have a lot less spending demands. She carefully weighs the numbers and believes she’ll need $40,000 per year to quit her 9-to-5.

Consequently, Jane needs the magical “4% of her portfolio” to equal $40,000 per year.

For a 4% withdrawal to equal $40,000, Jane will need a $1,000,000 portfolio.

If Jane reassess and realizes she needs $60,000 per year in retirement, Jane would need 25 times $60,000 (because 4% goes into 100% twenty-five times) which is $1.5 Million.

Jane might not need anywhere close to $1.5M if she intends to do a little part-time work in retirement, and is willing to use some math + research strategies to help herself out a bit when it comes to managing her nest egg! But more on that later…

4% Safe Withdrawal Rate: Potential Problems

Up until the 4% rule became a thing, when financial advisors were asked about safe withdrawal rates, the only thing they could really say is, “it depends.”

This was followed by a whole lot of graphs, math, and other boring stuff that no one really understood, but didn’t want to admit to not understanding.

The 4% rule of thumb was a BIG deal when it came to financial planning. It provided the best answer yet to the millions of retirees who desperately wanted an answer to the question:

“How much money can I take out of this portfolio each year without going broke and eating cat food as an 80-year-old?!!!

Before we get into discussing the nitty gritty of safe withdrawal rates today, we must understand the limitations of the 4% rule. Here are the major rules that I came across after reading for roughly a hundred hours. The research I read was mostly done by people who have dedicated a major part of their life’s work to studying retirement and spending patterns across the globe. As far as I can tell, they are our best hope for trying to define just what the range of outcomes will be for various types of retirement spending + investing plans. The two major experts that I relied on most were Wade D. Pfau and Michael Kitces, with major assists to the writers behind Early Retirement Now, The Mad Fientist, and Millennial Revolution.

1) There is no way to know the future returns for any asset class. We’ll get into this more later on in the show, but basically, the vast majority of the math that these folks are basing their withdrawal rates on is underpinned by a US stock market that has done incredibly well over the last 100+ years. A few other stock markets of developed countries have done as well (Yay Canada!), but the majority of stock markets DO NOT return 10%+ over the long haul.

It turns out that when you don’t know how much money your nest egg will be generating, solving for how much money to take out becomes kind of hard to answer!

2) These withdrawal plans were mostly created with a 30-year retirement time horizon in mind. When most people were retiring at 60 or 65, and living to 75-80, a 30-year window looked like a pretty safe horizon for most people. If this still describes your plan, a 30-year horizon is probably still a pretty safe rule of thumb. If you’re looking at leaving your job at 40-50 years of age (or even earlier) and living well into your 90s, you could easily be looking at a retirement that lasts 50+ years! (Which is pretty cool to think about, really!)

3) The 4% rule doesn’t reflect how many Canadians actually invest and pay for investment advice. In a perfect world, we would all handle our own withdrawal plan and DIY our portfolio allocations and withdrawals. But many of us aren’t interested in diving into the deep end of handling our own assets. Consequently, we have to take those pesky investment-related fees into account when looking at our safe withdrawal plans. If you’re paying 2% of your returns to a mutual fund salesperson each year, you will need a lot more than $1 Million to safely withdraw 4% each year.

4) The 4% rule doesn’t take into account adjustment in behaviour. For example, Jane might take on a little part-time work to make $10,000 per year if she sees her account balance going down too fast. Or she may decide to move somewhere that has much lower living costs. A blanket rule that tries to predict 30 years into the future can’t possibly allow for all of these variables.

5) There is no OAS and/or CPP taken into consideration when looking at the 4% rule. It’s also likely that Jane might not have considered how taxes might affect how much she needs to withdraw each year.

6) The 4% rule tries to address what us finance geeks call Sequence of Return Risk – but it gets really hard to do so after you go beyond the 30-year mark of retirement. More on this below.

So, now that we know what the rules of thumb are for safe withdrawal rates that the professors of all things money have come up with, as well as some of the limitations of those rules of thumb, let’s take a look at what this might mean when applied to your retirement!

How has the 4% Rule Done in the Past

Given all of these variables that the 4% rule doesn’t account for, you might be wondering just why it is so widely used.

The truth is that I put all that naysayer stuff first because folks love to poke holes in financial theories. (For good reason, we’re talking about people’s life plans here.) Let’s look at just why the 4% rule has become the rule of thumb.

As always when discussing financial planning and financial projects, one must understand that while looking at past results in the stock and bond markets is one of the best tools we have, it does not guarantee future results!

Drawing on what I’ve read from Bengen, the Trinity Study, and recent authors such as Pfau and Kitces, here’s some summary notes on just how the 4% rule would have worked in the past in the USA market. (The Canadian market has actually done slightly better most of the time, so the conclusions would be quite similar when looking at past Canadian returns.)

1) When you apply the original 4% withdrawal philosophy, not only does your money never run out over any 30-year period over the last 100 years – But 95% of the time the retiree would have finished with MORE THAN THEY STARTED WITH!

I know this sounds crazy, but companies have made a lot of money the last 100 years. If you owned a piece of them, you’ve done pretty well!

2) More than half of the time, the retiree who stuck to the 4% rule would have DOUBLED THEIR MONEY at the end of the 30-year time frame.

What this means, is that in the past, it is far more likely that retirees could have spent substantially more than that 4% withdrawal safety number, than it was that they would ever run out of money.

3) Rather than use Bengen’s 60/40 portfolio, you can actually increase your chances of favourable outcomes by skewing your portfolio to take on more stocks. Of course, your portfolio will also be likely to cause a bit more heartburn as you watch stocks gyrate up and down over the years.

4) Even folks who retired during the rough decade of the 2000s are doing just fine.

If I Want to Retire Early or do this whole “FIRE” Thing – Does the 4% Work for Me?

The short answer is: Probably Not

When you start to take rules that were created for a 30-year safe withdrawal period, and stretch them out over 50+ years, it makes sense that the rules of thumb don’t really work anymore.

Taking money out of your nest egg for that long means that you’re more likely to encounter a long-term period of rough markets, and have your money run out.

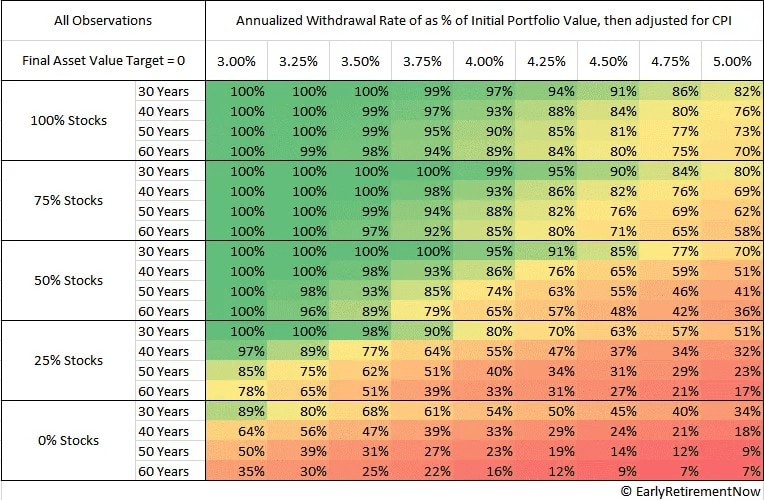

The website Early Retirement Now (created by folks who are fluent in high-level economics math and Monte Carlo simulations) have created the following chart and conclusions when it comes to safe withdrawal rates and long retirement periods.

I’ve checked their assumptions with a ton of really smart people that I trust, as well as doing the math myself, and if you assume the same returns that we’ve had the past 100 years or so in North America, I can’t find anything to argue with!

1) The 30-year 4% rule still works pretty well, and a 5% withdrawal rate is only fit for the very adventurous or flexible-minded out there!

2) Tilting your portfolio towards stocks over bonds increases your chances of the best outcomes – assuming that you don’t panic when markets go down and sell at the worst times.

3) At high stock allocations, the 4% rule still worked pretty darn well for a 50- or 60-year retirement! (With past returns that is.) Continue Reading…