With so many Canadians plugged into the latest Trump Tariff news, I felt that I needed to get an updated trade war column out as soon as possible!

So what I’m going to do today is update an article I wrote back when we were taking our first baby steps into Trump Tariff reality. Below you’ll see a ton of info on what tariffs are, what Canada’s situation is in regards to the big picture effect on our economy, and finally, what the impact is likely to be on your portfolio.

But first, just to bring you up to speed, here’s what the President announced in his big “Liberation Day” speech – complete with grade-five-science-fair-style cardboard visual aid.

A baseline tariff of 10% will be imposed on nearly all imported goods from all countries. This tariff is set to take effect on April 5, 2025

Canada and Mexico will not – for the moment – be part of that 10% baseline tariff.

Canada and Mexico trade is basically now broken up into three categories: goods that are USMCA-compliant, goods that are not UMSCA-compliant, and goods that are in sectors that Trump wants special rules for.

USMCA-compliant goods are actually in the best spot of any imported goods in the world right now – as they get to enter the USA tariff-free!

Goods that are not UMSCA compliant are still under the 25% “Fentanyl Tariff” rules.

We already knew about potash and fossil fuels having their own 10% tariff rules, but it appears that lumber, steel, and aluminium will continue to have their own special place on the Trump Tariff list as well.

Likely the biggest Canada-related news was that the 25% tariff on automobiles will be applied to Canadian-made vehicles (despite the USMCA explicitly outlining this as being illegal).

In regards to the rest of the world, the most noteworthy developments were:

An additional 34% tariff on China, resulting in a total tariff of 54% when combined with existing duties.

European Union: A 20% tariff.

Japan and South Korea: 25% and 24% tariff respectively.

India: 26% tariff.

Vietnam: 46% tariff.

Many many many other tariffs.

As we hit publish on this article, countries around the world were announcing retaliatory tariffs and US stock market futures were showing that the overall US stock market was set to lose 4% as it opened on April 3rd.

The best quote that I heard in regards to summing up this whole mess was from Flavio Volpe, president of the Automotive Parts Manufacturers’ Association who stated that the new tariff situation was “like dodging a bullet into the path of a tank.” He went on to write, “The. Auto. Tariff. Package. Will. Shut. Down. The. Auto. Sector. In. The. USA. And. In. Canada,” and then, “Don’t be distracted. 25% tariffs are 4 times the 6/7% profit margins of all the companies. Math, not art.”

It appears that the rest of the world is finally waking up to the same reality that Canada and Mexico have been experiencing for the last two months. There’s much more that could be written about the gnashing of teeth and simply incredible quotes from the President such as, “An old-fashioned term that we use, groceries. I used it on the campaign. It’s such an old-fashioned term, but a beautiful term: groceries. It sort of says a bag with different things in it.”

Oooook.

For now, take a deep breath and read what I had to say a month ago in regards to your stock portfolio. The reality was true then, and it’s true today. In my predictions column back in late December I wrote:

“One of the most pressing questions for Canadian businesses in 2025 is whether the newly elected U.S. president will follow through on his promises of large tariffs on Canadian imports.

Trump’s fixation on trade deficits could lead to a significant shake-up in the global economy. He appears intent on generating tariff income to support the legislative groundwork for corporate tax cuts. His “national security” justification may lack substance, but it could still trigger sweeping trade policies.

I don’t actually believe that Mr. Trump understands how trade wars actually work, and he hasn’t cared to learn anything new in several decades. So the hopes better angels will talk him out of this are perhaps misplaced.

I believe even more strongly that the President-elect doesn’t understand how trade balances work, and consequently, he does not understand that in buying goods from Canada with a strong US Dollar, his constituents (US consumers) are winning! There is no “subsidization” of Canadian business going on here.

While a blanket 25% tariff on all Canadian goods seems unlikely, a more targeted 10-15% tariff on non-energy products feels probable. If that happens, Canadian businesses would face a challenging environment, and retaliatory tariffs from Canada could escalate tensions further.

My guess is that we’ll see some major disruption in Canadian manufacturing, with supply chains snarled, and some factory commitments being delayed indefinitely as companies decide to move more operations within the USA for the next few years at the very least. I’d also be pretty worried if I was a farmer and/or worked in the dairy industry. Some of these tariffs might come off when the overall North American trade deal is finalized.”

I’d say that held up pretty well!

The key here is definitely not to panic. The Canadian stock market has actually held up pretty well so far – and as always, it’s key to remember that the vast majority of the companies in Canada’s stock market DO NOT depend on selling specific goods to the USA. It’s also worth noting that a lot of companies that weren’t previously UMSCA-compliant are likely to become so in a hurry. If that happens, there might actually be a lot of Canadian companies in an enviable position relative to the rest of their global competitors as they will have no tariff to worry about (for now) versus 10%-50%+ for other countries.

This isn’t going to be good for any of the world’s economies, but the Trump Tariffs are already proving very unpopular with US Citizens and even among Republican politicians. Read on for more detailed reasoning on why you don’t need to do anything drastic in the face of these latest Trump tariff developments, and the broader US – Canada Trade War that has now expanded to include the rest of the world.

Trump (Delayed) Tariff Details

So – what is a tariff anyway?

A tariff is a tax by a government on foreign goods coming into a country. The import company (or person) pays the tax to the US federal government. In the vast majority of cases, the company then turns around and sells the imported product for a higher price (and possibly also takes a hit to their profit margin).

Trump’s tariff summary:

A 25% tax on all imports – aside from oil. This happens on Tuesday, February 5th.

A 10% tax on oil. This is supposed to kick in on February 18th.

Mexico will see a 25% tax on all of its imports.

China will get a comparatively light 10% tariff on its imports.

Canada will respond with two-phases of tariffs in response. They will total $155 billion of US goods.

Mexico hasn’t finalized details but announced tariffs ranging from 5% to 20% on US imports including pork, cheese, fresh produce, manufactured steel and aluminum.

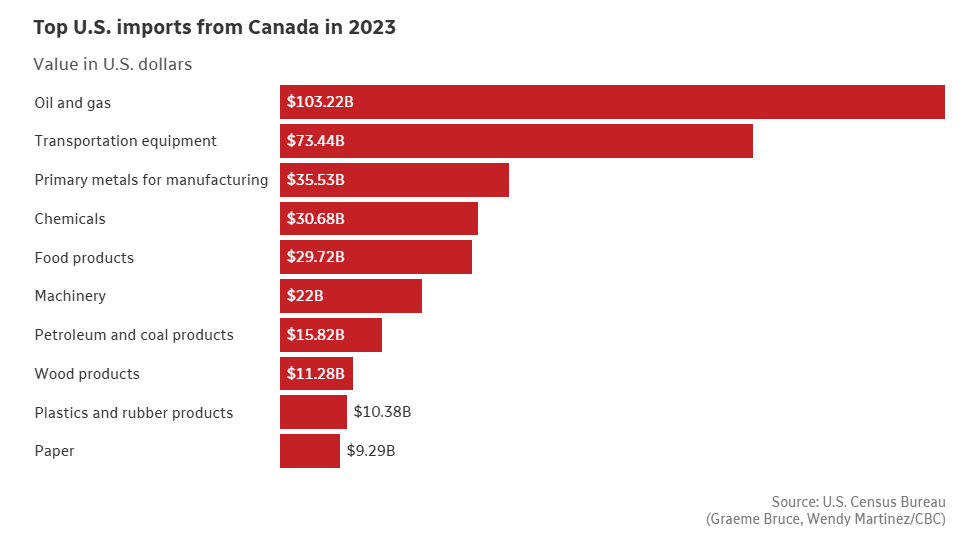

If you’re wondering what we send to the USA – it’s a lot (we don’t have 2024 numbers finalized yet).

The potential fallout from U.S. tariffs looms large. If the worst-case scenario unfolds and these tariffs stay on Canadian companies for more than a month or two, economists estimate it could push Canada into a three-year recession, shave three percentage points off our GDP, and wipe out 1.5 million jobs. While forecasts vary, one thing is clear – the economic risks are significant. It would likely be even worse for Mexico.

The USA isn’t going to get off the hook easily either. Predictions range between their GDP shrinking .3% to 1%. That range doesn’t give a precise picture of the fact that counter-tariffs will be heavily targeted with the goal of inflicting maximum pain to companies that are important to Republicans’ electoral chances. I wouldn’t want to be in the US alcohol or consumer goods business right now.

American consumers are going to immediately see higher prices on agricultural goods, lumber (which means more expensive houses), gasoline (especially in the midwest), and vehicles.

When it comes to cars, the idea that the tariffs will somehow shutdown Canadian factories and move them to the USA overnight is ridiculous. What will happen is that the complex supply chains involved for North American manufacturers will get much more expensive, and consequently it will make the final product more expensive. Continue Reading…

Here’s how an equally weighted portfolio of healthcare, utility, and consumer staples ETFs could provide better downside protection and reduce volatility.

Image courtesy BMO ETFs/Getty Images

By Erin Allen, Director, Online Distribution, BMO ETFs

(Sponsor Blog)

The U.S. stock market, particularly the S&P 500 index, isn’t as uniform as it might seem. While you may think of it as a homogenous entity, it’s far from reality.

The S&P 500 can be broken down into 11 Global Industry Classification System (GICS) sectors: information technology, health care, financials, consumer discretionary, communication services, industrials, consumer staples, energy, utilities, real estate, and materials.

Each sector groups together companies that operate in the same industry and offer similar products and services. Historically, different sectors have also shown varying levels of sensitivity to market and economic conditions.

Some are cyclical, meaning they typically do well during economic expansions but struggle in downturns. On the other hand, some sectors are considered defensive, as their revenues and earnings remain stable regardless of economic cycles.

One well-known investment strategy that takes advantage of these differences is sector rotation, where investors shift their money between sectors based on macroeconomic indicators like GDP growth, interest rates, and inflation.

Source:SPDR Americas Research. ++/– indicates the best/worst two performing sectors. +/- indicates the third best/worst performing sectors. The Energy sector did not make the top/bottom three sectors during any cycles, as it is less sensitive to U.S. economic cycles but more driven by global supply and demand of crude oil. For illustrative purposes only. 1

However, for risk-conscious investors, another approach involves overweighting defensive sectors — particularly health care, utilities, and consumer staples — to provide better downside protection and reduce portfolio volatility.

What makes a sector defensive?

A sector is considered defensive when its companies provide goods or services that consumers continue to purchase regardless of economic conditions.2

For example, when the economy weakens, a consumer might delay buying a new car or upgrading their phone. These are discretionary purchases: non-essential items that can be postponed until financial conditions improve.

In contrast, even during a recession, people still pay their water and gas bills and continue buying household essentials like groceries and personal care products.

The underlying economic principle at play here is elasticity. In economics, elasticity measures how much the quantity demanded of a product changes in response to price or income changes.

Goods with inelastic demand see little fluctuation in consumption, even when prices rise or consumer income declines. This makes sectors with inelastic demand more stable during market downturns.

Utilities: Electricity, water, and gas are necessities that households and businesses must pay for, regardless of economic conditions.

Consumer Staples: Essential items like food, personal care products, and household goods remain in demand even when discretionary spending drops.

Health Care: Medical services, prescription drugs, and insurance are critical expenses that people prioritize, often regardless of cost.

How defensive are these sectors?

One way to quantify how defensive a sector has historically been is to look at its beta, a measure of volatility relative to the broader market3.

The market itself has a beta of 1.0, meaning any stock or sector with a beta below 1.0 tends to be less volatile and moves less than the overall market during upswings and downturns.

When analyzing long-running sector ETFs, the historical five-year betas confirm that health care, consumer staples, and utilities have lower volatility than the broader market.

The Health Care Select Sector SPDR Fund (XLV) has a beta of 0.644, The Consumer Staples Select Sector SPDR Fund (XLP) comes in even lower at 0.575, and The Utilities Select Sector SPDR Fund (XLU) has a beta of 0.746. This suggests that all three sectors historically experience smaller price swings compared to the S&P 500.

Further supporting this, research from State Street Global Advisors examined periods of steep market drawdowns. Between 1999 and 2022, there were 11 instances where the S&P 500 declined by 10% or more in a single quarter7.

They found that an equally weighted portfolio of health care, consumer staples, and utilities delivered significantly smaller losses than both the S&P 500 and the Russell 1000 Value Index.

Morningstar direct. Data as of 6/30/227

This demonstrates how overweighting defensive sectors has historically provided better downside protection in times of market stress versus broad market indices.

The ETFs for the job

BMO’s lineup of SPDR Select Sector Index ETFs includes three options that align with the defensive sectors discussed earlier. These ETFs provide targeted exposure to U.S. health care, consumer staples, and utilities, ensuring investors can overweight these segments without exposure to the rest of the S&P 500. Continue Reading…

The four words ‘this time its different’ were made famous by Sir John Templeton as an admonition against the overzealous embrace of new paradigms.

To him, there is nothing new under the sun regarding the interplay of valuations and emotions in the emergence of investing bulls and bears. The thing is, sometimes the world changes in such a fundamental way that there really are no antecedents.

For example, where is the precedent for having the gangster in the White House? As a thought exercise, imagine if Al Capone could have become President in the 1930s. Here’s a man who managed to avoid being brought to justice (sound familiar?), who ran his empire using violence and the threat of violence, and who, for a time, was wildly popular among those who knew him. He was petulant and reactive; not strategic and thoughtful (again, does that sound familiar?)

As of mid March, the U.S. has surrendered its status as a constitutional democracy, as the President has effectively put himself above the law by ignoring a court order. This is unprecedented. Nothing like it has ever happened before. It’s different. The United States is no longer a country of laws, it is a country of unbridled power for the person at the top. To paraphrase a recent article in Time magazine:

“… a court that cannot enforce its rulings is not a court – it is a suggestion box…. and a presidency that can ignore the courts without consequence is no longer constrained by law – it is an untouchable executive”.

No more wind in our sales from Bond Bull market

There are other things that are different in 2025, too. For starters, the world is dealing with an existential crisis – climate change – the likes of which has never been seen before. Then there are the challenges that, while not unprecedented in history, have not been encountered in our lifetimes. Debt levels, both private and public, are at their highest level since World War II. A bull market in bonds that lasted over 40 years ended a few years ago due to the normalization of rates coming out of COVID. There will be no more wind in our economic sails, as has been the case throughout the entirety of the investing lifetimes of everyone reading this.

The peace dividend has been paid out. Everywhere throughout the world, countries are rearming because of geopolitical instability that has arisen out of autocratic powers that seem determined to acquire new territory at all costs. Not only is this destabilizing geopolitically, it also diverts expenditure into military pursuits that would have otherwise gone toward expanding the economy and/or some element of improved social justice.

Deglobalization is very much part of this new reality, too. Tariff barriers are being erected by the gangster madman, and countries around the world feel they have no meaningful recourse other than to reciprocate in retaliation, thereby exacerbating the needless self-inflicted harm. Continue Reading…

Theatrical release poster for the film, Idiocracy. via Wikipedia.

By Mark Seed, myownadvisor

Special to Financial Independence Hub

A few months ago I wrote:

“Yes, interesting times may call for interesting portfolio changes! Or not. :)”

Well, here we are.

Regardless about how you feel about the current U.S. Administration, I would think most people would agree that this U.S. President feels very emboldened right now. With no future term to go: this is his last shot at taking shots at pretty much anything and everyone he wants without too many consequences near-term. At least it seems that way …

Since writing this post below from December I thought I would update such a post about any recent portfolio changes and beyond that, how our shopping habits have shifted (if at all) in recent months.

How to invest and shop during Trump idiocracy

I put the term “idiocracy” in the post title since it’s very much how I feel right now.

It’s like watching the Ferris Bueller movie scene: on tariffs.

History repeats.

Now that tariffs are in place and we’re now in a (trade) war between Canadian and U.S. businesses, consumers and workers (sadly), I’m expecting these tariffs will roil stock markets for months or years to come.

I have.

This is how I intend to invest and shop during some prolonged Trump idiocracy.

Approach #1 – What investments can withstand stagflation?

New tariffs are likely, in my opinion, to trigger a sustained period of low economic growth and even higher inflation: which will impact everyone.

At the most basic level, inflation means a rise in the general level of prices of goods and/or services over a period of time. When inflation occurs, each unit of currency buys fewer goods and services. Inflation results in a loss in the value of money and purchasing power. We will all be impacted by this.

Stagflationis essentially a combination of stagnant economic growth, high unemployment, and high inflation. When you think about it …. this combination probably shouldn’t exist: prices shouldn’t go up when people have less or no money to spend. This could be a place where things are trending…

Farmland might perform well during stagflation but we don’t own any.

Instead, I own some “defensive stocks” including some in key economic sectors like consumer staples, healthcare and utilities in my low-cost ETFs that should be able to weather a prolonged disruption. I also consider a few selected stocks we own as defensive plays: waste management companies. At the time of this post, both Waste Management (WM) and Waste Connections (WCN) we own have held up very well and provided stellar returns over the last 5+ years that I’ve owned them.

WM is up almost 100% in the last 5-years.

WCN is up over 100% in the last 5-years.

We’ll see what the future brings and my low-cost ETFs are a great diversifier: regardless.

Approach #2 – Staying global while keeping cash

Beyend certain sectors, investors should always consider holding a well-diversified stock portfolio across different sectors and different economic regions to reduce the long-term reliance on industries directly affected by tariffs.

While I have enjoyed a nice tech-kicker return from owning low-cost ETF QQQ for approaching 10 years now, and I will continue to hold some QQQ in my portfolio, I could see technology stocks tanking near-term. To help offset that, I own some XAW ETF for geographical diversification beyond the U.S. stock market. Thankfully.

Times of market stress are however times to buy stocks and equity ETFs.

Near-term and long-term investing creates buying opportunities for disciplined investors. A well-structured, diversified global mix of stocks including those beyond the U.S. could provide some decent defence against a very toxic, unpredictable economic and political agenda.

For new and established readers on this site, you might be aware I’ve mentioned that our investing approach could be considered a “hybrid approach” – a structure that was established about 15 years ago as follows:

We invest in a mix of Canadian stocks in our taxable account: to deliver income and some growth, and

Beyond the taxable account, we own a bunch of low-cost ETFs like QQQ and XAW inside our registered accounts: inside our RRSPs, TFSAs and my LIRA for extra diversification.

I like the hybrid approach, the process and the results to date.

At the time of this post, I just don’t see how I should be making any significant changes to our equity portfolio.

Beyond our portfolio of stocks and equity ETFs we keep cash/cash equivalents.

Cash savings remains a good hedge for a very uncertain near-term future. We have a mix of Interest Savings Accounts (ISAs) / High Interest Savings Accounts (HISAs), along with Money Market Funds (MMFs) in particular in our registered accounts. Generally, plain-vanilla savings accounts offer very low interest rates. So, if you want to earn more on your savings deposits (rather than simply using your savings account) then consider an ISA or HISA.

The greatest appeal of ISAs and HISAs for taxable savings IMO is liquidity, while earning interest, and member financial institutions of Canada Deposit Insurance Corporation (CDIC) insure savings of up to $100,000. It’s good business for banks and institutions as well since money deposited generates interest by allowing the bank to access those funds for loans to others. There are usually no fees for these accounts and while interest rates have come down in recent months, ISA and HISA interest rates are consistently north of 2% at the time of this post.

I believe some form of savings account / ISA / HISA remains the cornerstone of everyone’s personal finance portfolio since 1. your money is saved for future expenses or ready for emergencies, 2. it is safe/low risk, 3. it is liquid, and 4. you still earn returns.

Let your equities do as they wish after that.

Approach #3 – Shop local, buy local, and avoid U.S. travel

We are fortunate to live in an area in Ottawa where we can shop local and buy from local farmers. We will continue to do that.

For those that want to shop more in Canada and buy more Canadian goods visit here:

We’ve been fortunate to save up some money in our “sunshine fund” as I call it for some future travel. I/we have no near-term plans to spend our money in the U.S.

I’ve been fortunate to visit many, many U.S. States over the years but given this recent trade war initiated by this current U.S. Administration I hardly have any desire to spend my money in a country whereby that government talks about annexing us.

It’s that simple for us.

I encourage other Canadians who can and do travel, to consider the same – avoiding the U.S. – not because of its citizens but the U.S. Administration decisions. Continue Reading…