By Mark Seed, MyOwnAdvisor

Special to the Financial Independence Hub

The term “financial independence” has many meanings to many people.

To some, this means the ability to work on your own terms.

To others, it boils down to not working at all but instead having “enough” to meet all needs and possible wants.

Where do I stand on this subject? This post will tell you in my six phases to financial independence.

Retirement should not be the goal: Financial security and independence should be

Is retirement your goal? To stop working altogether? While I think that’s fine I feel the traditional model of retirement is outdated and quite frankly, not very productive.

As humans, even our lizard brains are smart enough to know we need a sense of purpose to feel fulfilled. Working for decades, saving money for decades, only to come to an abrupt end of any working career might work for some people but it’s not something I aspire to do.

With people living longer, and more diverse needs of our society expanding, the opportunities to contribute and give back are growing as well. To that end, I never really aspire to fully “retire”.

Benefits of financial independence (FI)

In the coming years, I hope to realize some level of financial security and eventually, financial independence. For us, this is a totally worthwhile construct. The realization of FI can bring some key benefits:

- The opportunity to regain more control of our most valuable commodity: time.

- Enhanced opportunities to learn and grow.

- Spend extra money on things that add value to your life, like experiences or entrepreneurship.

Whether it’s establishing a three-day work week, spending more time as a painter, snowboarder, or photographer, or you desire to get back to that woodworking hobby you’ve thought about: financial independence delivers a dose of freedom that’s hard to come by otherwise.

FI funds time for passions.

FI concepts explained elsewhere

There are many takes on what FI means to others.

There is no right or wrong, folks: only models and various assumptions at play.

For kicks, here are some select examples I found from authors and bloggers I follow.

- JL Collins, author of The Simple Path to Wealth, popularized the concept of “F-you money”. This is not necessarily financially independent sums of money but rather, enough money to buy a modest level of time and freedom for something else.

- Various bloggers subscribe to a “4% rule”* whereby you might be able to live off your investments for ~ 30 years, increasing your portfolio withdraws with the rate of inflation.

*Based on research conducted by certified financial planner William Bengen, who looked at various stock market returns and investment scenarios over many decades. The “rule” states that if you begin by withdrawing 4% of your nest egg’s value during your first year of retirement, assuming a 50/50 equity/bond asset mix, and then adjust subsequent withdrawals for inflation, you’ll avoid running out of money for 30 years. Bengen’s math noted you can always withdraw more than 4% of your portfolio in your retirement years however doing so dramatically increases your chances of exhausting your capital sooner than later.

For simplistic math, such bloggers calculated your “FI number” could be approximately your annual expenses x 25. So, if you’re annual expenses are about $40,000 per year (CDN $ or USD $ or other), then your “FI number” is a nest egg value of $1,000,000.

Using that framework, there are levels of FI some bloggers have adopted:

- Half FI – saved up 50% of the end goal (in this case, $1 M).

- Lean FI – saved up >50% of end goal to pay for very lean but life’s essentials like food, shelter and clothing (but nothing else is covered).

- Flex FI – saved up closer to 80% of the end goal, this stage covers most pre-retirement spending including some discretionary expenses.

- Financial Independence (FI) – saved up 100% of the end goal, you have ~ 25 times your annual expenses saved up whereby you could withdraw 4% (or more in good markets) for 30+ years (i.e., the 4% rule).

- Fat FI – saved up at or > 120% of your end goal (in this case $1.2 M for this example), such that your annual withdrawal rate could be closer to 3% (vs. 4%) therefore making your retirement spending plan almost bulletproof.

- There is the concept of “Slow FI” that I like from The Fioneers. The concept of “Slow FI” arose because, using the Fioneers’ wording while “there were many positive things that could come with a decision to pursue FIRE, but I still felt that some aspects of it were at odds with my desire to live my best life now (YOLO).” They went on to state, because “our physical health is not guaranteed, and we could irreparably damage our mental health if we don’t attend to it.”

Well said.

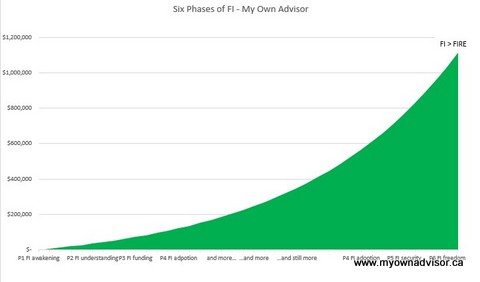

My six phases of financial independence

To the “Slow FI” valuable points, since we all only have one life to live, we should try and embrace happiness in everything we do today and not wait until “retirement” to find it.

After reviewing these ideas above, among others, I thought it would be good to share what I believe are the six key phases of any FI journey: including my own.

Phase 1 – FI awakening. This is where there is an awareness or at least an initial desire to achieve FI even if you don’t know exactly how or when you might get there.

(I had my awakening just before I decided to become My Own Advisor, triggered by the financial crisis of 2008-2009.)

Phase 2 – FI understanding. This is the phase where people are getting themselves organized; they start to diligently educate themselves on what their personal FI journey might be.

(I would say it took me until my mid-30s to get my financial life in order through more financial education and improved financial literacy. It was a process that took a couple of years although I’m always continuously learning and improving. I don’t pretend to know it all.)

Phase 3 – FI funding. In this phase, people start to realize some financial stability. Maybe the emergency fund is now fully established. Usually an approach to long-term investing has been solidified. More than likely, student loan debts are being dissolved for the 20-somethings or 30-somethings OR better still, those types of loans are completely put to rest for good.

In phase 3, debt management is under control: you might have a mortgage or a car payment but you’re learning to curb your financial behaviour for the better.

Maybe you’ve already made the crucial decision to become debt-free first or invest first.

This was my definitive answer to the paying your mortgage first or investing first debate.

The FI funding phase also means you’ve taken steps to start optimizing your financial life: reducing waste and excess. It’s doesn’t mean you’re perfect but you do start to align your spending with your financial values.

(In speaking about my own FI funding experiences, my wife and I really upped our FI journey once we landed on our two-pronged investing approach: owning a basket of dividend paying stocks for growing income AND continually buying more low-cost ETF units for long-term growth. I believed then (like I continue to believe now) our hybrid approach will deliver a masterful 1-2 investing punch to achieve FI.)

To pause here, phases 1-3 are really about financial organization. While FI is in the distant future you’ve put the necessary building blocks in place for future success.

Phase 4 – FI adoption. This phase is where routine, but often diligent combinations of debt repayments + investing are occurring over time. Somewhere early in your FI adoption phase, probably in your 20s and 30s, you’ve embraced the merits of having a cash emergency fund. In this case, should an emergency or an unfortunate unemployment situation were to occur, it would not cause financial ruin.

In phase 4, in addition to the cash cushion, there are also investments in the bank to ride out a financial storm for multiple months or quarters, or maybe even a few years.

With your FI brain fully engaged, you’re actively executing on your FI plan. There is no longer any second-guessing about what to invest in, why; you’re not rattled by stock market noise or various reports. You’ve carved out your FI path.

You don’t have to have targets of Half FI, Lean FI or anything else because you continue to optimize your life on your terms. Your process of planning and re-planning is working in your favour to reach your goal.

Admittedly, because “I’m here” in this phase, I can tell you this is absolutely the longest one.

The growth curve feels like it’s taking forever. Yet looking back, it’s tremendous to see how far we’ve come over the last decade: markets enabling of course.

Now that you’ve fully adopted your FI journey, you’ve accepted that journey could take many years or even a few decades, depending upon your path to FI. It is highly dependent on your savings rate, savings amount, and the ability to cut back expenses.

(My wife and I have determined that somewhere around age 50 is when we could be reasonably considered FI on our terms. I hope to post a new financial freedom update on that front later this month.)

Phase 5 – FI security. This phase is where your basic living needs (home expenses, groceries, other small necessary items like insurance) are covered by the cash flow from your investments (the combination of distributions, dividends, interest, or selling some assets as needed) and/or from passive income sources like rental income or royalties.

FI security doesn’t offer you cash for life, but it does cover many basic needs associated with it.

Based on how much you might have saved and invested, you could likely live a frugal existence for the coming decades. FI security is on the edge of full-on financial independence.

(My wife and I aren’t there yet but we are getting close to realizing this phase. For example, I calculated if we have no debt, we’d be in this phase now. We’re optimistic that dividend income (without selling any assets) from our non-registered portfolio alone should cover our condo property taxes and our condo fees for life: sometime next year. Those expenses are estimated to be in the range of $12,000 per year. Those expenses will likely increase with inflation over time. We’re optimistic that dividend raises from the companies we own will help offset those inflationary costs.)

FI security equates to a financial Crossover Point. The Crossover Point was popularized in the book Your Money or Your Life. This is the point whereby investment income matches or ideally exceeds common monthly expenses on a consistent basis. Reaching your personal Crossover Point means you have a steady income stream for life.

Phase 6 – FI freedom. You’ve made it! This is what I consider the final phase in my FI journey, where truly all expenses (basic and discretionary) are covered by existing and more than likely growing assets (if you did not significantly draw down your portfolio at all).

You could live off distributions or dividends in the range of 3-4% in perpetuity.

There is no need to work at all, although some people may choose to do so for social, physical, mental and other wellness benefits. (I intend to.) Some of these wellness benefits even escaped a financial classic that sold millions of copies – The Millionaire Next Door.

As part of your FI Freedom Day, the income delivered to you (from your investment portfolio, from other assets such as rental income) cover everything you need and more. Since you’re well beyond FI security now, you can buy those gently used vehicles every few years – if you wanted; travel more on your own terms – if you wanted; upgrade your lifestyle with better food decisions – all without ever worrying about breaking the bank.

At the frothy end of the FI freedom phase, you might have FI surplus – an abundance of cashflow whereby you can be more philanthropic to causes or events that make a positive contribution to the lives of others.

Oddly enough, you might not even be debt-free when you reach your FI Freedom Day. This is because you could readily pay off any liabilities (e.g., rental properties) without any long-term financial consequences.

The sum of phases 3-6 are labelled by me as financial actualization. The building blocks you established as part of financial organization allowed you to realize your goals. By phase 6, you’ve been so effective and efficient at your financial management processes over the years, they’ve become second nature and part of your DNA.

Having enough thoughts

Whether you choose to share your hard-earned wealth with others, via a family legacy, bequeath, or on you alone, the choice becomes yours with the dawn of FI Freedom Day.

Ultimately good health is the best possible form of wealth but that’s a subject for another day.

When it comes to money management I’m convinced if you follow my six phases of financial independence, whatever you call your FI journey, I suspect you’ll find what you’re looking for at whatever pace you wish.

Mark Seed is a passionate DIY investor who lives in Ottawa. He invests in Canadian and U.S. dividend paying stocks and low-cost Exchange Traded Funds on his quest to own a $1 million portfolio for an early retirement. You can follow Mark’s insights and perspectives on investing, and much more, by visiting My Own Advisor. This blog originally appeared on his site on Oct. 17, 2019 and is republished on the Hub with his permission.

Mark Seed is a passionate DIY investor who lives in Ottawa. He invests in Canadian and U.S. dividend paying stocks and low-cost Exchange Traded Funds on his quest to own a $1 million portfolio for an early retirement. You can follow Mark’s insights and perspectives on investing, and much more, by visiting My Own Advisor. This blog originally appeared on his site on Oct. 17, 2019 and is republished on the Hub with his permission.