Pleased to meet you

Hope you guess my name

But what’s puzzlin’ you

Is the nature of my game

- Sympathy for the Devil, by The Rolling Stones

By Noah Solomon

Special to Financial Independence Hub

Historically, bonds have offered investors two main benefits. Firstly, their yields provided a reasonable, if unspectacular return. Secondly, they offered diversification value, muting overall portfolio losses during bear markets.

In my view, it is the second attribute that is the most important. In relative terms, bonds are not particularly useful for providing investors with strong long-term returns (that’s equities’ job!). So, by process of elimination it follows that the primary function of bonds is their diversification value.

When comparing equity strategies, one should compare their relative returns, volatilities, Sharpe ratios, drawdown characteristics, etc. However, given bonds’ primary purpose of providing diversification, an extra layer of diligence is required when evaluating bond strategies. Specifically, you should analyze their differing correlations to equities, and by extension their varying abilities to offset stock price declines during challenging environments.

There is no Free Lunch Part I

Economist and Nobel Prize recipient Milton Friedman famously stated, “There is no such thing as a free lunch,” which means that every choice has a cost, even if it’s not immediately obvious.

Traditional bond mandates each have their individual advantages and pitfalls with respect to returns, risks, and diversification properties. In terms of the tradeoff between risk and return, history strongly suggests that there is no clear free lunch to be had.

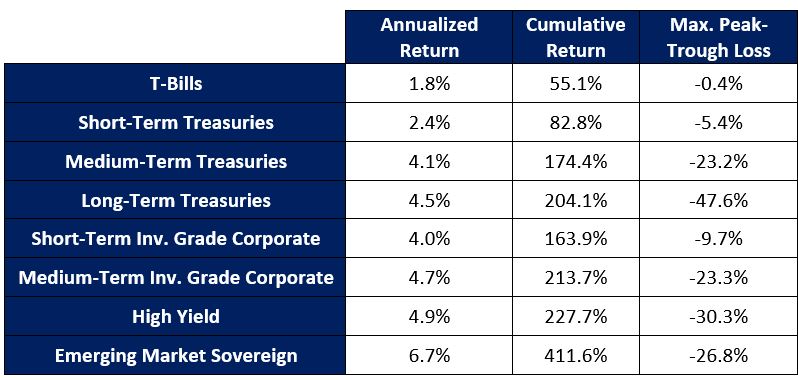

Risk vs. Return by Bond Type: 2000 – 2024

As the above table illustrates, there is a clear relationship between the returns of the various segments of the bond market and the maximum losses that they have sustained over the past 25 years. If you want extra return, you can reasonably expect to suffer larger losses in bad times. That being said, large losses in bond holdings are generally not what investors want or expect.

There is no Free Lunch Part II

Not only is there no free lunch with respect to the tradeoff between risk and return, but there is also none when it comes to diversification value. Higher returns are not only associated with larger losses but are also associated with higher correlations to equities.

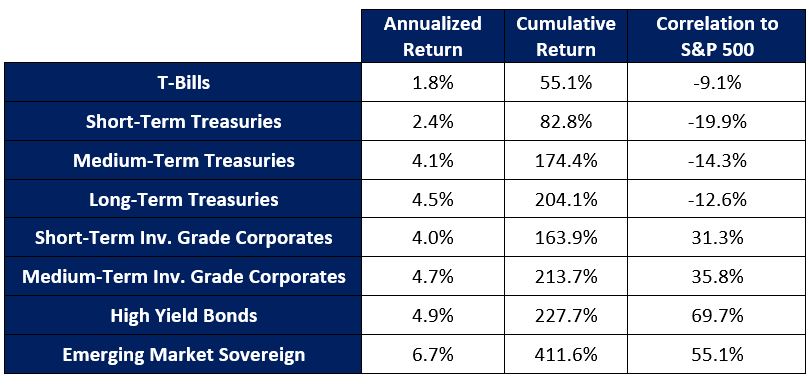

Return vs. Correlation to Stocks by Bond Type: 2000 – 2024

Bonds that offer higher returns have a greater tendency to move in tandem with stocks, thereby providing less ability to mitigate stock losses during bear markets. In contrast, lower-return bonds possess greater diversification properties and thus are better equipped to offset stock-price declines during times of equity market turmoil.

None of the above: Sometimes there’s Nowhere to Hide

Notwithstanding the fact that higher-return bonds have on average suffered more severe losses and offered less diversification value than their lower return counterparts, these relationships have exhibited significant variations across different bear markets.

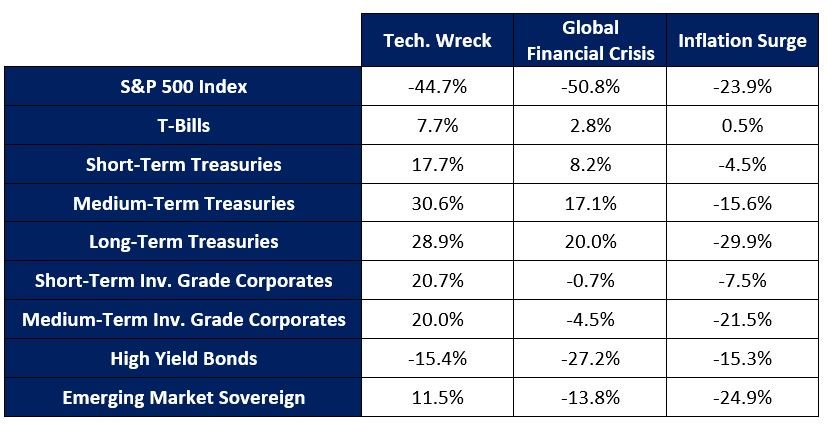

Bear Market Performance by Bond Type

During the Tech Wreck of the early 2000s, all manner of bonds posted gains, with the exception of high-yield bonds. Interestingly, medium-term investment grade corporate bonds rose more than Treasuries of similar duration, thereby providing a better offset to stock price declines. In addition, despite being one of the riskier segments of the bond market, emerging market sovereign bonds also posted significant gains.

Moving on to the global financial crisis, the data offers a somewhat different picture. Whereas Treasuries of all durations provided some ballast within balanced portfolios, other segments of the bond market failed to do so, with high yield and emerging market bonds suffering substantial losses.

Finally, during the inflation scare of 2022, there was no corner of the bond market that offered a safe harbour. Any bond portfolio containing meaningful duration or credit risk was punished severely, with the higher-risk corners of the bond market suffering the most severe losses. Specifically, medium-to-long-term Treasuries (the “heroes” of prior bear markets), medium-term investment grade corporate bonds, high-yield bonds, and emerging market bonds all experienced losses of over 15% to nearly 30%. Simply stated, there was nowhere to hide, with only T-Bills (i.e. cash) emerging unscathed.

Forrest Gump described life as being “like a box of chocolates. You never know what you’re gonna get.” Similarly, bonds have and can perform very differently in bear markets, offering anywhere from substantial to no protection from sharp declines in stock prices. What has worked in some bear markets has not in others.

A word about Liquidity and Optionality

Barton Biggs, who during his tenure at Morgan Stanley became known as one of the world’s foremost global investment strategists, stated, “Liquidity is a coward. It disappears at the first sign of trouble.”

Not only can corporate bonds fail to provide portfolio protection during equity bear markets but can also be ominously illiquid. In such environments, when many investors seek to liquidate positions, the corporate bond market has historically exhibited a tendency to freeze up. Those wishing to sell face considerable difficulty doing so. Even if they are successful, it is at severely discounted prices. This issue, which is especially pronounced in the Canadian corporate bond market, resulted in TELUS bonds trading at approximately 65 cents on the dollar during the global financial crisis. The bottom line is that corporate bond liquidity, and by extension the ability to sell, is most challenging when it is most needed.

Turning to the explosive growth in private debt markets over the past decade, issues regarding liquidity are even more concerning. Notwithstanding that corporate bond markets tend to “malfunction” in bad markets, this issue is far less pronounced than with private debt markets. During times of heightened stress, private-debt investors who succeed in liquidating their holdings at significant discounts should consider themselves fortunate, as there are many positions that become practically unsellable.

Importantly, the tendency of corporate bonds and private debt to suffer significant losses and become illiquid during bear markets can deprive investors of meaningful option value. After suffering massive declines during the global financial crisis, stocks bottomed out in mid-March of 2009. Over the course of the following several months, investors would have been well-served to take advantage of undervalued stocks and reallocate a larger portion of their portfolios to equities.

However, to the extent that this would have necessitated liquidating corporate bond positions, this would have confounded the process. Not only would issues surrounding liquidity have posed problems, but losses in corporate bond positions would have left investors with less dry powder to allocate to equities. In essence, liquidity issues and losses saddled investors with significant opportunity costs.

Not a Free Lunch … but still a Bargain

I make no claim that there is any sure thing that “solves” the aforementioned tradeoffs between return, risk, correlation, and liquidity (if I did, you should stop reading!). However, I do believe that there is a different approach that offers a better combination of these attributes.

The Outcome Tactical Bond Fund uses a 100% rules-based, algorithmically driven approach to tactically alter the duration and credit profiles of its portfolio on a monthly basis, with the objective of reaping the return premium of longer-duration and higher-yield bonds while minimizing drawdowns in challenging environments.

Importantly, should its underlying signals dictate, the strategy has the ability to partly or entirely invest in cash. Lastly, the portfolio tends to have a lower correlation to equities than traditional bond mandates, thereby providing superior diversification for balanced portfolios.

Please feel free to contact me if you would like more information about the Outcome Tactical Bond Fund, which offers a different, logical, and value-added approach to fixed-income investing.

Noah Solomon is Chief Investment Officer for Outcome Metric Asset Management Limited Partnership. From 2008 to 2016, Noah was CEO and CIO of GenFund Management Inc. (formerly Genuity Fund Management), where he designed and managed data-driven, statistically-based equity funds. Between 2002 and 2008, Noah was a proprietary trader in the equities division of Goldman Sachs, where he deployed the firm’s capital in several quantitatively-driven investment strategies.Prior to joining Goldman, Noah worked at Citibank and Lehman Brothers.

Noah Solomon is Chief Investment Officer for Outcome Metric Asset Management Limited Partnership. From 2008 to 2016, Noah was CEO and CIO of GenFund Management Inc. (formerly Genuity Fund Management), where he designed and managed data-driven, statistically-based equity funds. Between 2002 and 2008, Noah was a proprietary trader in the equities division of Goldman Sachs, where he deployed the firm’s capital in several quantitatively-driven investment strategies.Prior to joining Goldman, Noah worked at Citibank and Lehman Brothers.

Noah holds an MBA from the Wharton School of Business at the University of Pennsylvania, where he graduated as a Palmer Scholar (top 5% of graduating class). He also holds a BA from McGill University (magna cum laude). Noah is frequently featured in the media including a regular column in the Financial Post and appearances on BNN. This blog originally appeared in the October 2025 issue of the Outcome newsletter and is republished here with permission