By Ian Duncan MacDonald

By Ian Duncan MacDonald

Special to the Financial Independence Hub

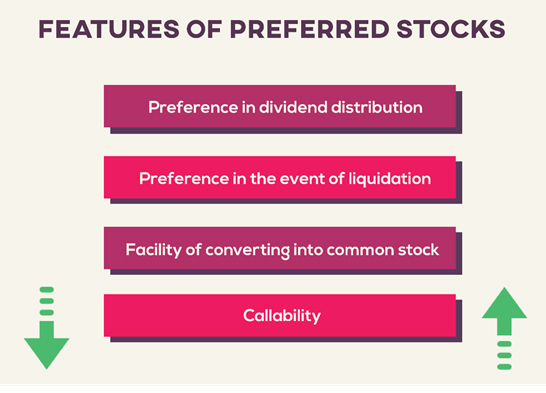

You identify preferred shares by their stock symbols. Their symbol contains a “PR” or a “PF.” For example, an Enbridge Inc. preferred share is ENB.PR.N.

Preferred shares pay dividends, often in the range of 5 or 6 per cent. This is usually one or two per cent more than what the company pays common share holders.

Like a bond, they are a form of loan; thus they do not share in the capital gain of a corporation, nor do they have any ownership or voting rights. While they rank ahead of common shares in realizing money from a company’s liquidation, they rank behind bondholders. Their ranking is of little benefit. After the lawyers, bankruptcy trustees and the banks (with their fully secured debentures) are paid off, the chance of anything being left for distribution is just about nil.

While you can conveniently buy and sell preferred shares on the stock market very few investors have any interest in them. Zero trades in a day is not unusual. There are 654 shares on the TSX pay paying a dividend of 3.5%. or more. Of these, 364 are preferred shares and of those only 112 had more than 4,000 shares traded in a typical day, despite their high dividends. This is due to the low possibility of preferred shares delivering an increase in share price to speculators.

Preferred shares are issued at a standard price of $25 each. Of the 364 preferred shares only 17 had a share price exceeding $25 and of these only one was greater than $30. The chance of realizing a capital gain from a preferred share is 1.91% and 183 or (50% of them) had lost at least 20% of their value. They were now worth less than $20. Five were trading for less than $10. It is not surprising that not one analyst recommended that investors buy any of these 364 preferred shares.

Issuers can call them back in

Three further complications discourage stock buyers. If interest rates decrease, the corporation, who issued the preferred shares, can call them in and issue new preferred shares paying a lower dividend rate. As well, unlike bonds where you get back all the money you invested; with a preferred share you only get back what someone is willing to pay for a preferred share. 98% of the time the price would be less than the $25 they were issued at. Finally, if a company runs into financial difficulty, unlike bonds, a company can suspend paying all dividends, including those for preferred shares.

Preferred shares are cheaper than bank loans, without the payment commitments of bonds. While the value of a company’s assets limits how much a corporation can borrow from a bank, assets do not secure preferred shares. The number of preferred shares issued seems to be limited by what the corporation “thinks” they can afford to pay out in dividends. Executives, with their annual stock option incentives tied into a rising common share price, promote preferred shares because their issue, unlike the issue of new common shares, does not interfere with their chances to make bonus money.

If preferred shares are likely to give you a capital loss, why would you add them to your portfolio? To guarantee that you do not outlive your savings you need the capital gain of common shares. I identify many good ones in my book “Income and Wealth from Self-Directed Investing” [cover shown below] that pay a higher dividend than preferred shares.

After graduating from McMaster University, with $100 left in his pocket (but no student debt), Ian Duncan MacDonald hitch hiked home to Sudbury to work four months as a labourer in International Nickel’s smelter. In four months, he had saved enough to seek his fortune in the big city.

After graduating from McMaster University, with $100 left in his pocket (but no student debt), Ian Duncan MacDonald hitch hiked home to Sudbury to work four months as a labourer in International Nickel’s smelter. In four months, he had saved enough to seek his fortune in the big city.

In Toronto, he was immediately hired by Dun & Bradstreet as a credit reporter. While he had expected to be a reporter for the rest of his life, D&B had other plans. Within four years, he was General Manager of their Marketing Services Division. Three years later, at the age of 28, he was responsible for the sales, marketing and advertising for all three divisions of the company.

At 32, he left D&B to build Screening Systems International Ltd, for a large conglomerate, which led to his interest in collections. Moving to Creditel of Canada Ltd. he became Senior Vice President. Subsequently bought by Equifax, he remained there until his retirement in 2005. In anticipation of his retirement he incorporated Informus

At 32, he left D&B to build Screening Systems International Ltd, for a large conglomerate, which led to his interest in collections. Moving to Creditel of Canada Ltd. he became Senior Vice President. Subsequently bought by Equifax, he remained there until his retirement in 2005. In anticipation of his retirement he incorporated Informus

Inc. to sell his art, his publications and consulting services (www.informus.ca.)

His book “Income and Wealth from Self-Directed Investing” provides a detailed system, plus stock scoring software, which arms someone who has never invested with the knowledge they need to successfully and safely generate income and wealth for the rest of

their lives.

Too true. Bought some preferred shares as a vehicle to earn dividend income. They do that, but all are worth less than ACB. Plus, the rate reset ones where a disaster a few years back. Slowly moving out as the capital loss is greater than the dividends earned.

This book is your path to possible wealth. I am a living example and cannot talk about it enough. It has changed my life. Incredible. All I had to do was finding the courage to believe and trust. It worked. Thank you, Ian Duncan MacDonald.

Thanks Sabina for your kind words.

Replying to old article. Things may have changed since 2019! Recently, it has been possible to buy perpetual preferreds issued by companies with very low credit risk, that yield in the 6.5-7% range. These will do that for ever or at least until called. If a retiree draws 4%, this leaves 2.5-3% to cover inflation. Price of the shares will go up if interest rates drop. If interest rates go above their current high level, the share prices will drop, but the dividends will not. Seems like a good way for retirees to supplement other fixed income while taking advantage of the dividend tax credits. Rate Resets can also be attractive, but prices may be more volatile. With any preferreds, best to buy at below par for long term hold.