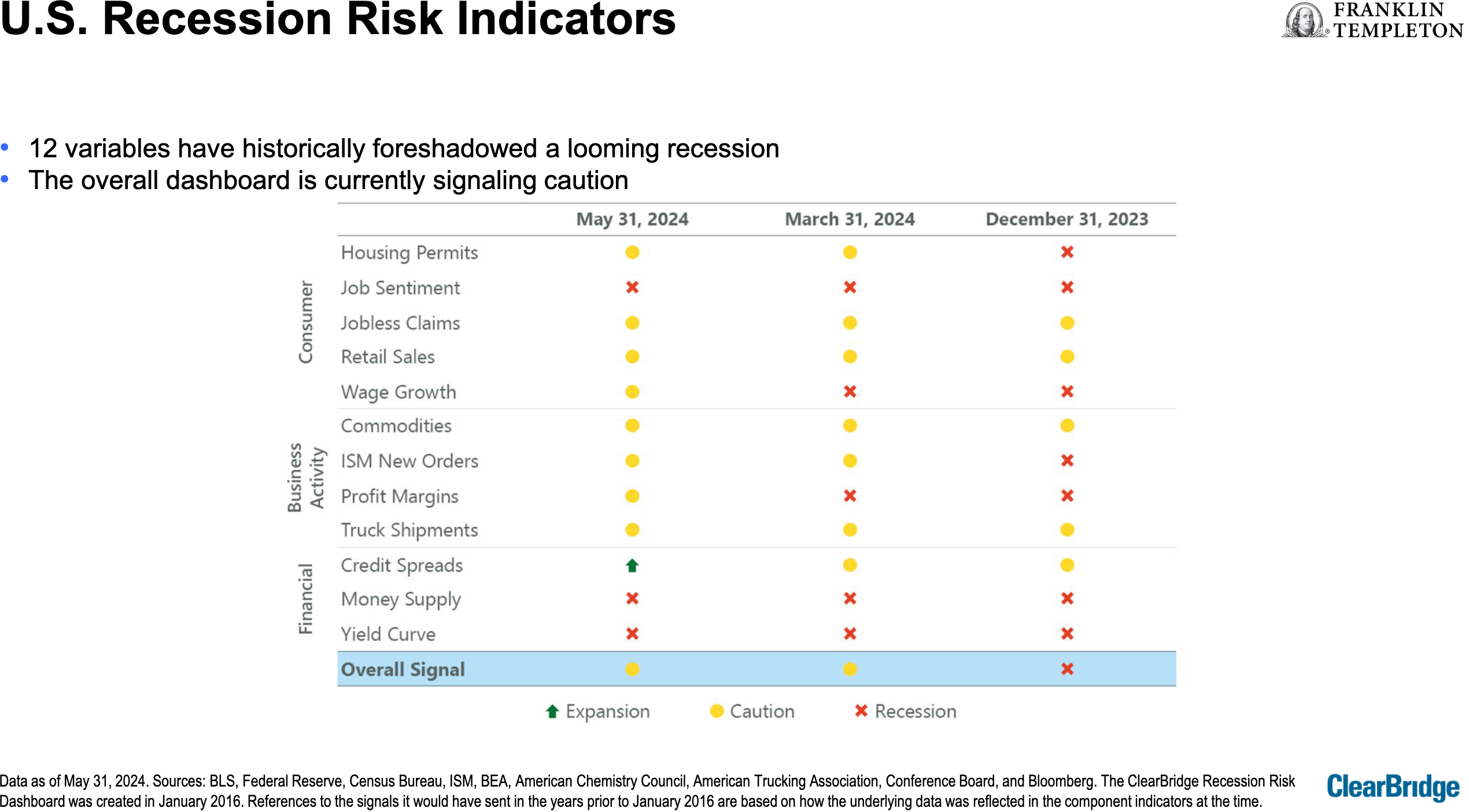

The 12 variables used to forecast Recessions are currently “signalling caution,” says Jeffrey Schulze, CFA.

Speaking Wednesday in Toronto at Franklin Templeton’s mid-year outlook, Schulze — Managing Director, Head of Economic and Market Strategy for Clearbridge Investments — told financial advisors and media that as of May 2024, the 12 variables he tracks have “historically foreshadowed a looming recession … the overall dashboard [shown below] is currently signalling caution.”

Three indicators — Job Sentiment, Money Supply and Yield Curve — have been flashing red since the end of 2023 and continue to be, as you can see in the above chart taken from a presentation made available to attendees. The only green light is Credit Spreads, while the other eight — which include Housing Permits, Jobless Claims and Profit Margins — are all a cautionary yellow.

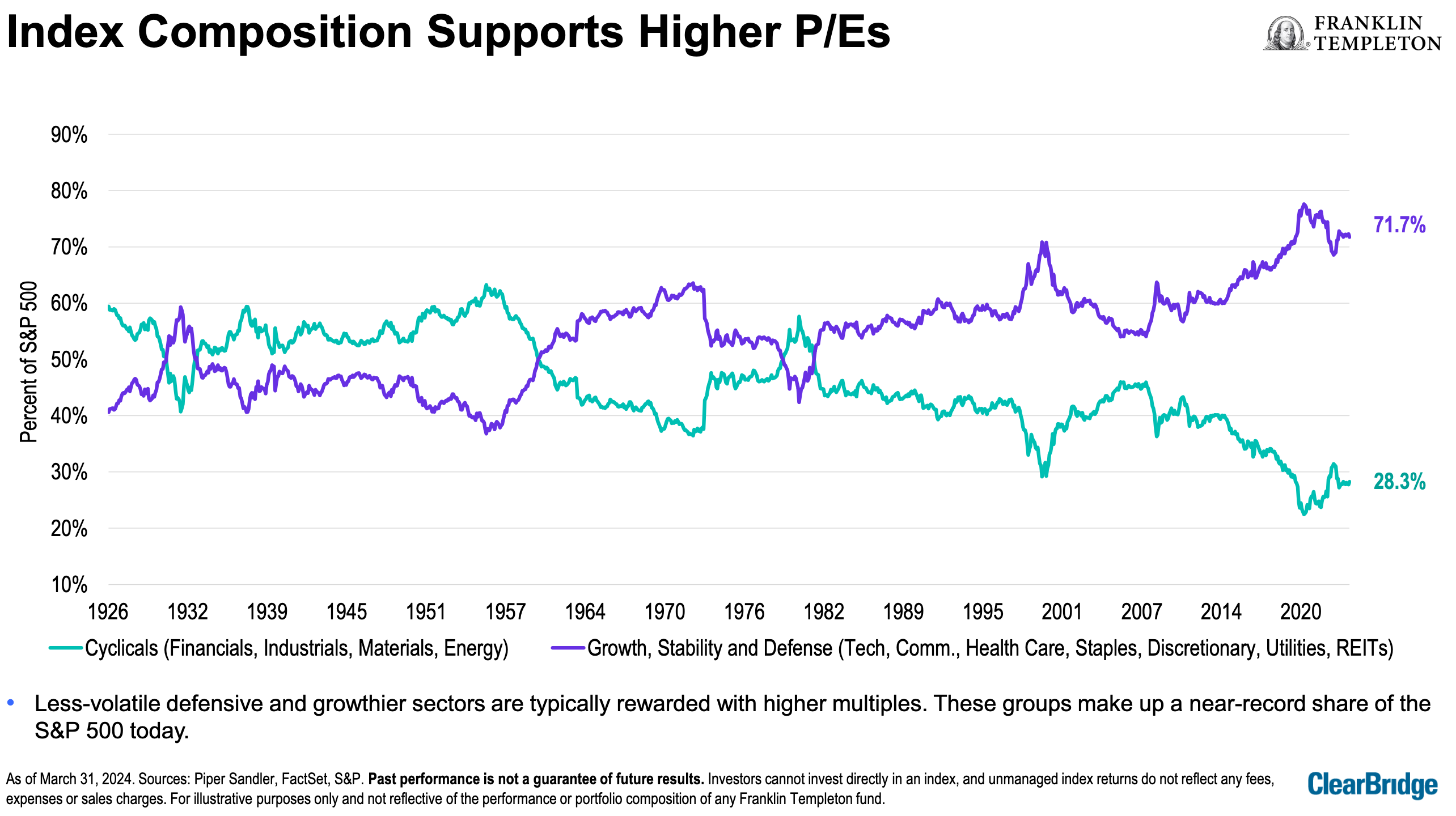

However, stock valuations do not appear to be too stretched at present. The composition of major stock indexes, such as the S&P500, support higher P/E ratios, Schulze said. “Less-volatile defensive and growthier sectors are typically rewarded with higher multiples. These groups make up a near-record share of the S&P 500 today.” As you can see in the chart below and in the higher purple line of the graph, these Defensive stocks include Tech, Consumer Staples, Utilities, and Health Care.

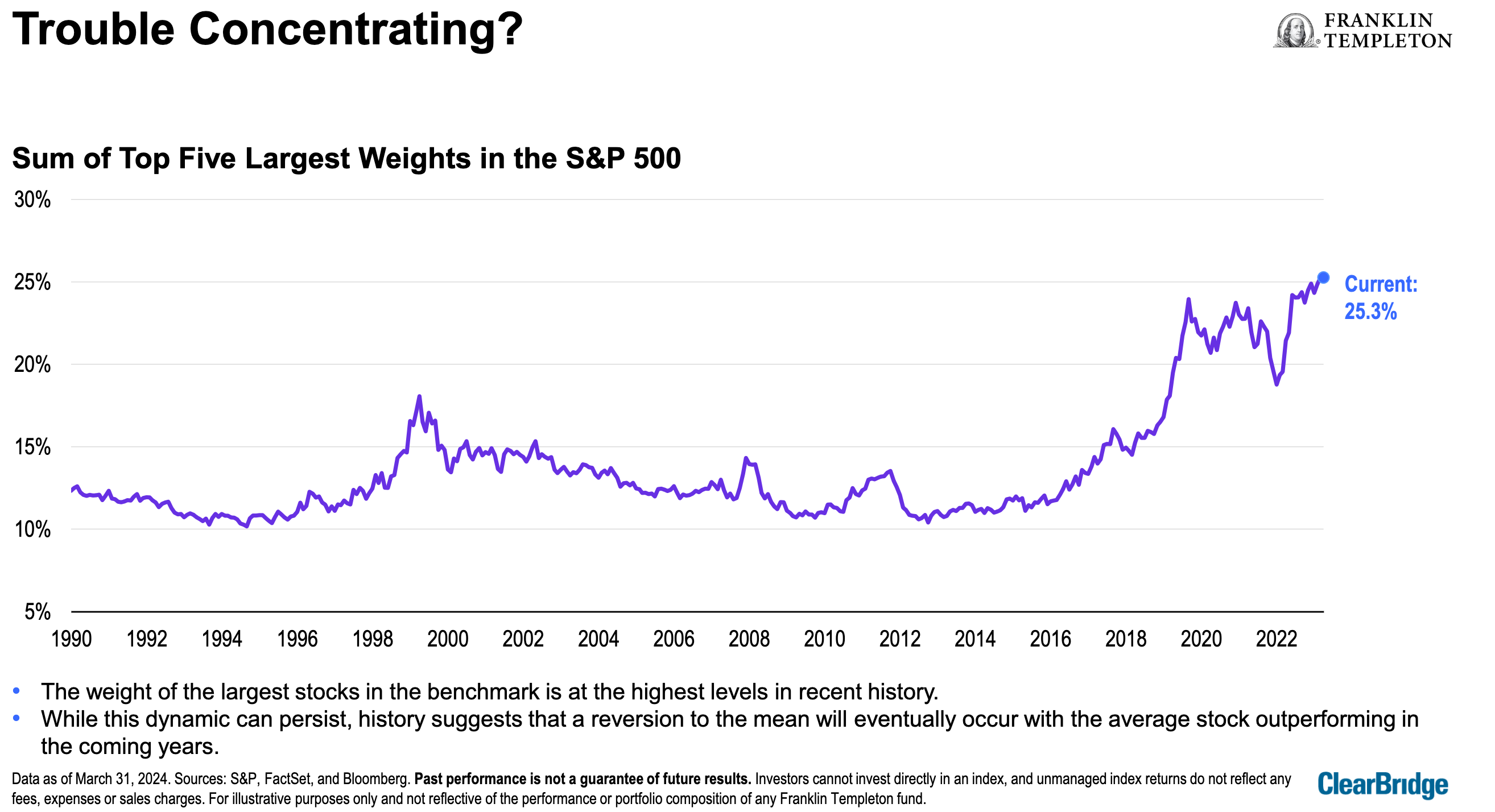

However, Schulze did note a “troubling” record-high concentration of the largest S&P500 names by market weight. As you can see in the chart below, the five largest-cap components now account for more than a quarter (25.3%) of the index, which is “the highest levels in recent history … While this dynamic can persist, history suggests that a reversion to the mean will eventually occur with the average stock outperforming in the coming years.”

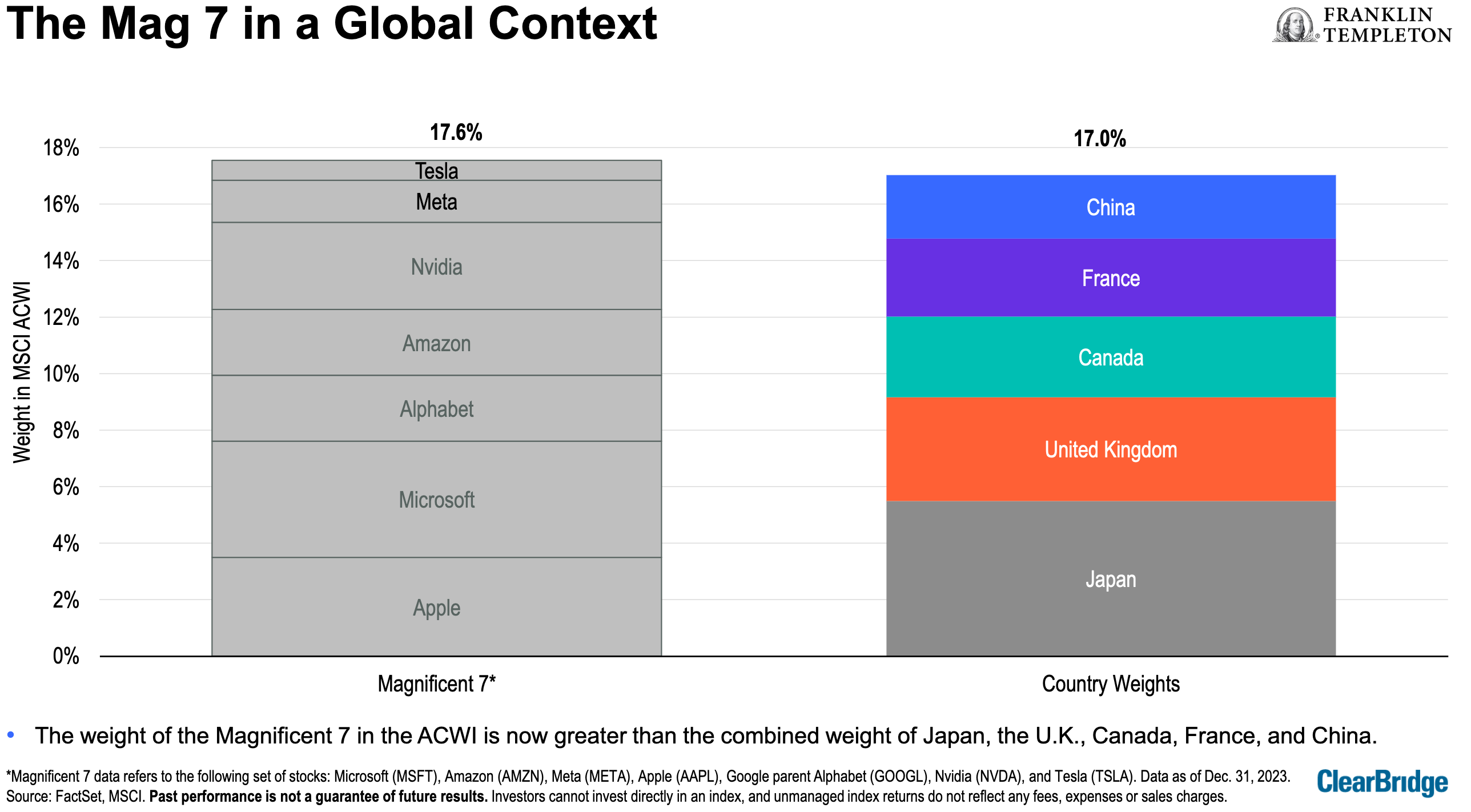

In fact, the combined weight of the so-called Magnificent 7 tech stocks now exceeds the combined market weight of the stock markets of Japan, the U.K., Canada, France, and China!

However, “after behaving fairly monolithically in 2023, the performance of the Mag 7 members have diverged substantially so far in 2024,” Schulze said. A slide of the “Divergent 7” showed Tesla down 28.3% and Apple flat, while the others were higher, led by the 121.4% surge in the price of Nvidia this year.

A key driver of the Mag 7 outperformance has been superior earnings growth, Schulze said, but “this advantage is expected to dissipate in the coming year, which could be the catalyst for a sustained leadership rotation.”

Companies that grow their dividends are overdue to start outperforming. “Over the past year, dividend growers have trailed the broader market to a degree rarely seen over the past three decades … Past instances of similar underperformance have been followed with a strong bounce-back for dividend growers.”

A positive for markets is the “copious” amount of cash sitting on the sidelines and being readied to deploy on buying stocks. After the October 2022 lows, investors flocked into money market funds with a net increase of US$1.5 trillion, or 32%, Schulze said: “Should the Fed embark upon its widely anticipated cutting cycle later this year, investors may reallocate. This represents a potential source of upside for equities.” Continue Reading…