Last month, the British Columbia Securities Commission (BCSC) launched an investor education campaign targeted at helping investors better understand the fees they pay. There simply can’t be enough education around this issue and we absolutely applaud their efforts.

Its Investright.org website is a great source of information and education and this latest campaign showcases some new tools and guides that any investor would find helpful. There are even some new TV ads which would be kind of funny if the subject matter wasn’t so serious.

New regulations came into effect on July 15 of this year which require investment advisors to provide better disclosure about their compensation. Rather than simply show percentage fees, compensation and other charges will have to be shown in dollars and cents. We expect investors to suffer a fair degree of sticker shock next year when everyone will start receiving these new mandated statements.

New statements won’t show all fees

Unfortunately the statements still won’t reveal the total fees investors are paying as they only relate to “compensation and other charges” which go directly to the advisor and the advisor’s firm. It won’t include any additional expenses paid to, say, mutual fund companies that manage the funds selected by your advisor.

For a mutual fund that comes with a management expense ratio (MER) of 2.5%, if 1% of that goes to your advisor as an annual sales commission, your statement of compensation and other charges will only show the 1%. However, it’s really the combination of high and hidden trailing sales commissions and high fund expenses that ranks Canadian mutual fund fees among the very highest in the world.

Fees make a difference – kindly Investright has put a simple fee calculator front and centre on their website which you can use to figure out how much you could save by being more fee conscious.

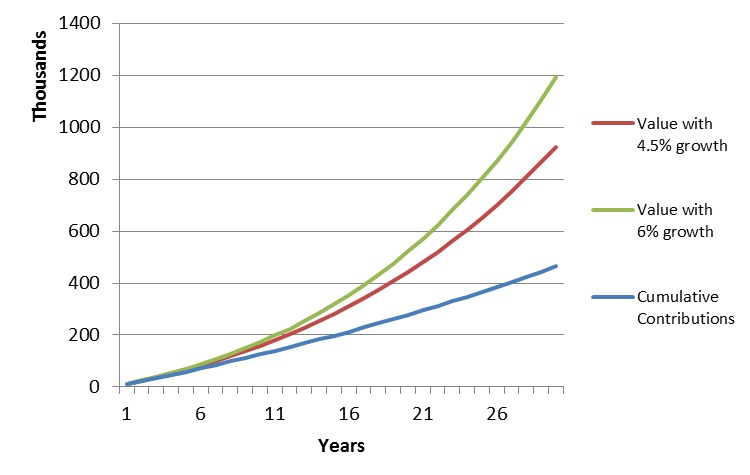

Fees can have a huge impact

Here’s a simple example. Let’s say you and your partner start saving in Tax Free Savings Accounts (TFSAs) at the beginning of 2017 and have a 30 year time horizon. Further, let’s say that contribution limits continue to increase with inflation along the lines of current TFSA rules and you’re fortunate and diligent enough to contribute the maximum each year. Assuming a 6% return you’d have nearly $1.2 million by the end of the 30 year period! Folks, it’s the miracle that is compound interest! But it’s also the curse that makes the impact of fees so devastating. The chart shown at the top of this blog depict this stylized example illustrates the issue quite clearly:

If excessive fees mean you only earn 4.5% per year you’d have nearly $270,000 less in your pocket at the end of the 30 years. That is a ridiculous amount of money to give away in excessive fees! Put another way, by lowering your fees, your investment earnings would be almost 60% higher over the time period.

Of course lowering your fees is not as simple as dialing up your financial institution or advisor and saying, “I’d like lower fees please.” The options for lowering fees in Canada are less common and less well understood than in other countries. Ultimately you have to take responsibility for your financial well-being and educate yourself. The financial services industry has a strong vested interest in you not educating yourself. So please start by visiting the Investright.org website. If you want further reading material we have a list of 4 Sensible and Concise Books on Investing that we recommend.

Graham Bodel is the founder and director of a new fee-only financial planning and portfolio management firm based in Vancouver, BC., Chalten Fee-Only Advisors Ltd. This blog is republished with permission: the original ran on October 26th here.

Graham Bodel is the founder and director of a new fee-only financial planning and portfolio management firm based in Vancouver, BC., Chalten Fee-Only Advisors Ltd. This blog is republished with permission: the original ran on October 26th here.