My latest MoneySense Retired Money column has just been published. You can find it by clicking on the highlighted text here: Why “unretirement” may be the fate of so many Canadians.

Even before the Tariffs threats emerged under Trump 2.0, Canadian seniors were starting to find the economic uncertainty and rising living costs to be unmanageable. No surprise then that many seniors approaching Retirement Age are delaying their exit from the workforce.

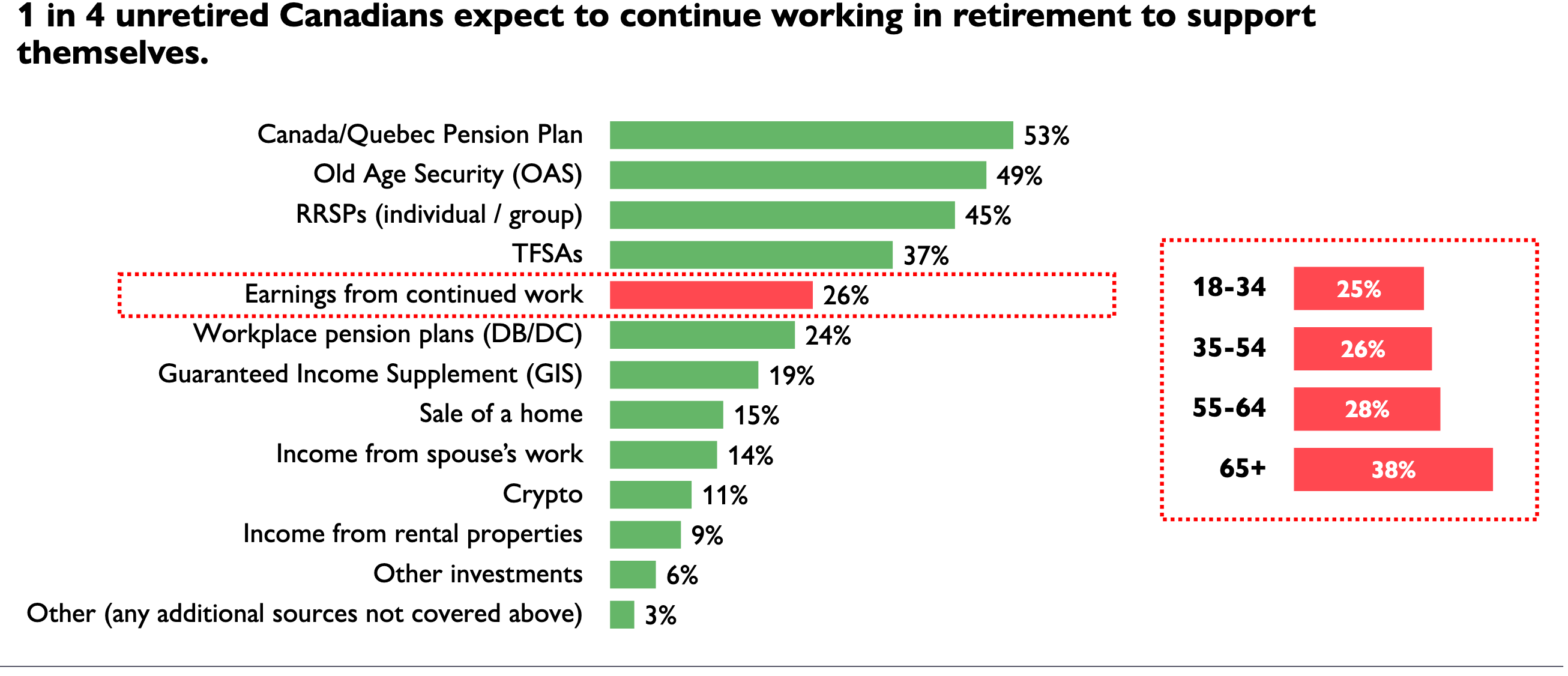

According to a report by HealthCare of Ontario Pension Plan, 28% of unretired Canadians aged 55-64 say they expect to continue working in retirement to support themselves financially. Here’s a screenshot from the HOOPP survey:

The Healthcare of Ontario Pension Plan (HOOPP) commissioned Abacus Data to conduct its sixth annual Canadian Retirement Survey in the spring of 2024. The latest survey finds “persistent high interest rates and a rising cost of living continue to have a significant negative impact on Canadians’ ability to save and manage the cost of daily life, threatening their retirement preparedness.” While all Canadians are struggling, “women and those closest to retirement are especially hard hit with lower savings and higher levels of financial stress.”

While most Canadians are struggling to save amidst a high cost of living, HOOPP finds women are particularly affected. Half (49%) of all Canadian women have less than $5,000 in savings and almost a third (28%) have no savings (compared to 33% and 17% of men, respectively), similar to the 2023 results

The MoneySense column also looks at more recent Retirement surveys that also reveal anxiety about rising costs of living. One is from Bloom Finance Co. Ltd., conducted by founder Ben McCabe after Trump’s Tariffs started to kick in this year.

A Bloom study conducted with Angus Reid found 46% of Canadians thinking of working part-time in Retirement. That’s in line with a Fidelity survey in 2024 that found half of Canadians plan to delay Retirement. According to the Bloom Report [in March 2024], 67% of Canadian homeowners over 55 were concerned their savings would not sustain their quality of life through retirement. Only 29% considered downsizing or alternative living situations to access their home equity earlier than expected. 59% of the same cohort agreed accessing micro-amounts of their home’s equity would help maintain their desired living standard.

The Trump Tariff war won’t improve the situation. Earlier this month, Bloom surveyed a small sample of younger seniors aged 60 to 64 about the impact of Tariffs; this cohort was the most concerned about their retirement prospects. 61% of that group felt they would need at least $20,000 in “buffer funds” this year in order to feel more financially secure. “Those who didn’t have the luxury of disposable income through their careers that could have been allocated to building sizeable investment portfolios don’t have the ability to draw on that as a meaningful contributor to their retirement income.”

The column offers the perspective of what financial advisors can do about this.

“With this type of uncertainty and a lack of alternative financial resources, the average Canadian has no choice but to continue to work,” says Matthew Ardrey, Portfolio Manager & Senior Financial Planner for TriDelta Private Wealth, “Additionally, it can be very difficult to find the money to save for the future when one is struggling to pay for today.”

Obviously, the more time before retirement looms, the easier it is to improve your situation. “Course correction is always easier from farther away,” Ardrey says, “The more time you have the less of a sharp turn you need to make.” You can create a budget to understand your inflows and outflows. Look for some discretionary expenses that can be reduced or perhaps a way to increase income. After that, try to move into a forced savings program.

Much like the pension contributions coming off of a pay cheque, take a portion of each pay and save it for your future. “Take advantage of registered accounts. TFSAs are not only for the wealthy. They are great investment accounts for the lower income Canadian as well. With tax refunds from RRSPs being limited at lower income levels, the TFSA can make more sense. Also, withdrawals in retirement are tax free, so it does not affect income-tested benefits like GIS.

Thank you for the article.