By Dina Ting, CFA, Franklin Templeton ETFs

(Sponsor Blog)

For decades, public markets were where companies grew up. Investors could watch young firms move from small-capitalization (cap) to mid-cap level and, for the rare few, into the ranks of the largest companies in the world. That journey today happens increasingly in private markets. We’re seeing now that by the time some companies list, they can seem to arrive already fully formed.

This shift is testing index construction. The impending listings from the likes of SpaceX, OpenAI and Anthropic have prompted index providers to revisit how quickly very large companies making initial public offerings (IPOs) should enter major benchmarks. Some index providers, including FTSE Russell and Nasdaq, have been racing to ensure benchmarks can capture the next generation of large public listings. Others, including S&P Dow Jones Indices, have preferred to keep established guardrails in place, maintaining a more deliberate approach to eligibility and inclusion.

In our view, this diversity of approaches is healthy. Index providers are trying to balance two important goals: reflecting the investable market as it evolves, while maintaining liquidity, stability and transparent rules. There is no single correct answer. A benchmark that moves too slowly may miss important changes in the economy. A benchmark that moves too quickly may expose investors to companies before trading history, float and fundamentals are well established.

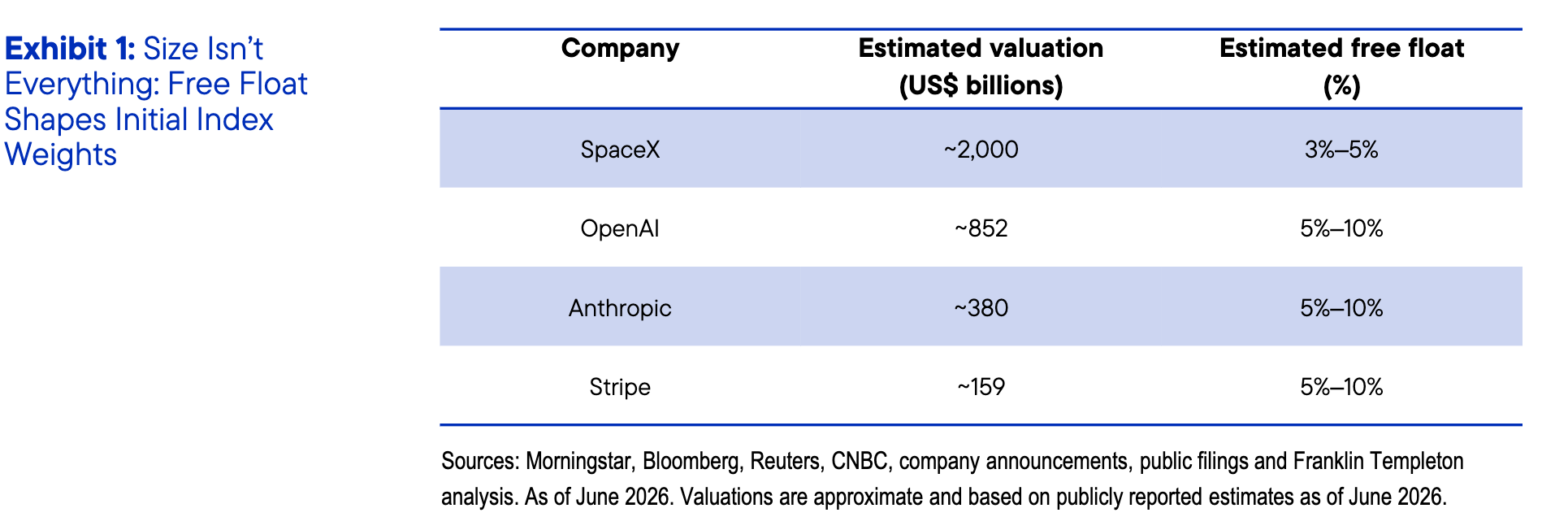

An overlooked aspect of benchmark construction is that headline valuations and index weights are not the same thing. Most major equity indexes rely on free-float-adjusted market capitalization, which means they consider the shares actually available for public trading. FTSE Russell’s own preliminary analysis of SpaceX assumed a total market capitalization of US$1.5 trillion but available market capitalization of about US$70 billion, producing estimated weights of only 0.11% in the Russell 1000 Index and 0.08% in the FTSE GEIS All-World Developed Index.1

A company may dominate headlines yet enter a broad index with a relatively modest initial footprint. Over time, lockup restrictions — which typically prevent founders, employees and early investors from selling shares immediately after an IPO — expire, allowing more shares to enter the public market and potentially increasing the company’s index weight.

Another question investors may not have considered is whether these listings automatically make indexes more growth oriented. At first glance, the answer might seem like a no-brainer. Many of these companies operate in areas such as artificial intelligence (AI), aerospace and cloud infrastructure. Yet index construction is often more nuanced than headlines suggest.

FTSE Russell’s treatment illustrates this. Fast-entry IPOs have generally inherited the style characteristics of their assigned subsector until company fundamentals become available. However, the index provider has also acknowledged that relying solely on industry averages could create what it calls “market misrepresentation,” leaving room for alternative treatment in certain cases. For SpaceX, FTSE’s preliminary classification pointed to telecommunications, where the subsector average was 18% growth and 82% value.2

That may surprise investors who instinctively view anything rocket-fueled as growth. But it is a useful reminder: Index investing is rules-based, not headline-based. Style indexes do not simply ask whether a company feels innovative. They evaluate characteristics such as valuation, earnings, growth metrics and industry classification. As more mature private-market companies list, some may challenge traditional style frameworks.

This is where broader portfolio implications emerge. Broad-market index ETFs remain efficient, tactical tools for gaining diversified equity exposure, and country or style ETFs can help investors express more targeted views. But indexes are not static. New companies enter, sector weights shift, float changes, classifications evolve and concentrations emerge. Index exposure is therefore not necessarily something investors should set and forget.

We believe the next wave of large public listings will make “know what you own” more important, not less. The IPO may grab headlines. The lasting story may be how these companies reshape benchmark exposure over time.

Dina Ting, CFA, is senior vice president and head of Global Index Portfolio Management at Franklin Templeton. Her team is responsible for managing Franklin Templeton’s suite of index-based strategies, including ETFs. Prior to joining the firm in 2015, Ms. Ting spent nearly a decade at BlackRock, where she led the Institutional Emerging Markets team that managed over 70 global equity portfolios for clients worldwide. She also managed a multitude of iShares ETFs covering smart beta, global real estate, sector-based and emerging market strategies. In 2019, Ms. Ting was named one of Money Management Executive’s Top Women in Asset Management and in 2018, she was recognized by the San Francisco Business Times as one of the Most Influential Women in Bay Area Business. She earned a master of science in management science and engineering from Stanford University and holds a bachelor of science degree in industrial engineering from Purdue University. She is a Chartered Financial Analyst (CFA) charterholder.

Endnotes

- Source: FTSE Russell. Estimated weights as of June 2026. The Russell 1000 Index measures the performance of the large-cap segment of the US equity universe. FTSE GEIS All-World Developed Index is a market-capitalization-weighted benchmark representing the performance of large and mid-cap companies in developed markets.

- Source: FTSE Russell. As of June 2026.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

Large-capitalization companies may fall out of favor with investors based on market and economic conditions.

Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks.

Investments in privately held companies present certain challenges and involve incremental risks as opposed to investments in public companies, such as dealing with the lack of available information about these companies as well as their general lack of liquidity.

Performance of the portfolio may vary significantly from the performance of an index, as a result of transaction costs, expenses and other factors.

There can be no assurance that the underlying index’s calculation methodology or sources of information will provide an accurate assessment of included issuers or that the included issuers will provide the portfolio with the market exposure it seeks.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation

to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced,

distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may

change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from

other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact

regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market

or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not

get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All

investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that

connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and

Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that

Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and

may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a

recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient

basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon

the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG”

as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors

as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on

availability of products and services in your jurisdiction.

Canada: Issued by Franklin Templeton Investments Corp., 200 King Street West, Suite 1400 Toronto, ON, M5H3T4, Fax: (416) 364-1163, (800) 387-0830,

www.franklintempleton.ca.