Life insurance is a must if you have a spouse or children who depend on your income to get by. But asking a life insurance agent if you need more life insurance is like asking a barber if you need a haircut. Of course the answer is going to be ‘yes’. Indeed, the life insurance business has a long history of commission-hungry agents pushing expensive policies onto consumers who would be better off with simple term coverage.

Life insurance is a must if you have a spouse or children who depend on your income to get by. But asking a life insurance agent if you need more life insurance is like asking a barber if you need a haircut. Of course the answer is going to be ‘yes’. Indeed, the life insurance business has a long history of commission-hungry agents pushing expensive policies onto consumers who would be better off with simple term coverage.

While you should view any life insurance discussion with a skeptical eye, the reality is that many people are severely under-insured. Most group insurance policies at your workplace only provide coverage for one or two times your annual salary. You might need 10 or 15 times that amount if you have a young family at home.

The other challenge with group life insurance coverage is that it’s not transferable: you can’t take it with you when you leave your employer.

Ending my Group Coverage

That’s the situation I find myself in right now. The group coverage I have with my employer is quite generous at 2.5 times salary. They also offer the voluntary option to add up to an additional $500,000 in coverage at favourable rates (each $100,000 in coverage cost just $4.50 per month). I took the maximum optional coverage and increased my overall life insurance coverage to approximately $700,000. My total premiums cost less than $35 per month.

The rational side of me knew that I’d eventually leave my job and would need to take out a private insurance policy. But I didn’t get around to it. Then I quit my job.

Now I’m scrambling to get an insurance policy in place before the end of the year to avoid any lapse in coverage. First, I performed a life insurance needs analysis. A lot has changed in 10 years. My kids are older (11 and 8 next year). We have a lot more money saved. We have less debt. Do we still need $700,000 in coverage? Do we need more?

A needs analysis considers things like your survivor’s income and spending needs, years of income replacement, personal and household debt, children’s education, non-registered assets, and final expenses. My analysis found that a 15 year term with $600,000 in coverage would be sufficient.

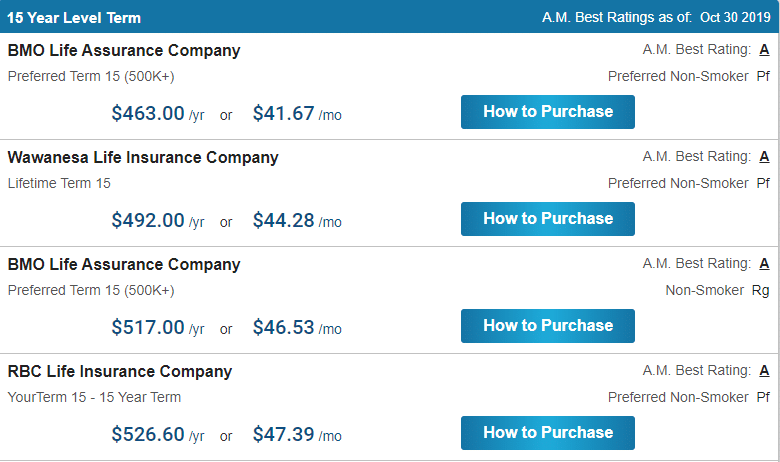

Term Life Insurance quotes

I shopped around for term life insurance quotes using the website term4sale.ca (no affiliation).

I like the site because it offers unbiased comparisons from various life insurance providers, and I can obtain a quote within seconds (without entering an email address or phone number and risk being hunted down by commission-hungry agents).

Armed with a range of quotes from various insurers, I called my long-time auto and home insurance broker to see what he could do for me. He asked about the quotes and so I shared where I found them. He said his quotes might vary somewhat because the insurer will do a more rigorous interview and examination, which makes sense. After all, I filled out a quick five-question form online to arrive at those other quotes.

We settled on one insurer who offered the 15-year, $600,000 term life policy at a price that seemed reasonable (less than $45/month). They set up a 20-minute phone interview, and then arranged to have a nurse visit my home to take blood and urine samples, and to take my blood pressure. Definitely more thorough than an online quote!

Final thoughts

As I await the results to see if 1) I qualify for coverage, and 2) I received an “excellent” health designation to qualify for the lowest premiums, I can’t help but kick myself for making such a rookie personal finance mistake.

Topping up my life insurance with my group coverage provider was the easiest and cheapest option available to me at the time. But in hindsight I should have taken out a private insurance policy much earlier and held it in tandem with my workplace coverage.

Not that I could have predicted I’d be leaving my employment after 10 years and going to work for myself. But the lesson here is that insurance is cheap and plentiful when you’re young and healthy, so you might as well buy as much as you need through a private policy – just in case. After all, isn’t that what insurance is for?

In addition to running the Boomer & Echo website, Robb Engen is a fee-only financial planner. This article originally ran on his site on Nov. 20, 2019 and is republished here with his permission.

In addition to running the Boomer & Echo website, Robb Engen is a fee-only financial planner. This article originally ran on his site on Nov. 20, 2019 and is republished here with his permission.

I understand that everybody’s situation is different and should be evaluated independently, but there’s no way that most people should have anywhere near this much insurance.

$45/month compounding at 5% over 15 years is over $12,000 of forsaken income, and those are even after-tax dollars. The tl;dr is that is a lot of money to spend on a catastrophic fantasy, and at least in my opinion reflects a really poor evaluation of risk.

This is a great reminder, especially about not relying only on group coverage. When I was comparing options outside work, I found that getting clear term life insurance quotes

helped a lot in figuring out how much coverage actually made sense for my family without being pushed into expensive permanent policies. Shopping around really makes the difference.