The majority of Canadians are afraid they’ll run out of money in Retirement, especially women and young people, according to a survey released Wednesday morning by the Canada Pension Plan Investment Board (CPPIB).

The 2025 CPPIB Retirement Survey (for Financial Literacy Month) says 59% of all Canadians are afraid of running out of money during Retirement, with the percentage jumping to 63% for women, compared to just 55% of men. It also found a whopping two thirds (66%) of Canadians aged 28 to 44 share the same fear. As the CPPIB graphic below illustrates, those who have a financial plan are slightly less worried.

As you’d expect the CPPIB to point out, the Canada Pension Plan (CPP) helps protect retired Canadians from this risk: as it says above, CPP “benefits are payable as long as you live and [are] indexed to inflation.”

Indeed, CPP and the other main government retirement income program, Old Age Security, are both valuable sources of inflation-indexed retirement income. CPP is available as early as age 60 and OAS at 65 but a staple of Canadian personal finance commentary is that the longer you wait to receive benefits, the higher the benefits will be. In the best of all worlds, you’d wait until 70 for both programs to start paying out, even if you have to keep working longer and/or start withdrawing money from your RRSP before it’s mandated at age 71/72. (While the CPPIB doesn’t mention it, retirees with no other savings may also benefit from the Guaranteed Income Supplement to the OAS: and the GIS is tax-free.)

The second graphic reproduced below is less straight-forward: it appears to present various excuses for delaying the creation of a proper financial plan to help get to Retirement. Roughly half of younger Canadians cite their need to advance their careers and make more money, and to buy their first home as priorities.

While it’s true that if nothing else, the future arrival of CPP and OAS benefits should put minds partially at ease about covering off basic Retirement expenses, it seems to me pretty obvious that at least for those who lack a generous employer-sponsored pension plan (ideally an inflation-indexed Defined Benefit pension), that it will be necessary to maximize savings in RRSPs and TFSAs as soon as possible.

Because of the Time Value of Money and the magic of compounding investment returns (especially when tax-deferred in RRSPs and TFSAs), the sooner you start saving in these vehicles the better. There’s no excuse not to make RRSP contributions from the get-go, ideally as soon as you land your first real job, since it reduces your income tax. Yes, decades from now when RRSPs become RRIFs you’ll have to pay some tax on the ultimate withdrawals, but that’s more than made up by the tax-deferred investment growth.

It does make sense to pay off mortgage debt (not to mention high-interest credit-card debt or auto loans) before contributing to TFSAs, since few investments in TFSAs can match the returns of paying down high levels of debt. But the moment those debts are paid off you should start maxing out ideally $7,000 a year in TFSA contributions. If you do this while you’re still feeling the sting of mortgage payments, you may find that once those payments are gone you can redirect them to TFSA contributions and/or higher RRSP contributions.

The foundation of Financial Independence

It’s not for nothing that in my financial novel, Findependence Day, I say “the foundation of Financial Independence is a paid-for home.” It’s a big moment when you no longer have to pay rent to some landlord, and to worry that he or she will keep hiking that rent as the years go by. In Retirement, you definitely will sleep easier if your home is paid for.

As for the temptation to procrastinate on planning Retirement, I suggest those still worried about their careers and getting a foothold on the housing ladder should at least seek the advice of older and wiser people who have already gone down this path. If you are investing in stocks through a stock broker or in mutual funds or ETFs through a financial advisor, you’re already paying for some advice anyway. Some may charge extra for a one-time financial plan, which are also offered by fee-only financial planners. I’d consider any such costs to be an investment in your own future, and that of your spouse (if applicable) and eventual family.

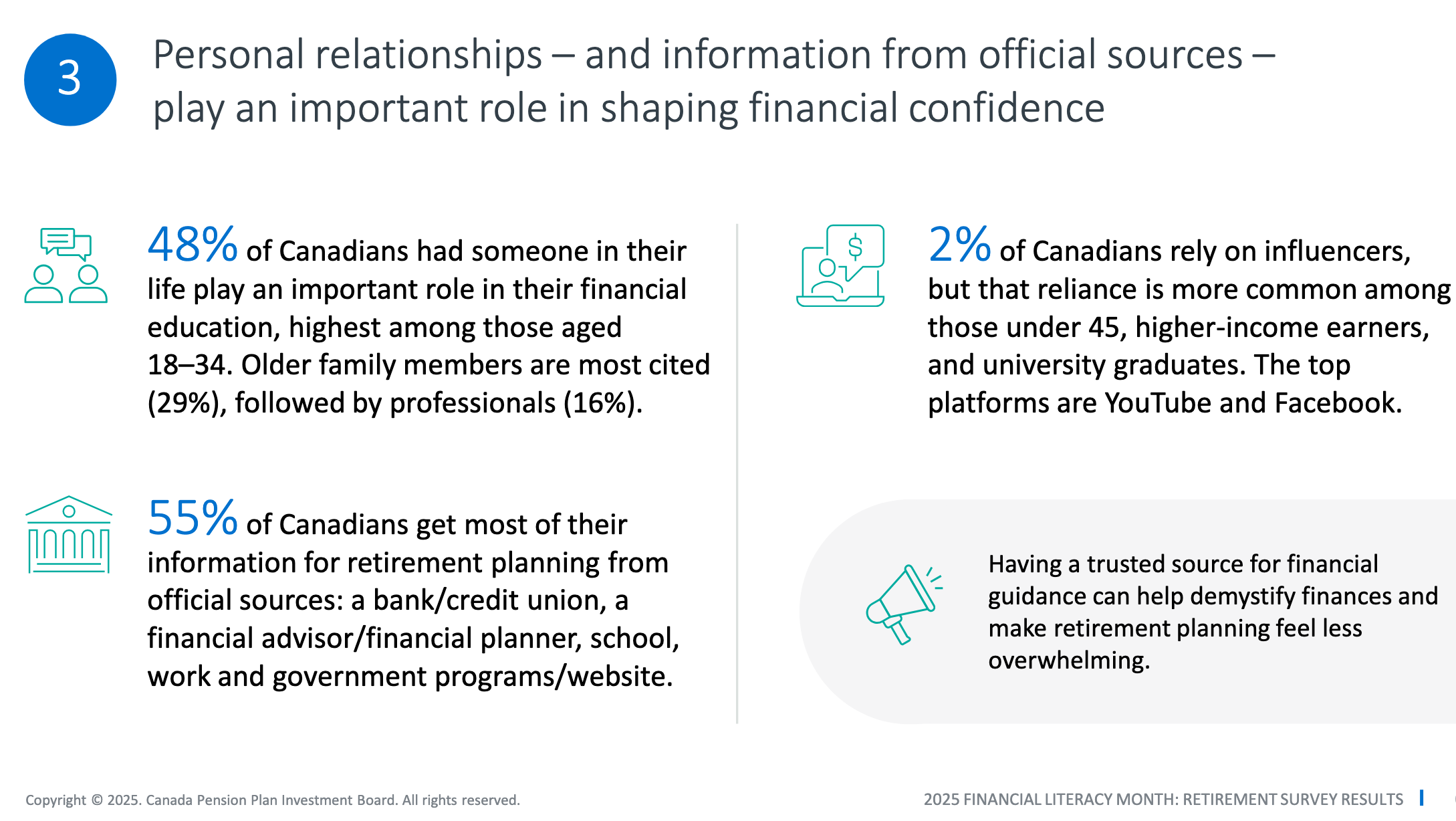

The graphic below illustrates the value of such personal relationships as well as of information from official information sources like banks, credit unions and government programs or websites.

If you’re reading this blog and looking for new sources of information on Retirement, you might be interested in tapping into a new community of (mostly) retired investors: the Retirement Club, of which I am a member. The link is to a blog I wrote about the club for Findependence Hub this summer.  The members are mostly keen do-it-yourself investors with a strong interest in investing and all things Retirement. A recent session focused on annuities, which will interest those who don’t have a generous DB pension. Another featured an executive from the Purpose Longevity Fund, which prompted me to subsequently purchase for a chunk of my own RRIF account.

The members are mostly keen do-it-yourself investors with a strong interest in investing and all things Retirement. A recent session focused on annuities, which will interest those who don’t have a generous DB pension. Another featured an executive from the Purpose Longevity Fund, which prompted me to subsequently purchase for a chunk of my own RRIF account.

The CPPIB’s online survey was conducted by Innovative Research Group between August 25 and September 4, 2025, with a sample of 5,183 Canadians (outside of Quebec), 18 years or older.