By Aman Raina, SageInvestors.ca

By Aman Raina, SageInvestors.ca

Special to the Financial Independence Hub

NOTE: This review was initially undertaken using data compiled as of January 30, 2020, which marked the 5-year anniversary during which the portfolio was active but prior to the severe market turbulence that occurred in February and March 2020. As it became apparent that the market pullback was becoming an epic meltdown, additional data was compiled and included into the review.

Five years ago I embarked on a personal experiment. I was having a hard time getting any insights on the effectiveness of a new investment services that was shaking the ground at the time in 2015.

Known or labeled as Robo Advisors, these new wealth management companies offered services to invest on behalf of others using an online platform and a combination of algorithms and computer coding to buy and sell specific investments and manage portfolios. Five years ago these firms were just stepping into the investing consciousness, but since then they have mushroomed and even traditional investment companies are now offering some flavor of online investment management services.

It all seemed quite appealing; however, there was one thing that many marketing materials, blogs, and mainstream media were avoiding … do these types of services make money for investors? Is this the type of service that would successfully bring more people, who naturally feel intimidated and frustrated by the whole investing concept into the investing domain?

Since no robo advisor company back then was interested in disclosing their performance (they still avoid it) other than citing research that their low cost/passive oriented strategy is superior, I decided five years ago to try an experiment to get some more insights that did not involve boilerplate marketing speak. I set up an account with one of the “large” Robo Adviser firms and invested $5000 of my own money into it.

My goal was to go through the process and blog about my experience using the service, how the ROBO went about making decisions and how it managed my portfolio, and more importantly, the results. I’ve always said that we need a good five years to really get a handle on how effective these services are compared to traditional wealth management services. Well, I just crossed the five-year mark of my ROBO journey, so let’s check back in and take a look at how it’s been doing. I’ve also said that I would reserve my opinions about this service until we reached that five-year threshold. Well here we are and I’m ready to unload my takes.

2019 was an epic year for stocks. US major stock indexes were up just over 30 per cent on the year. Fantastic returns. Hopefully my ROBO got a good piece of that action.

Performance

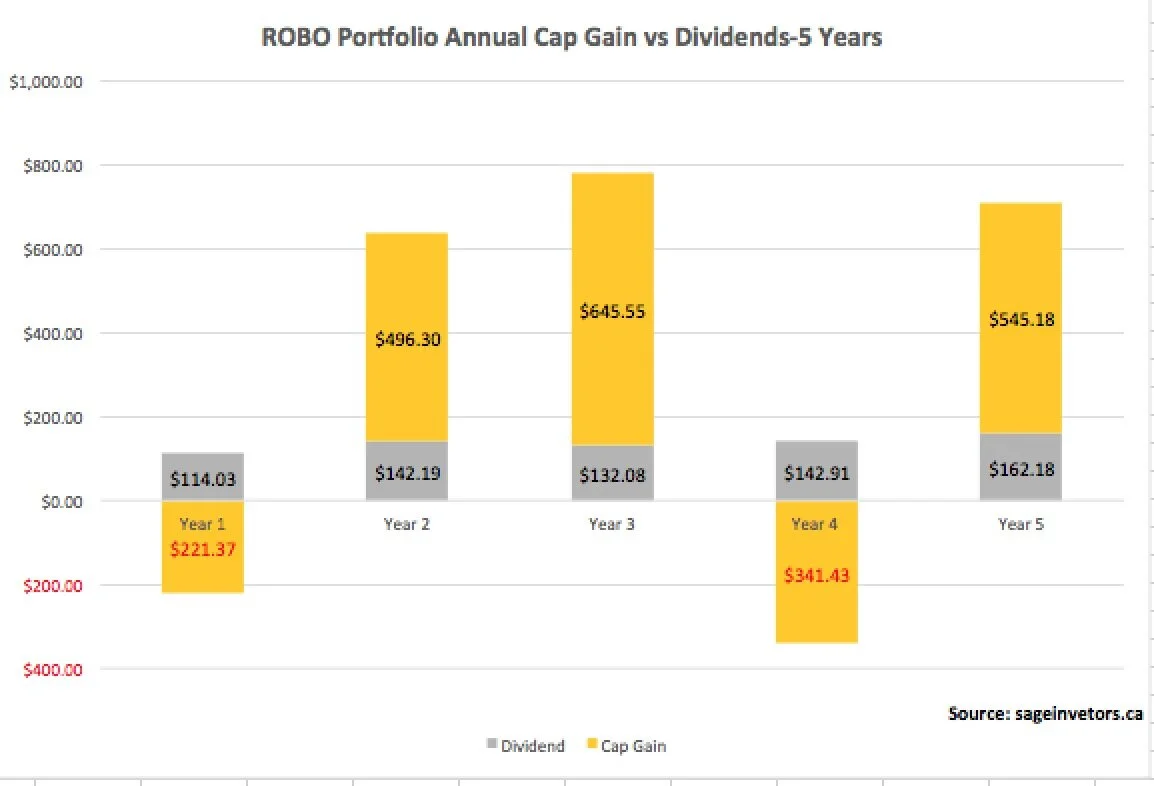

Overall, my ROBO portfolio posted a solid year. The portfolio was up 11.6 per cent year over year, a nice rebound from the previous year where it lost 2.1 per cent. Over the 5 years, the portfolio generated positive returns in three of the 5 years, and posted double-digit returns in those three years. The portfolio increased by $707, of which $162 came from dividend income while the remaining $545 came from capital gains. Over the year period, the ROBO portfolio increased from my initial $5000 to $6817, a cumulative return of 36 per cent. Of the $1817 increase, 1/3 was from dividends while the remainders was from capital gains. The portfolio continued to benefit from higher concentration of US and Canadian equities, which again hit it out of the park the past year.

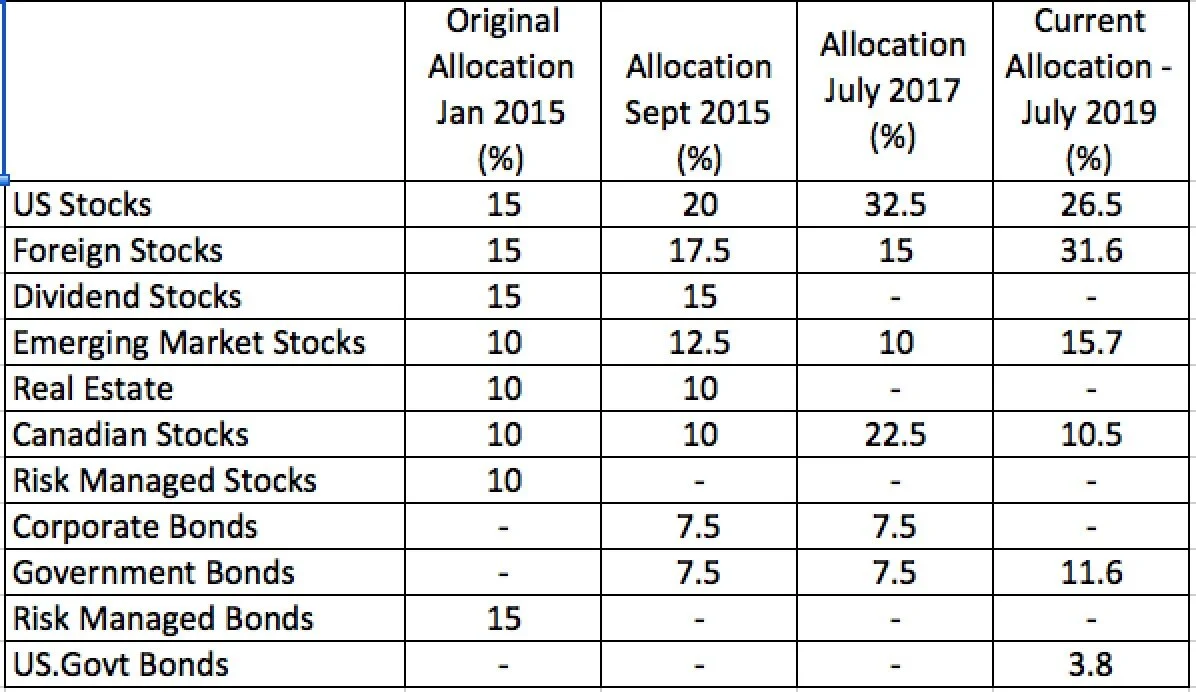

Below is the breakdown of the portfolio. Five years ago when I set up the account I answered a series of questions about my financial literacy and risk tolerance. ROBO took my responses and crafted a portfolio that it felt was compatible with my profile.

As I am pretty experienced with investing and have a long-term investment horizon, ROBO determined that a portfolio mix of 85 per cent stocks and 15 per cent bonds would work for me. Over the five years, it has consistently retained this basic weighting. From there ROBO carved out allocations to a variety of equity assets using ETFs to provide the appropriate exposure. Below is the most recent allocation and performance.

ROBO Portfolio: Asset Allocation – January 30, 2020

In my July 2019 mid-year review, I itemized the changes in the asset allocation of the ROBO portfolio. The ROBO has significantly adjusted the weightings on the various asset classes and also rotated out of several ETFs. Some of these decisions made sense (e.g. reducing the Canadian/US equity weightings as they almost made up half the portfolio). Since then the ROBO has not made any significant changes. As I commented in the mid-year report, the moves marked the 3rd significant change in the makeup of the portfolio over the 5-year period. The portfolio has reduced weightings in core ETFs such as the Vanguard Total Stock Market and iShares S&P/TSX Composite and introduced more active oriented ETFs to diversify the portfolio.

Five years ago, the portfolio was created with 8 ETFs, which had a more actively managed investment philosophy and specialized in niche assets such as dividend equities, risk-managed equities, and real estate, which was surprising to me at the time given the value proposition that my ROBO service was pushing was low-cost, passively index oriented ETFs. Over time the ROBO moved away from these speciality ETFs and moved into more appropriate broad based index oriented ETFs. When the portfolio was created five years ago, the weightings were more evenly distributed across the asset classes, but over time they weightings shifted to emphasize Canadian and US based equities. While I was critical on the overweight, clearly the results show that it was a positive approach.

Fees

The ROBO model is much more transparent in terms of fees it charges itself as well as the fees the individual ETFs charge, which is good to see. In the past year, I paid directly to my ROBO service $39.54, which was slightly higher than previous year where I paid my ROBO a total of $37.36, which was much higher than the $24.72 in fees in year 3. The costs represent 0.58% of the portfolio. Over the 5 years, I paid my ROBO $112.56 to manage my account and generate $1817.

These costs do not include the Management Expense Ratio that is charged by the various ETFs. Last year the MER was approximately 0.10 per cent. When you add in the ROBO’s costs the total cost came in at 0.68% of the portfolio, which is slightly lower than the previous year where it was 0.70%.

When I set up the account five years ago, the ROBO service did not charge fees for portfolios $5000 and under. A couple of years ago they changed their fee structure and according to their website now charge 0.5% on the first $100,000. Somehow though I’m paying 0.68% in costs, which makes me wonder where the extra 18 basis points came from?

The fees are still much lower than what you would pay for a portfolio of mutual funds which would charge you well over 1 percent and higher.

Breaking News!!! Robo performance during the Covid Market Meltdown

In late February and March, the markets experienced a generational meltdown. The COVID-19 global pandemic, forced entire swaths of the world economy to shutdown to contain the rapid spread. Stock markets tanked falling 30-40 per cent … and as of this writing, the damage is still ongoing.

Even though I cashed out my ROBO portfolio just before the stock prices cratered (COVID did not factor in to the decision), I was able to go back and update the portfolio numbers to reflect what my portfolio would have looked like during the market meltdown. I used closing prices as of March 23, 2020.

Oh dear.

My portfolio would have gone from $6,817 on January 30, 2020 to $4,602 as of March 23, 2020, a drop of 32 per cent. In literally a couple of weeks, I went from being up almost 40 per cent to losing 8 per cent over the 5-year period.

Unbelievable.

Market crashes come at you fast.

Even though I had cashed out before all this went down, I felt quite rattled by the violent nature of the pullback. It was a $5,000 investment. I imagined if I had put a much larger amount. That would be rough one to deal with, considering how tame the portfolio has behaved over the past 5 years, to see it crash with a thud.

The nature of the drop was consistent with level of drops in the broader markets, which reinforces my observation that during good times, the portfolio participates nicely on rallies, but given the passive nature of the ETFs in the porfolio, it is not constructed to dampen the blow from a violent market crash. That’s not the ROBO portfolio’s fault. It’s designed with a mandate to mirror the returns of the market. Ironically the ROBO incorporated several ETFs that invest in low-volatility stocks, to dampen it from these type of shocks. It didn’t make a difference. When a market crashes, everything goes down.

The ROBO investing ideology revolves around a passive, buy-and-hold methodology. Looking at the results of this 5-year window, the end result is now not great; however, if we expanded the window to the last 10 years, a period where the S&P500 almost tripled, the recent body-blow to the portfolio would amount to a flesh wound.

This result would have happened whether you used a ROBO service, managed the portfolio yourself, or outsourced it someone else to manage it. I don’t think it changes my viewpoint in terms of whether this ROBO service is better or worse. Whatever path you take on your investing journey, you need to always be mindful of risk and mindful that you will enter periods where you will lose money. How you manage these periods and how you behave is more critical regardless if a computer is managing your money. Your consideration of what path you take will involve your willingness to educate yourself about the mechanical and behavioural aspects of investing, your willingness to engage in the process and what stage of our life you’re in.

I hope you found these observations helpful to you and will aid you to make decisions that are appropriate for you. I have learned a great deal from this exercise.

Thanks for following along my robo advisor journey. Best of luck.

Aman Raina, MBA is an Investment Coach and Founder of Sage Investors. Aman teaches new and experienced investors how to make educated and successful investment decisions so they can achieve financial freedom in their lives with confidence. Follow Aman on Twitter and Facebook. This blog was published on March 25, 2020 and is reproduced here with permission.

Aman Raina, MBA is an Investment Coach and Founder of Sage Investors. Aman teaches new and experienced investors how to make educated and successful investment decisions so they can achieve financial freedom in their lives with confidence. Follow Aman on Twitter and Facebook. This blog was published on March 25, 2020 and is reproduced here with permission.

Thanks for the great update – including the crash update. Great stuff. While there are passive pieces to this portfolio, this is without a doubt an active portfolio. With the number of changes in five years and the products and allocations selected, this is true active management. On the equity side, a simple VT (or VXC) with maybe some XIC for home bias would be all that’s needed on the equity side to truly capture market returns. And one aggregate bond ETF (again maybe a second to add some CAD bias). That’s it. But the challenge for any advisor that truly believes in indexing – digital or otherwise – is that it’s a tough sell to charge people fees to simply buy, hold, and occasionally rebalance a 2-3 ETF portfolio. And yet that’s all you should have if truly the goal is to capture returns.

https://www.investmentexecutive.com/in-depth_/magazines/keeping-it-simple/