• Gold is shining again; prices have surged to record highs this year and are forecast to climb further.

• Central banks are buying at a record pace, while investors seek protection from rising debt and currency debasement through gold ETFs.

• BMO’s gold ETF suite offers choice: ZGLD for stability, ZGD for growth, and ZJG for high-octane exposure.

Gold shines in 2025

By Erin Allen, Director, Online Distribution, BMO ETFs

(Sponsor Blog)

Gold’s reputation as an ancient store of value has rarely felt more modern.

The metal has been one of 2025’s standout performers among major asset classes, surging to record highs of around US$3,900 per ounce as of September 2025. The rally has been fueled by central bank buying, rising fiscal concerns, and investors seeking protection from a weakening U.S. dollar.

BMO Capital Markets recently lifted its gold price forecasts to an average of US$3,900 for the final quarter of 2025 and US$4,400 for 2026, reflecting what analysts describe as structural changes in the geopolitical and financial landscape¹.

The key driver: debt. With deficits in the U.S., Japan, and Europe ballooning, gold is increasingly being viewed not just as a safe haven, but as a strategic hedge against long-term currency debasement.

In this piece, we unpack what’s driving gold’s renewed strength, assess whether it’s sustainable, and outline ways investors can gain exposure through BMO ETFs from the physical metal itself to large and small-cap miners.

Central banks are quietly building reserves

One of the biggest tailwinds for gold has been record levels of central bank buying.

According to Reuters, central banks now hold 36,000 tonnes of gold, having added more than 1,000 tonnes annually for three consecutive years². This surge reflects a broad reassessment of what constitutes a safe asset.

Geopolitical instability and questions over the long-term stability of U.S. Treasuries have prompted central banks to diversify reserves. Gold has even overtaken the euro to become the second-largest global reserve asset, and for the first time since 1996, represents a larger share of reserves than Treasuries².

Chart 1: Foreign central banks hold more gold than Treasuries

Gold fell from 75% to 15% of reserves; Treasuries rose and surpassed gold holdings around 2023 for central banks.

The World Gold Council notes that while emerging markets typically hold 5–25% of their reserves in gold, developed economies hold more than 70%³. This steady official-sector accumulation underscores the global shift to tangible assets amid growing fiscal and political uncertainty.

Trade tensions and currency debasement fears

Gold’s strength also reflects what Bloomberg calls the “debasement trade.” As government debt piles up and fiscal discipline erodes, investors are moving out of major currencies and into alternative stores of value such as gold, silver, and Bitcoin⁴.

The U.S. dollar is down roughly 8% year-to-date, while gold continues to post record highs. Bloomberg notes that the current cycle echoes previous bouts of U.S. dollar weakness following the global financial crisis and periods of aggressive monetary easing⁴.

As George Heppel, Vice President, Commodity Research at BMO Capital Markets, explains, both cyclical and structural forces are converging¹:

“What we’re really seeing this year is the combination of a short-term thesis and a long-term thesis for holding gold, which has created a perfect storm for the metal. And naturally all of this increases concerns around sticky or growing inflation and the potential for negative real rates next year, which makes gold an attractive asset to be holding as an inflation hedge,” he says.

With U.S. debt climbing and political gridlock persisting, investors have reason to question the durability of fiat currencies. Gold, with no counterparty risk and a finite supply, has reasserted its role as a monetary anchor.

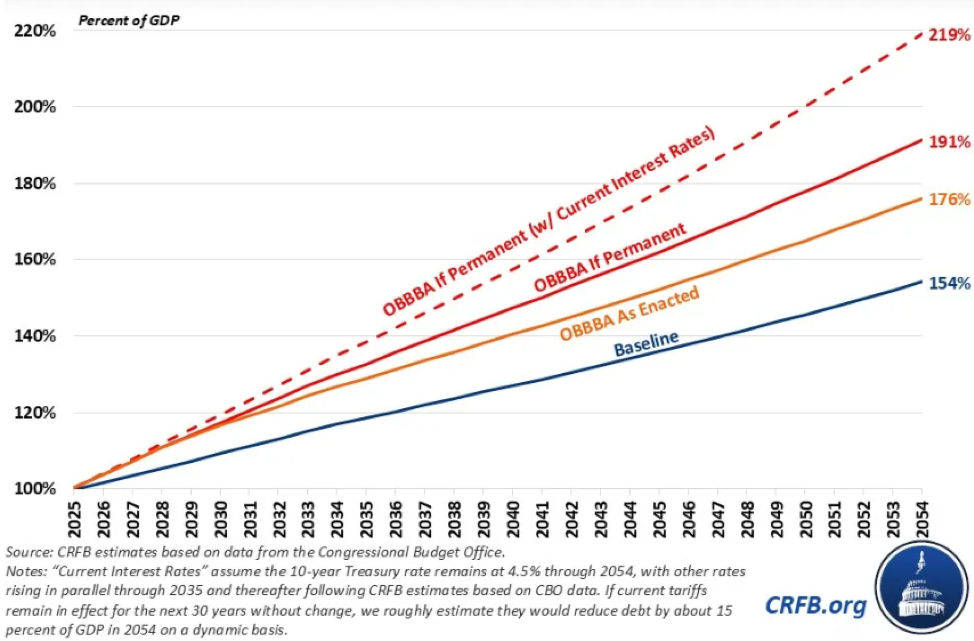

According to the Congressional Budget Office (CBO), the recently passed One Big Beautiful Bill Act (OBBBA) – also known as the “Trump tax cuts” – will add an estimated US$19 trillion to U.S. debt over 30 years as written, or US$32 trillion if made permanent⁵.

“The passage of OBBBA will put tremendous pressure on the nation’s fiscal and economic health. Layered onto an already unsustainable outlook, the new law increases the risk of higher interest costs, slower growth, volatile markets, and reduced capacity to respond to future crises or invest in national priorities,” the CBO warned.

Chart 2: Debt soars under OBBBA

Projected U.S. debt-to-GDP rises sharply from 2025 to 2054, peaking at 219% under the highest scenario in the chart.

All logos and trademarks of other companies and/or organizations are the property of those respective companies and/or organizations.

Gold ETF demand surges to near-record levels

While central banks are leading the charge, investors are not far behind.

According to ETF.com, global gold ETFs have attracted US$44 billion in inflows this year, equivalent to roughly 443 metric tonnes of the metal⁶. That puts 2025 on track to rival the record US$49.5 billion set in 2020: the strongest year ever for gold-backed funds. Canada alone saw over $1B flow into commodity ETFs, largely driven by gold, according to National Bank of Canada’s September flows report.

Gold ETFs have become the preferred way to access gold, offering liquidity, transparency, and simplicity: all without the complications of physical storage.

Investment banks turn bullish

Institutional sentiment has followed suit.

BMO analysts believe the gold market is undergoing profound structural change, driven by debt, inflation, and de-dollarization. The bank has raised its long-term gold-price assumption to US$3,000 per ounce, up from US$2,200, placing it near the top of sell-side consensus¹. Continue Reading…