By Zayla Saunders, BMO ETFs

(Sponsor Blog)

Markets are noisy right now. Between trade talks, shifting rate expectations and recession whispers, there’s no shortage of turbulence. That’s why low-volatility strategies are back in focus: and BMO’s lineup is standing out.

Not all low-vol ETFs are created equal. In fact, BMO’s low-volatility ETFs have been quietly dominating their corner of the market. Here’s what’s working with the approach and the key differentiators of the methodology.

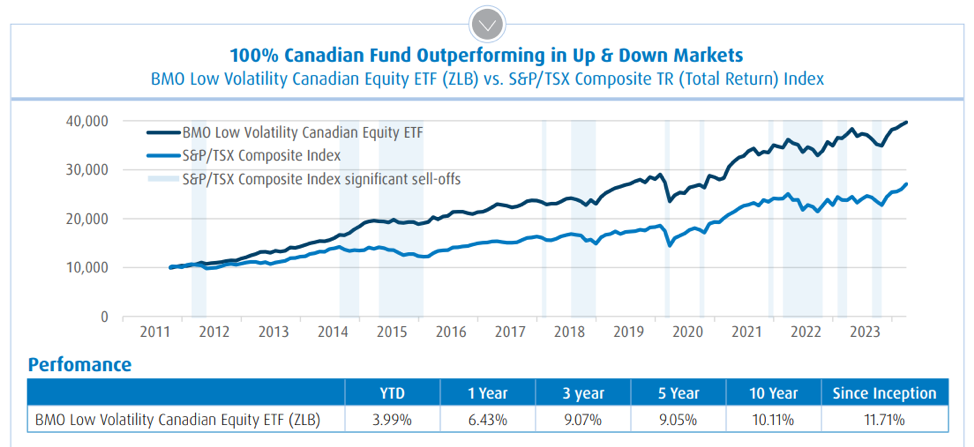

Source: Morningstar as of March 31, 2024 2

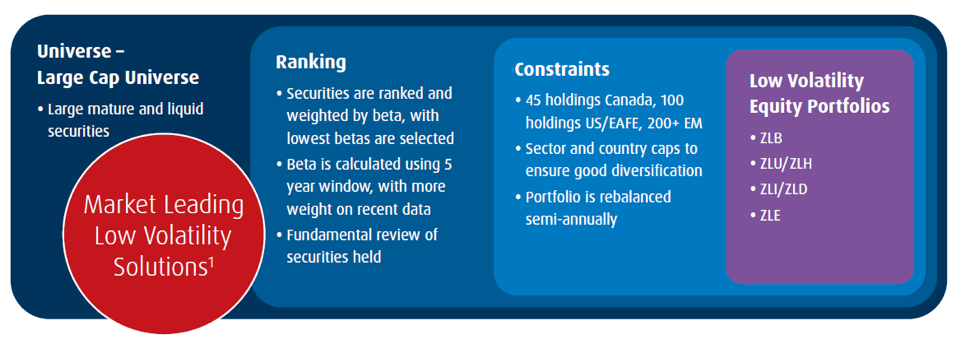

Smart, Targeted Methodology

BMO doesn’t just take the market and strip out the riskiest names. Its methodology is precise, practical, and time tested

Step 1: The Starting Point

BMO begins with a broad universe of stocks that are the largest and most liquid from a particular region — say, Canada or the U.S. — and then ranks them based on historical return volatility (also known as beta). Lower is better here.

Step 2: Ranking

Next, the securities are ranked and selected based on their beta, with lowest betas carrying the highest weight in the portfolio. Beta is calculated using 5-year window, with more weight on recent data. Then the team engages in a fundamental review of securities held.

Step 3: Sector Constraints

Unlike some low-vol strategies that end up extremely overweight in defensive sectors (hello, utilities and consumer staples), BMO imposes sector caps. Why? To ensure diversification and avoid concentration risk. That means that while there will be a tilt towards defensive sectors, you’re building a balanced, resilient portfolio.

The Burning Question: Why ‘Beta’?

Beta and Standard deviation are two of the most common ways to measure a fund’s volatility. The key difference is that beta measures a stock’s volatility relative to the market as a whole, while standard deviation measures the risk of individual stocks.

This is where BMO ETFs stands apart in their strategy: The BMO ETF Low Volatility Strategy uses beta as the primary investment selection and weighting criteria. By constructing ETFs with lower beta securities, the BMO ETF Low Volatility Strategy gives investors access to portfolios that are designed to provide growth while reducing exposure to market risk. Over the long term, low beta stocks may benefit from smaller declines during market corrections and still increase during advancing markets. Additionally, they tend to be more mature and provide higher dividend yield than the broad market.

Beta is a risk metric that measures an investment’s sensitivity to fluctuations in the broad market (market sensitivity). The broad market is assigned a beta value of 1.00, an investment with a beta less than 1.00 indicates the investment is less risky relative to the broad market.

So why now?

Low volatility has always had its place: particularly for long-term investors looking to stay invested through all market cycles, or those who tend to be more emotional around volatility in their portfolio. But right now, the case is even stronger: Continue Reading…