I’d gladly lose me to find you

I’d gladly give up all I have

To find you, I’d suffer anything and be glad

I’ll pay any price just to get you

I’d work all my life, and I wi

To win you, I’d stand naked, stoned and stabbed

I call that a bargain

The best I ever had

- Bargain, by The Who

By Noah Solomon

Special to Financial Independence Hub

Many investors could be forgiven for believing that U.S. stocks are a superior investment to their non-US counterparts. Since the global financial crisis, U.S. stocks have not merely outperformed those of other countries: they have trounced them. Over the past fifteen years, the S&P 500 outpaced other developed market equities by a cumulative 150%.

Notwithstanding this astounding outperformance, successful investing necessitates looking ahead. To assess the likelihood that U.S. stocks will continue to outperform, it is important to (1) analyze the drivers of their past outperformance, and (2) determine the future sustainability of these drivers.

Not as Exceptional as you might think

Over the past decade, U.S. companies have delivered stronger earnings growth than those in other countries. However, given the degree to which their share prices have outperformed, the magnitude of their excess earnings growth is far less than one might suspect. Over the past ten years, American company earnings have outpaced those of foreign companies by a meagre 3.8% on a cumulative basis. Moreover, this excess growth was concentrated in the first part of the decade, with U.S. companies growing their earnings at the same clip as their non-U.S. peers from 2020-2024.

Not only has U.S. earnings growth been undifferentiated over the past five years, but it has achieved this mediocrity due to the stellar growth of a small handful of mega-cap tech stocks. Between 2020-2024, the magnificent six (Tesla was not in the index at the end of 2019), which collectively represent a 32% weight in the S&P 500 Index, grew their earnings at an extraordinary, annualized pace of over 20%. Given that the aggregate U.S. earnings growth, which was bolstered by a handful of mega-cap growth companies, has been undifferentiated, it follows that most U.S. companies have been subpar vs. the rest of the world from a fundamental perspective.

Despite relatively weak earnings growth from a global perspective, the non-magnificent 68% of S&P 500 companies nonetheless trade at a significant premium to their non-U.S. peers. Going forward, unless these companies can produce greater earnings growth than those in other regions, their relatively elevated valuations are not fundamentally justified. Moreover, there are several reasons to suspect that that U.S. companies will fail to grow their earnings faster than those in other regions.

Firstly, the U.S. administration’s imposition of tariffs on its trading partners will inevitably raise costs for American companies and reduce the global competitiveness of goods produced in the U.S. Even in rare instances where U.S. companies are successful in passing through these increased costs to their customers, their profits will nonetheless suffer from lower volumes. In addition, recent developments in U.S. immigration policies will reduce the supply of labour, which will hinder economic growth. Lastly, continued policy uncertainty is likely to engender a “wait and see” mode among CEOs, thereby leading to lower levels of investment.

The Magnificence is Evolving

Even if the non-magnificent majority of U.S. stocks fail to deliver the superior earnings growth that is required to justify their relatively high valuations, there is always a possibility that the magnificent minority could save the day by delivering earnings that exceed expectations. At an aggregate valuation of 30 times forward earnings, magnificence does not come cheap. However, if these companies can continue growing their earnings at their historic pace, their valuations are sufficiently reasonable to allow for strong gains in their stock prices. Conversely, if their growth reverts to less magnificent levels, the ensuing capital losses could be substantial.

One of the key drivers of the magnificent Six’s success has been their ability to grow their earnings at a breakneck pace with far smaller amounts of investment than what has been required of past behemoths. However, they have been aggressively ramping up investment in response to the current AI gold rush. While it is possible that these investments will produce strong returns, the fact remains that the low investment/high growth dynamic which has been a key element of the magnificent six’s magnificence may be a thing of the past.

Have I got a Deal for You

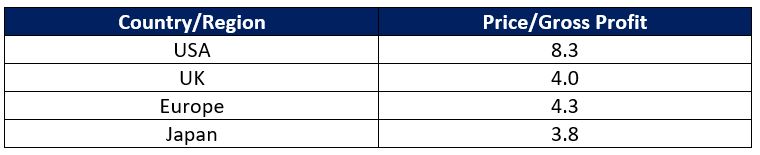

Given that U.S. companies have experienced similar earnings growth as their global peers, it follows that the former’s outperformance has been driven primarily by greater multiple expansion, which has resulted in U.S. P/E ratios that currently stand in the 90th percentile of their historical range. Relatedly, the earnings yield on U.S. stocks is close to an all-time low relative to Treasury yields. In contrast, international stocks are currently valued at a historically large discount to their U.S. counterparts.

Price/Gross Profit by Region

Admittedly, it is possible for valuations to become even more stretched in the short term, and timing markets perfectly is an exercise in futility. However, history strongly suggests that higher valuations foreshadow below average returns over the medium-to-long term. Moreover, in the absence of any compelling argument that future profit growth of U.S. vs. non-U.S. companies will be meaningfully different, the latter appear to be a relative bargain. Continue Reading…