By Michael Wickware, CMO, Planswell

Special to the Financial Independence Hub

We’re all accustomed to seasonal advertising. Real estate listings in the spring, back to school sales in late summer, holiday sales in the fall, and at the start of every new year, financial industry ads urging you to contribute to your RRSP.

The traditional RRSP season is driven by two main factors:

1.) The rules say you have the first 60 days of each new year to make a contribution that can be applied to your previous years’ tax return.

2.) RRSPs are lucrative for banks and financial advisors, because you’re likely going to keep paying them fees every year from now until retirement.

You might ask, “Isn’t it also driven by the fact that RRSPs are a great way for Canadians to save money?” The billboards, posters, banners and sales pitches certainly seem to suggest as much. I may be a marketing guy, but I work at a financial planning company, so I know it’s not quite that simple.

Unless these advertisers actually know about your personal financial situation, how can they be so sure that an RRSP is the right answer for you? Does absolutely everybody need to contribute to an RRSP, or is there some nuance these Mad Men might be missing?

In my search for answers, I had one major advantage. Planswell has built more than 100,000 financial plans for Canadians. Every plan is based on analyzing dozens of data points about things like goals, income, assets, debts, investments, insurance and more. In other words, I know more than any bank or ad agency about what individual people actually need to get ahead financially.

I asked our engineering team to dig into the data, and what we found definitely challenges the conventional wisdom:

An RRSP was wrong choice 52% of the time!

I didn’t think an RRSP was the best choice every time, but the gap between what the marketing campaigns are saying and what people actually need is a lot wider than I expected. It turns out the annual RRSP ad blitz, backed by all the biggest financial institutions in Canada, has been giving bad advice to half the country.

We decided to dig deeper, and found several reasons why an RRSP may not be the best choice for you. Here are three of the top reasons:

1.) It won’t always maximize your tax savings

An RRSP is not meant to avoid tax completely: just to put it off until you retire. The idea is to reduce your taxable income while you’re working and in a relatively high tax bracket, then pay the tax when you’re retired and in a lower tax bracket. But if you’re already in a low tax bracket, this strategy doesn’t work. And, if you’re early in your career and expect to be in a higher tax bracket in the future, you might be better off letting your RRSP contribution room accumulate until you can use it for a bigger benefit.

2.) You have shorter-term priorities

An RRSP is a long-term retirement investment. You don’t want to be paying fees and taxes and losing contribution room by taking money out early. That means you should make sure that your short-term needs are covered first. For example, if you don’t already have an emergency fund set aside or if you’re planning to buy a home or make a major purchase within the next few years, you may not want to lock your savings away in an RRSP now.

3.) You could miss out on bigger opportunities

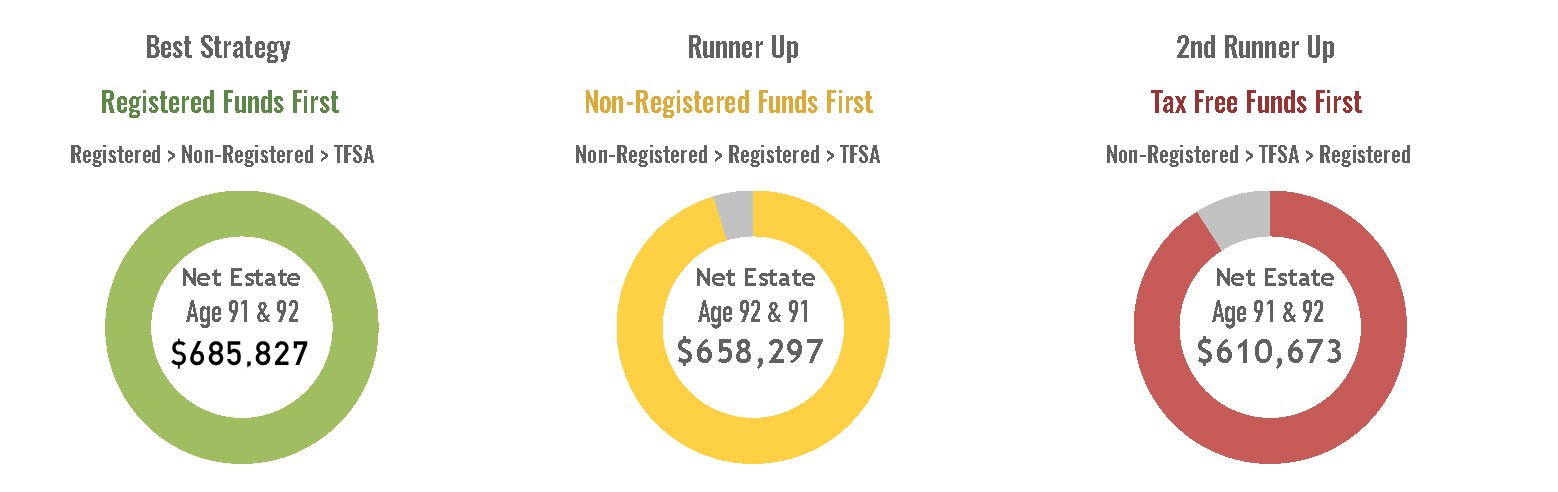

Let’s assume an RRSP makes sense from a tax point of view and that you have your short-term needs covered. You’re good to go, right? Not necessarily. Continue Reading…