By Ian Moyer

Special to the Financial Independence Hub

Pension incomes are not created equal. They come in all shapes and sizes. They are as varied as the people who have accumulated them and who seek to use them.

In this seemingly infinite variety, in this mathematical complexity, there is a common thread as far as advisors are concerned: delivering clients the most after-tax income possible.

CPP, OAS, Defined Benefit Pension, Dividend Income, Interest Income, RRIFs, Part Time Employment Income, Corporate Dividends, TFSAs: These are just a few of the various sources of income individuals may have access to when they exit the workforce. Upon retirement, decisions about what, when, and how much income to draw upon, move to the forefront.

Tax is key to coordinating multiple income streams

Coordination here is key as each of these sources of income is subject to different tax rates, different tax deferrals and different estate taxes. Tax is key, in other words.

Recent or prospective retirees need more than a competent advisor at this stage. Understanding the tax rates, tax deferral rates and the implications regarding OAS and Income Splitting is one thing. But accounting for these sources of income and the complicated ways in which they interact requires an algorithm.

The specialized software, Cascades, cascadesfs.com, performs these calculations, giving users informed withdrawal strategies. Designed by financial advisors in partnership with software developers, Cascades uses actual tax rates, not average tax rates, projecting for the duration of retirement, including longevity risk.

Because numbers require context to be meaningful, let us consider prospective retirees Bill and Anne Smith.

Case Study: a Couple in their late 60s

Retirement Plan: Bill and Ann are 68 and 67 currently. They have been retired for a few years but still have RRSPs and a LIRA and want to know if they should start using them for income or defer payments until age 71.

Income Sources: Both have CPP and OAS. Anne has a defined benefit pension from having worked as a teacher.

Investments: Bill has a healthy RRSP and Anne has a modest RRSP and a LIRA. They have maxed out their TFSAs and each have about $100,000 additionally in individual non-registered accounts.

Total: 12 different income sources and investment accounts to manage for retirement income

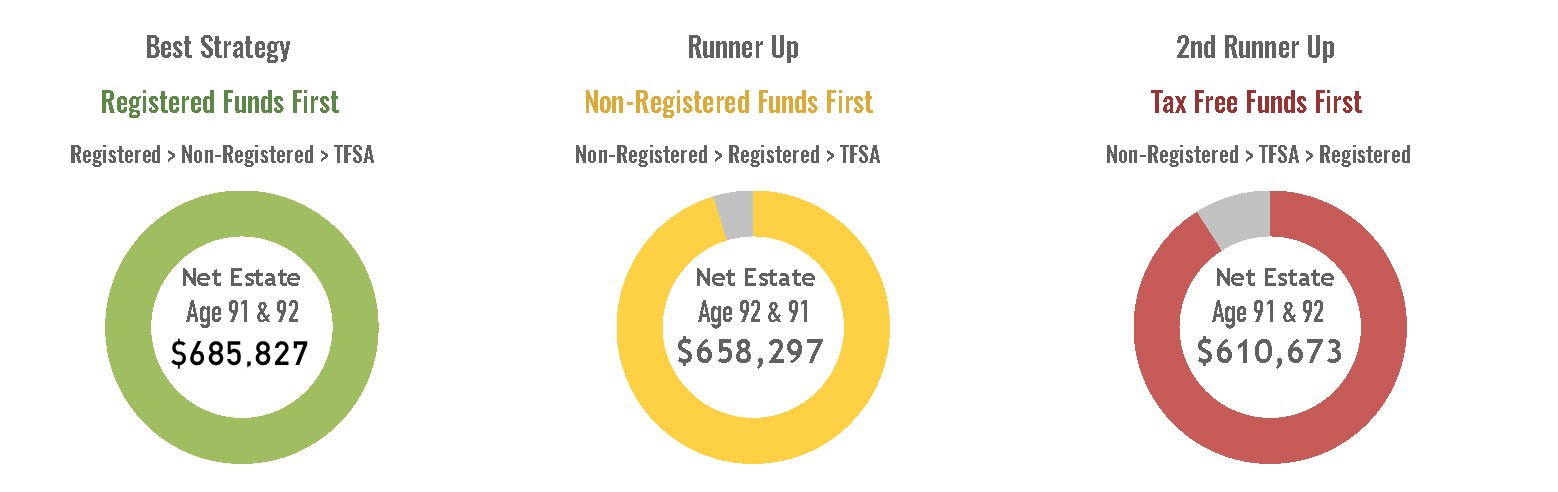

Cascades provides direction in the following way. Users — whether they be Anne and Bill themselves, or their advisors — fill in a detailed online questionnaire, submit their responses and in under ten seconds they have a report. This report (an excerpt is shown at the top of this blog) automatically gives three potential strategies and shows which one works best. For Anne and Bill, drawing down and re-investing their registered accounts first is expected to save them over $75,000 in their estate compared to a complete deferral of their registered money.

As far as Bob and Linda Sanderson are concerned, on the other hand, a Cascades report advises them to do just the opposite and ultimately predicts a savings of $125,000. Here’s how:

Quite different withdrawal recommendations for this younger couple

Bob and Linda are both 55 and currently working. They plan to retire in 10 years. They have a rental property they maintain that they plan to sell in 15 years and want to know how to plan for the long-term.

Income Sources: Both will receive CPP and OAS. Bob will receive a small defined benefit pension. Both will earn rental income until sale of the property. Both will receive corporate dividends until age 80 from a holding company.

Investments: Both have large RRSPs, nearly capped TFSAs, and a small amount of non-registered savings. Additionally, Linda has a small LIRA.

Total: 18 different income sources and investment accounts to manage for retirement income.

Cascades proposes three withdrawal strategies and highlights the best plan. Using all of their non-registered savings before rolling over registered investments will save Bob and Linda over $125,000 in their estate compared to an early drawdown of their registered money. Cascades software is designed to help users do their due diligence on the matter of retirement planning. The results are specifically tailored to the retirement in question and they are reliable, informed and rigorously defined as they are by Canada’s vast and varied tax laws.

.

Ian Moyer is the founder of Ian C. Moyer Insurance Agency Inc. and Cascades Financial Solutions Inc.

Ian Moyer is the founder of Ian C. Moyer Insurance Agency Inc. and Cascades Financial Solutions Inc.