By Tony Porcheron

Special to the Financial Independence Hub

What everyone wants is for their money to grow without any risk. This is of course impossible, especially over a short time period.

Risk is usually measured by volatility, however risk and volatility are not exactly the same.

Risk for most investors is the chance that they lose money or do not meet their long term financial goals.

Volatility is the amount that your investments go up and down over a certain time period.

sigma is the usual definition of Volatility

Beta defines how much a return is based on an underlying index or other investment

Alpha is your return earned above your index and volatility.

This is the holy grail of investing.

What methods do professional investors use so that volatility does not turn into risk? Asset Allocation.

You may have heard the term, “Don’t put all of your eggs in one basket”, this is Asset Allocation.

In most investment research, 80 to 90% of your investment returns are from you asset allocation, not your individual investment picking. Given this fact, this is what you should be paying attention to more than picking your winning investments.

Asset Allocation is deciding on what percentage of your portfolio should go into asset classes. Generally this is broken up by:

- Asset Type (Equity, Fixed Income, Alternative)

- Size of the underlying company (Large, Mid and Small)

- Geographic Region (USA, Canada, Western Europe, Asia, Emerging Markets)

You then make the decision:

- Manager type (Index, Active, Hedge)

- What are your financial goals? How close are you to them? Are you contributing or withdrawing money?

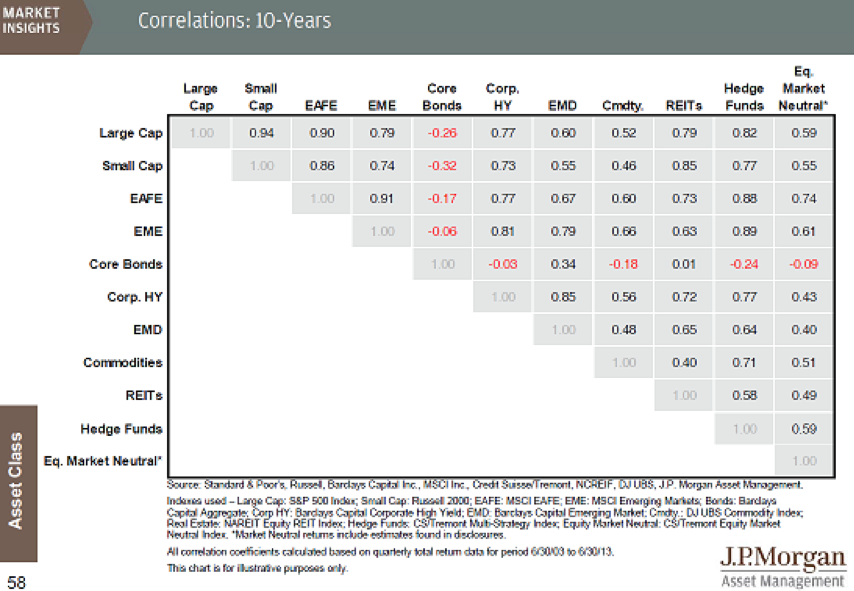

- What is the correlation between the different asset classes (how much do they go up and down together

The chart at the top of this blog shows a correlation analysis.

Strategic and Tactical Asset Allocation

The 2 main types of Asset Allocation are Strategic and Tactical. The adjustments to asset allocation are called rebalancing.

Strategic Asset Allocation is determining your asset allocation based on your long term investment return goals, volatility acceptance based on historical investment returns, volatility and correlation. Continue Reading…

We might consider this a truly green investment because the at the core (geothermal pun intended) we have Canadians who are making a choice to ‘Go Green’, or their version of green. As an investor, you are enabling those projects. Your monies will fund projects that will reduce CO2 emissions, and perhaps reduce polluting particulates that are a by-product of traditional energy generation. You will be an ‘investor agent of change’.

We might consider this a truly green investment because the at the core (geothermal pun intended) we have Canadians who are making a choice to ‘Go Green’, or their version of green. As an investor, you are enabling those projects. Your monies will fund projects that will reduce CO2 emissions, and perhaps reduce polluting particulates that are a by-product of traditional energy generation. You will be an ‘investor agent of change’.