“Can you believe it, honey? Friday’s my last day at work! Time sure flies. I can’t wait to start spending all of our free time together!”

Did this thought warm your heart, or get your pulse racing in panic? That probably depends on whether you’ve given some good thought to what you’re doing after retirement.

But what do you actually want to do after you stop working? Your retirement income goals will depend much on your answer to that question, as your financial adviser is apt to tell you.

We’re living longer — and that’s a good thing, if you plan for it

‘Retirement’ wasn’t really a thing, until recently. You lived, you worked, you died … and the world kept turning as youth picked up the baton of life’s track meet. That’s partly the reason pension age was set at 65: few were expected to live long enough to claim it! When the USA passed their Social Security Act in 1935, American men were expected to live to about 58.

But with our longer life spans, you could still be shuffling around decades after you’ve stopped working. According to Statistics Canada and the 2016 Census, “there were 5.9 million seniors in Canada, which accounted for 16.9% of the total population. In comparison, there were 2.4 million seniors in 1981, or 10% of the population.”

There are more retirees than ever! So, our question is a practical one: how do you retire and still fill 40 hours a week?

What Canadian retirees are already doing with their time

Does this all seem inspiring … or overwhelming? Is the room spinning at the prospect of playing shuffleboard and doing yard work for the next two or three decades? Fortunately, we’ve picked up an important idea from doing retirement income planning with countless clients. Continue Reading…

Canadian securities regulators may be putting investors at risk. They implemented a new mandatory risk weighting system in September 2017 based on 10-year Standard Deviation. Every Canadian mutual fund and exchange-traded fund (ETF) must now include a risk rating based on the following:

Before implementing this policy, the Ontario Securities Commission (OSC) asked for submissions from the industry. These can be viewed here.

Over 50 submissions were received (mine included.) and out of those, three warned about the deficiency that Standard Deviation does not differentiate between upside and downside volatility.

Scott C. Mackenzie of Morningstar made a particularly succinct comment:

“A conservative investor’s portfolio that is missing a key sector or asset class, essential for prudent diversification (and risk reduction), may demand the inclusion of a small amount of a concentrated sector mutual fund or ETF. A single measure risk score for such a vehicle may be higher than recommended for the investor and they are consequently dissuaded from incorporating it. The irony and potential downside is that the risk of the conservative portfolio may actually be higher than otherwise would have been had the investor included the diversifying investment. “Diversification as a risk-reduction activity is a sensible approach, practiced by many, and supported by decades of investment research.” http://www.osc.gov.on.ca/documents/en/Securities-Category8-

It does not differentiate between Standard Deviation and Downside Deviation; and

It measures individual portfolio components rather than the overall Standard Deviation of the entire portfolio.

This policy will not protect investors from experiencing losses, but may prevent investors from structuring portfolios for reduced volatility, optimal performance and effective diversification. The resulting reduction in investment demand in sector funds will result in a negative impact for many Canadian public companies.

The overall weakness of this approach is best exemplified by the fact that Bernie Madoff’s fund had the lowest Standard Deviation in the industry for over 30 years – yet investors lost most of their money.

David Ranson of H.C. Wainwright & Co. published a report entitled “Why Standard Deviation Won’t Serve to Classify the Risk of a Portfolio.” This report details why Standard Deviation is a poor and overly simplistic approach to measuring the risk of a portfolio.

“The riskiness of an investment product cannot be represented by the Standard Deviation (volatility) of its historical returns, or by any other single statistic … On a real risk scale, cash could be assessed as risky and gold as safe.”

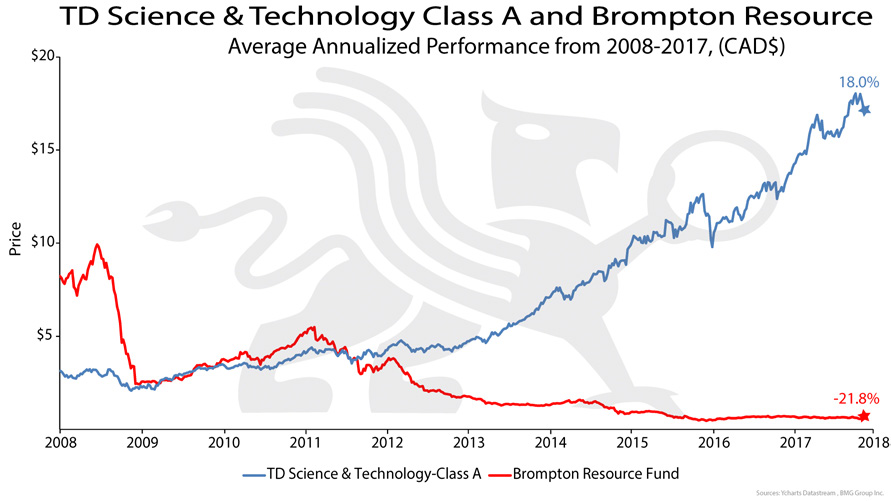

As an example of how flawed this policy is, Morningstar Canada lists 9,412 equity classes of mutual funds. Of these,1,932* have 10-year performance histories. The best-performing fund is the TD Science and Technology Fund, which achieved an 18.00% 10-year annualized return net of MER. A $10,000 investment in 2007 would now be worth $66,554*.

On the other side of the performance scale is the Brompton Resource Fund. It ranks as 1,932*(last) in performance and has experienced a-21.8% annual decline over the same 10-year period. A $10,000 investment ten years ago would now be worth only $643*.

*As of July 18, 2018

The 10-year (2008-2017) Standard Deviation for the TD Science and Technology Fund is 17.7% (MEDIUM to HIGH RISK) and for the Brompton Resources Fund it is 29.57% (HIGH RISK). However, the Downside Deviation is 10.6% (LOW to MEDIUM RISK) for the TD Fund and 25.7% (HIGH RISK) for Brompton Fund.

It should be obvious, even to the unsophisticated investor, that the risk of these funds that are at opposite ends of the performance spectrum is not similar.

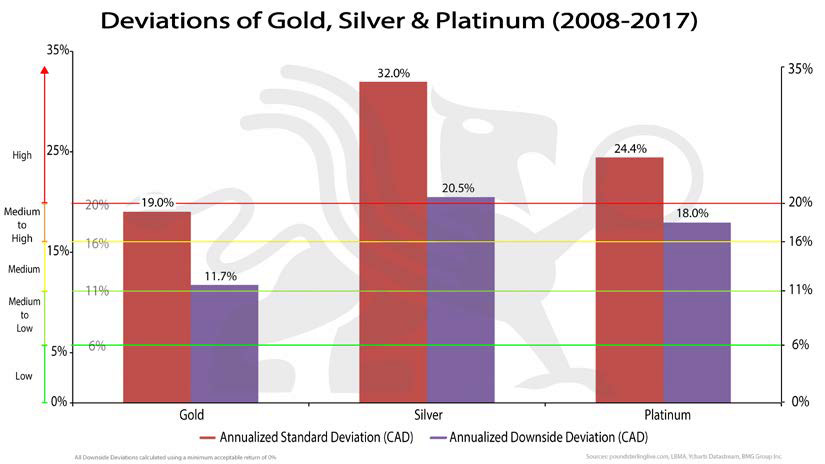

This flawed methodology is more pronounced when it comes to physical bullion funds such as the BMG Funds. According to this methodology, the Standard Deviation for gold results in a MEDIUM to HIGH risk rating. Silver and platinum would be rated HIGH RISK.

This new risk rating methodology is in direct contradiction to the suggested risk rating for gold established by the Basel Committee on Banking Supervision (BCBS). BCBS brings together regulators from 28 countries, and establishes rules governing the appropriate level of capital for banks. The current version of these rules, known as Basel III, is a key element of the international regulatory reform agenda put in motion following the global financial crisis of 2008. During the 2008 financial crisis, gold was used in international settlements as a zero-risk asset after many decades of being sidelined in the monetary system. Gold’s old emergency usefulness resurfaced, albeit behind closed doors, at the Bank of International Settlements (BIS) in Basel,Switzerland. Continue Reading…

In April, the Italian public was so incensed by the country’s broken government budget, endemic graft and unaffordable inward migration that half of the general election vote went to two protest parties. On the left, the Five Star Movement topped all, with 32% support, while the right-wing League party took 18%. Since then, the League has gathered even more support. Its leader, Matteo Salvini, may now be the most powerful person in Italy.

Salvini’s answer to the European Question

With a wave of migration from North Africa and the Middle East in recent years, Italy finds itself dealing with culture clashes and a scramble to find the money to house and feed the new arrivals.

But amid all the talk of the migrant crisis, what has gone largely unnoticed is that both Five Star and the League have some economic policies that are irrational at best, dangerous at worst. With the news cycle focused on cultural issues, we are wise to remember that Salvini, currently positioned as the champion of nativist Italy, has communist roots. His economic belief system has shifted with age, but this is no solace to EUR longs.

Key planks

The coalition government’s common ground includes overturning the Fornero Law, which increased retirement ages, and putting a universal basic income of €780 (C$1,193) per month on the table. However, the coalition does interestingly entertain the idea of a flat tax. All of these together would conspire to blow out Italy’s 2.3% budget deficit-to-GDP ratio.

Positive backdrop

Italy’s 1.4% GDP growth may be anemic, but it is above water, and high by Italian standards; the norm this century is +0.4%. The manufacturing purchasing managers’ index, at 52.7, has essentially been in nonstop expansion since the first quarter of 2015.1 Unemployment is down to a still-troubling 11.1%, but it was nearly 13% in 2014. Investors must ask: what odd fiscal and/or monetary policies will voters demand if conditions become recessionary?

Start with one such policy, which Brussels fears, that is haunting the bond market and EUR.

The specter of a parallel currency

A “New Lira,” side-by-side with the euro. The state will not come out and say it at the moment, but that’s what the proposal for “mini-BOTs” will mean. If Five Star and the League do go down this path, mini-BOTs would be short maturity debt instruments that can be used to state obligations. On the other side of the ledger, owners of the mini-BOTs could use them to pay taxes. This risk has been haunting the bond market and EUR since the idea entered the conversation in mid-May.

For this privilege

Figure 1 highlights in green the few bonds that yield more than two-year Canadian sovereigns. Australia and the U.S. generally yield more across the board, but investors have to reach for seven-year bonds in Italy to exceed Ottawa’s 2020 maturities.

Figure 1: Sovereign Yields (Highlighted Green if > Canadian Two-Year Government Bond)

December looms

The stated aim of the European Central Bank (ECB) is to “keep prices stable, thereby supporting economic growth and job creation.” But in the last decade, what mattered is its implicit mandate: keep Europe together. The combination of fuzzier European economic data and the potential for Italian mini-BOTs could cause a “dovish” surprise by the ECB’s Mario Draghi, who is set to end the central bank’s €30bn bond purchase program in December. Perhaps the surprise is an extension of the bloc’s zero interest rate policy for another year or so. That could harm EUR bulls.

European banks not yet indicating Contagion

One way in which European systemic risks can be priced is via bank credit default swaps (CDS). Figure 2 shows current CDS levels along with the peak fear points of the last five years. Continue Reading…

Have you ever thought about seasonal work in retirement? My friend, Kirk, recently leveraged seasonal work to experience something for the first time in his life. He became a cowboy, through a seasonal job at a Dude Ranch.

At Age 58!

You may remember Kirk, he’s visited with us before (including his thru-hike on the Appalachian Trail, his broken foot on the Pacific Crest Trail and the story of breaking his ribs when he Lived Life At The Limits on a mountain bike ride with yours truly). This Fall, he’s heading to Nepal to do some trekking around Mt. Everest. Interesting guy, my friend Kirk, and we can all learn something from the way he lives his life in retirement.

Today, he tells us the story of doing seasonal work in retirement at a Dude Ranch, which he did in the Spring of 2018.

The old military and corporate guy became a cowboy. Well, that may be a bit of an exaggeration, but he did “wrangle horses” for 6 weeks at a Dude Ranch. How cool is that?

Here’s his story…

Working On A Dude Ranch

Kirk. A “FIRE Guy In His Prime”

I promised myself I would write three “potential” blog posts for my friend this year covering what could possibly be my most adventurous year since my retirement began 2 ½ years ago. Caution: I am not the spectacular writer that Fritz is; however, here is my latest adventure …

(Note from Fritz: I don’t know about my writing skills, but I do know that Kirk lives life more “on the edge” than anyone I personally know. Nepal, really? That Kirk guy is nuts!)

When I retired roughly 2 ½ years ago I decided to do away with my “LinkedIn” account. I was cleaning up some old things from my work years and didn’t think I would need a resume in my retirement life. As I started checking off things in my Dump Truck List (Buckets are no longer big enough) I started realizing that I had some skill gaps. Ultimately, I wanted to be a wrangler for a cattle drive in Montana but realized that wasn’t going to happen if I didn’t have some experience handling a horse.

I researched some possible jobs through www.coolworks.com and drafted a list of the qualifications for some of the wrangling jobs which interested me. Much to my surprise, I met them all with one exception:

I had no experience in riding a horse.

Having grown up on a farm really prepared me well for many aspects of the job, but we never had horses. How could I learn to ride a horse, handle the tack, teach the ranch’s customers, etc. if I didn’t know how to handle horses myself? While I suppose I could have paid for the experience — I am FI [Financially Independent], after all — there was something in me that kept gnawing in the deep recesses of my mind.

Thoughts which whispered, and thoughts that led to my decision to pursue seasonal work in retirement:

You have been so frugal all your life to get to FI, is this really how you want to spend your money?

Would you really be able to buy this experience or is this something you have to spend time acquiring skill, talent, and familiarity?

What other experiences do you need now in order to pursue the future adventures of your dreams?

(Note from Fritz: I like how Kirk thinks several moves ahead. Dream for your tomorrow, and identify what you should be doing Today in order to achieve your dreams. Move your life from Good To Great).

After much thought, I decided to venture out to an unknown area for me and listen to the younger crowd who said many of their wonderful experiences were as “Workaway” people. Workaway is simply a web service that connects people who are looking for experience with people that are looking for help. The Workaway people generally work 4 – 5 hours per day, 5 days per week in exchange for room/board and experience. Given that I have plans to travel through Asia in the coming years, this approach could help with some international options as well. I looked into the site http://www.workaway.info and decided to give it a try.

It was somewhat difficult to determine where I would go to gain this experience. I wasn’t sure how it would all work out, so I decided to minimize my risk by choosing a location that:

had good/great reviews by those who participated

was close so if it was horrible I could bail

had more than just myself as a workaway so I could learn from the experience of others

I ended up selecting a Bed and Breakfast Dude Ranch in upstate NY, only an hour away from where I grew up and where my mother still lives. If it was a horrible experience I had a solid Plan B. I would simply bail out and stay with my mom, working around her house to complete some things on her “To Do” list. It would also afford me the opportunity to spend time with some aunts, uncles, and cousins which I had not seen in far too long. Continue Reading…

In the modern world, there are two types of debt: good bad and bad debt. Good debt would be considered financing something that has the potential to go up in value, like a home or a small business. Bad debt would be considered consumer debt like jewelry, designer clothes, and luxury cars. These things tend to depreciate. People typically get into trouble financially when they start going into debt with consumer goods or things they really don’t need.

1.) Create a budget

Unless you are already financially well-off, you are going to need to create a budget for you and your family. This is the single biggest way not to go into debt. Why? Because you are tracking every dollar you spend. Start out by listing your monthly income after taxes at the top of the budget, then list your expenses below that. If you don’t have a surplus of money after all your expenses are accounted for, you are either spending too much money or you are not making enough money. Whatever the case may be, adjust your budget accordingly.

2.) Quickbooks

The Quickbooks online platform by Intuit is probably one of the best online financial tools you can use for your business. In general, it is an online accounting software that helps manage your finances for you. With an easy Quickbooks online payment, you can pay people and you can receive money too. In the end, business finances can get pretty confusing. Quickbooks allows you to track your finances more easily. Also, Intuit has a budgeting app called Mint. I use Mint quite often and it tracks all my transactions and spending activity. It also tracks your budgets, monthly cash flow, and your credit score along with many other investments and other accounts.

3.) Emergency fund

Let’s face the fact that bad things happen to good people. When these setbacks occur, people need money set aside to protect themselves from debt. This is what an emergency fund can do. First, start by putting away a simple $1,000 just in case an emergency happens. Continue Reading…

By Tea Nicola

By Tea Nicola