By Ed Rempel

Special to the Financial Independence Hub

TFSA vs. RRSP is one of the most common questions I am asked. If you want to know for sure which is better for you, then you need a financial plan.

Many articles have been written on this topic that list pros and cons with general opinions.

The truth is that:

1.) Rather than just having an opinion, there is a precise right answer specifically for you. To the extent that you know your present and future marginal tax brackets, you can calculate a precise optimal contribution for RRSP and TFSA for each year, as well as the optimal amounts to withdraw each year after you retire.

2.) The decisive factor is your tax brackets now vs. after you retire. Most people just assume they will be in a lower tax bracket after they retire, because their income will be lower. In many cases, that is not true.

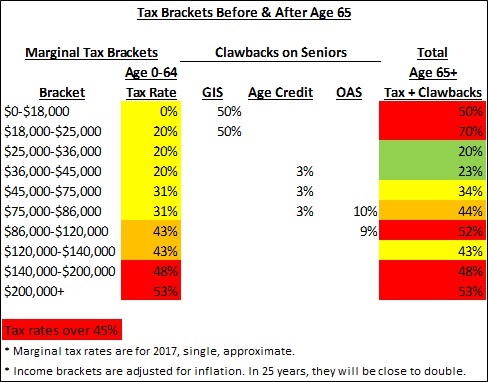

When you include the clawbacks of government income programs that affect everyone over 65, many seniors are in shockingly high tax brackets!

The clawbacks cost you actual money and are the same as a tax. The three main clawbacks are the 50% clawback on GIS for low incomes (under $20,000), 15% clawback on the age credit for middle incomes ($35,000-85,000), and the 15% clawback on OAS for higher incomes ($75,000-120,000).

The chart above shows the actual approximate tax brackets before and after age 65. Check out the tax brackets over 45% in red:

Understand the differences

You can own the same investments in your TFSA as your RRSP. The main difference is that RRSP contributions and withdrawals have tax consequences, while TFSA contributions and withdrawals don’t.

Therefore, the answer to TFSA vs. RRSP is primarily based on your marginal tax bracket today compared to when you withdraw after you retire: Continue Reading…