I have stood here before inside the pouring rain

With the world turning circles running ’round my brain

I guess I’m always hoping that you’ll end this reign

But it’s my destiny to be the king of pain

– King of Pain by The Police

By Noah Solomon

Special to Financial Independence Hub

This may seem strange coming from a me: a quant geek who uses data, technology, and machine learning to develop and manage investment strategies, but here it is:

I believe that technology has made markets less efficient.

The efficient-market hypothesis (EMH) was developed in the 1960s at the Chicago Graduate School of Business. It states that asset prices reflect all available information, causing securities to always be priced correctly, thereby making markets efficient.

In my view, perfect efficiency is like the tooth fairy: it would be nice if it really existed, but in reality, it is purely fictional. This divide between the ivory tower and the “real world” was epitomized by the legendary Fisher Black, co-architect of the Black Scholes option pricing formula. After moving from M.I.T. to Wall Street, Black remarked, “Markets look a lot less efficient from the banks of the Hudson than the banks of the Charles.”

Bubbles: The Archnemesis of the EMH

Over the past several decades, markets have borne witness to two extreme bubbles:

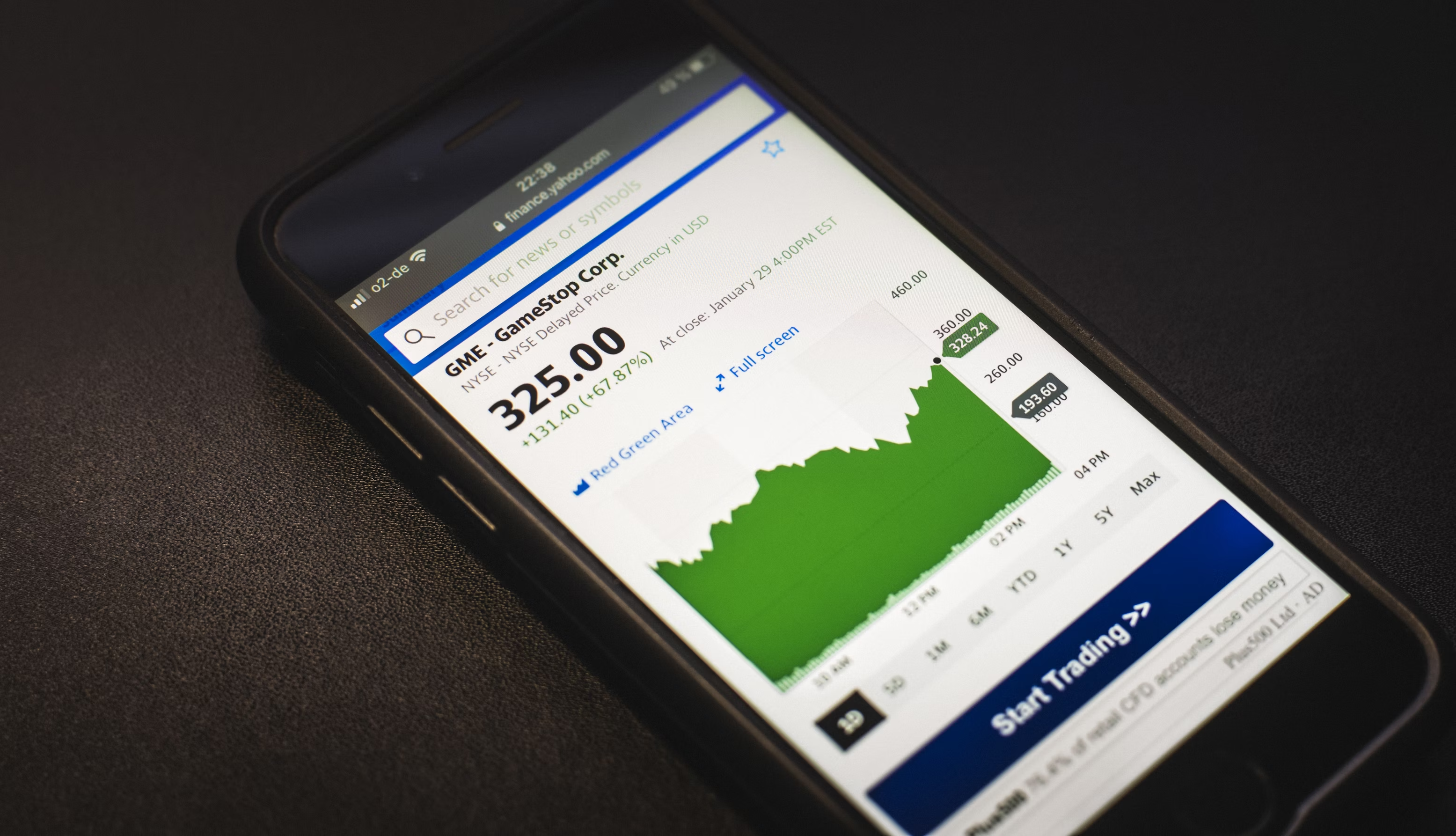

- In 1989, the Japanese stock market was trading at 65 times earnings. The aggregate value of Japanese stocks exceeded that of U.S. stocks despite the fact that the U.S. economy was three times the size of Japan’s. Soon after, things went from sensational to miserable, with Japanese stocks suffering a particularly prolonged and steep decline.

- Little more than a decade later, the S&P 500 Index, aided and abetted by a tremendous bubble in technology, media, and telecom stocks, reached the highest multiple in its history. Not long thereafter, the index suffered a peak trough decline of roughly 50% over the next few years.

Clearly, to quote palace guard Marcellus in Shakespeare’s Hamlet, “Something is rotten in the state of Denmark.” How is it that markets experienced such extreme aberrations? I’m not sure that “crazy” is the right word, but I’m darn sure that it’s not “efficient.”

Without a doubt, periodic bubbles can be attributed to recency bias, a common behavioural quirk where investors overweigh recent information and events at the expense of considering objective facts and probabilities. This can cause people to chase recent winners and push their prices to unsustainable levels. According to famed economist John Kenneth Galbraith:

“There can be few fields of human endeavor in which history counts for so little as in the world of finance. Past experience, to the extent that it is part of memory at all, is dismissed as the primitive refuge of those who do not have the insight to appreciate the incredible wonders of the present.”

Recency bias notwithstanding, I believe that there are other factors at play that are contributing to irrational behaviour and resulting in decreased market efficiency.

The Rise of Passive Investing & Market Efficiency: Nobody Knows

A persistent feature of markets over the past 20 years has been a secular shift in assets from active managers to passive, index-tracking funds. I do have some sympathy for the argument that this has led to less efficient stock prices. Granted, if the entire world shifted to indexing, then by definition markets would become inefficient for the simple reason that nobody would be analyzing companies.

However, this is clearly not the case, which begs the question of what percentage of investable assets need to be in passive vs. active strategies to engender a meaningful decline in market efficiency. I don’t believe that anyone can answer this question with any degree of certainty.

The Paradoxical Effect of Technology: The Wise Crowd vs. the Foolish Herd

Market manias and the related mispricing of assets seems paradoxical given the amount and speed of information that has become widely available over the past 20 years, not to mention the precipitous declines in commissions and other trading costs. However, speed and availability of information is a proverbial double-edged sword, especially as it pertains to the efficiency of markets over the medium to long term.

In theory, technological advancements, and specifically the ability to obtain and process greater amounts of information at an increasingly rapid rate, should make markets more efficient. However, these developments are not a significant factor for investment strategies with medium or longer-term horizons, for which the speed and availability of information are not particularly important.

On the other hand, technology has had a deleterious effect on the proverbial “wisdom of the crowd,” which is defined as “the notion that the collective opinion of a diverse and independent group of individuals (rather than that of a single expert) yields the best judgement.”

The catch here lies in the word “independent.” While I agree that security prices should be “correct” when investors think and act independently, this is clearly not the case when they act with a herd mentality and all run off the lemming cliff in unison. Under such circumstances, the crowd’s “wisdom” becomes anything but, which leads to manic behaviour and market inefficiencies. In a world where social media personalities such as Keith Gill (Roaring Kitty) can incite their millions of followers into frenzied bouts of groupthink, crazy things are bound to happen. Continue Reading…