By Billy and Akaisha Kaderli

Special to Financial Independence Hub

Millennials, those born roughly between 1980 and the year 2000, face a different future than Baby Boomers did at their same age. In terms of Wealth Building and saving for Retirement their challenges are wage stagnation, unemployment, underemployment and a seeming sense of entitlement. Because they came of age during the Great Recession, their faith in brokerage firms, Wall Street and global banks has been bruised.

Being optimists, we believe the financial future of this generation can still be bright, but with loads of student debt and lack of investment understanding they need to get started learning about finances and money management now.

Time is on your side and is your greatest asset

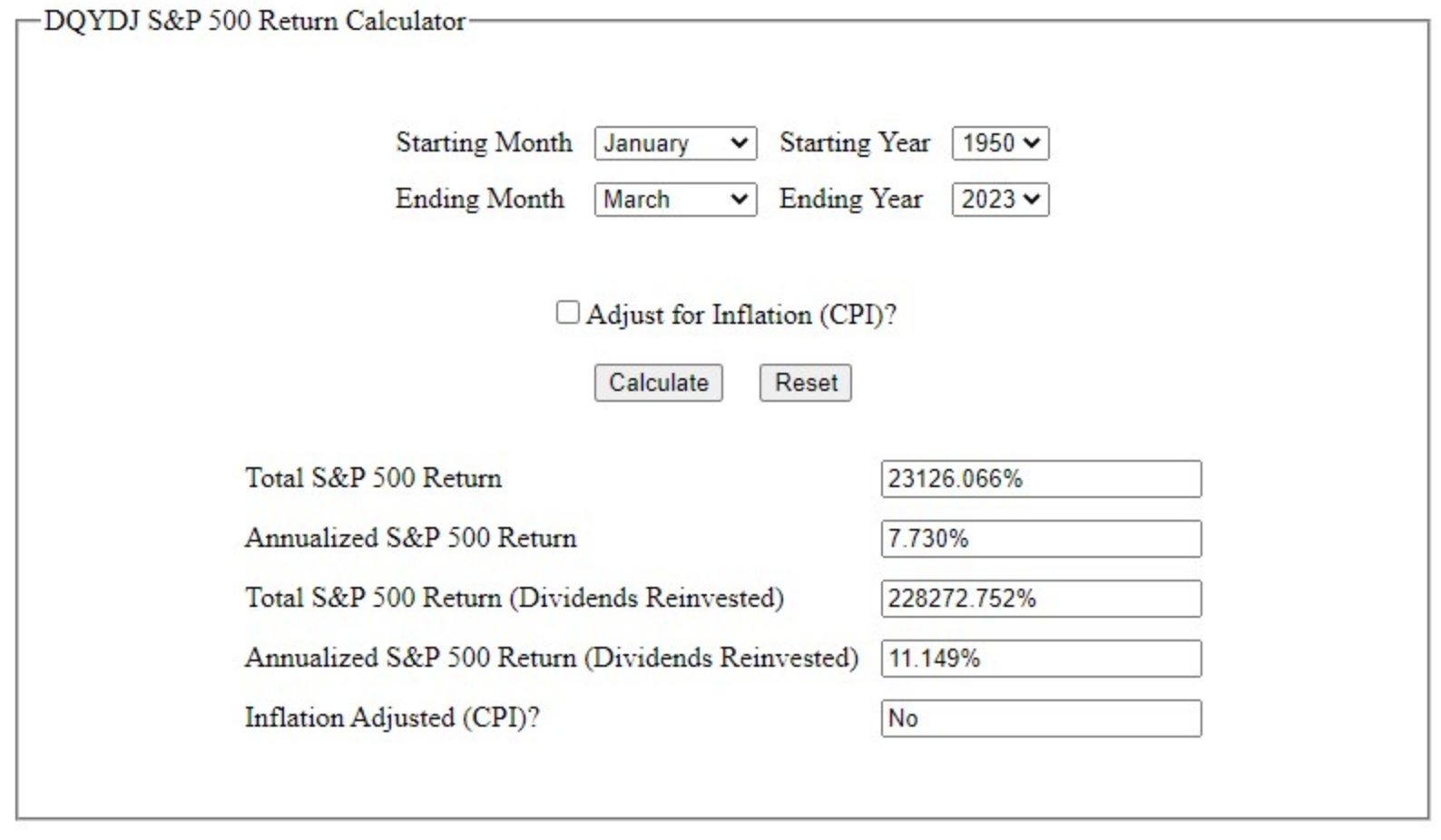

One thing Millennials have today that Boomers don’t is great stretches of time before Retirement. It is their greatest resource and this fact needs to be made clear to them. Time cannot be replaced, and if you are a Millennial, then knowing about the power of compounding will change your financial life. $10,000 – the cost of a used car – invested today in the S&P 500 Index and based on market historical returns from 1950 to March 2023 could grow to US$1,000,000 or more throughout your career, thereby building a solid foundation for your retirement needs. This return is without adding another dollar to your investment.

S&P Market Return Chart

S&P Market Return Chart

If you do nothing else for your retirement, scrape and scrap to make this investment into SPY (S&P 500 Index ETF) or VTI (Vanguard Total Stock Market ETF) and you will be handsomely rewarded, since you have this time on your side.

Just get Started

A new investor with limited funds can utilize an online, no-frills brokerage account and — depending on which brokerage you pick — you can open an account with less than $1,000. Not every house requires initial investments of more than $2,500, and as of this writing, Fidelity is offering a no minimum for opening an account. Continue Reading…