Merry Christmas!

Below we canvas 11 retirement experts and financial planners in Canada and the United States about how they and their clients can use new Longevity insurance products above and beyond traditional life annuities.

These experts were gathered by Featured.com, which has been supplying Findependence Hub with quality content for several years. It recently changed its procedure so editors like myself can request input on particular topics we think will interest our readership. The sources are all on LinkedIn, as you can see by clicking on their profiles below.

Here’s what we asked for this instalment:

“In addition to Annuities, what is one new Longevity product or fund that you believe in enough to recommend to clients approaching or already in Retirement? Examples in Canada are Purpose Longevity Fund and Guardian’s Longevity Funds. Are there similar new products in the U.S. (or Canada) of which you are aware?”

Here is what these 11 thought leaders had to say:

In addition to traditional annuities, one of the emerging longevity products in the U.S. that I have come to recommend to clients approaching or already in retirement is the LifeX Longevity Income ETF, particularly the LFAI fund.

In addition to traditional annuities, one of the emerging longevity products in the U.S. that I have come to recommend to clients approaching or already in retirement is the LifeX Longevity Income ETF, particularly the LFAI fund.

While it is not a classic insurance product, it is designed to provide predictable monthly distributions over a long horizon, effectively hedging against the risk of outliving one’s assets. The fund invests primarily in U.S. Treasuries and money-market instruments, and its structure is built around the concept of a target cohort’s 100th birthday, which allows for a systematic income stream without relying on a life insurance company guarantee.

For many clients, especially those who purchased assets during low-interest periods or are seeking reliable cash flow without tying up their entire portfolio in an annuity, this product offers a compelling complement to their existing retirement income strategy. What I find particularly valuable is the transparency it provides. Unlike certain annuities, clients can clearly see the underlying investments, understand how distributions are generated, and retain the flexibility to adjust allocations as their personal circumstances or market conditions evolve.

It also fits naturally into a broader retirement strategy where a portion of assets remains growth-oriented, some is allocated to defensive income-generating investments, and a dedicated longevity-income segment addresses the specific risk of living decades beyond retirement.

Of course, it is not without considerations; while the fund aims to provide stable income, it is sensitive to interest-rate changes, inflation, and the assumptions built into its cohort-based design. Clients need to assess the fit carefully, ensuring the time horizon and income targets align with their health, lifestyle, and other holdings. For those who understand these dynamics, however, it offers a sophisticated and innovative approach to longevity planning, bridging the gap between traditional annuities and fully self-managed income portfolios, and giving retirees confidence that they can sustain their lifestyle even as they live longer than expected.

Andrew Izrailo, Senior Corporate and Fiduciary Manager, Astra Trust

If you’re getting close to retirement, you might want to check out the BlackRock LifePath Paycheck fund. I’ve been following it. It works like those Canadian longevity funds, designed to give you regular monthly checks. The biggest risk is outliving your savings, and this fund has professionals handle the withdrawals so you don’t run out of money. It seems to offer more flexibility than a traditional annuity, which is worth a look.

JP Moses, President & Director of Content Awesomely, Awesomely

——————————————-

The Vanguard Target Retirement Income Fund is not an entirely new “longevity” product in the mold of Canada’s Purpose and Guardian funds, but it fulfills a similar role for retirees. It is intended to deliver a steady flow of income while protecting against the effects of inflation by investing in a diversified blend of stocks, bonds and cash. The Fidelity Strategic Advisers (r) Core Income Fund is also designed to provide income for retirees with a diversified approach. The two funds both provide some level of stability for those who want to keep a lid on risk and market vomit in retirement.

Evan Tunis, President, Florida Healthcare Insurance

——————————————-

I’ve often been asked about newer longevity products beyond traditional annuities, especially by clients preparing for retirement who want flexibility without giving up stability. What I have observed while working with financially cautious founders and executives is that people want income structures that feel modern, transparent, and liquid, and one option in the U.S. that I genuinely find promising is the Stone Ridge LifeX Longevity Income ETFs. I first came across them while helping a client map out a long term retirement strategy, and what stood out was how these funds provide monthly distributions while still allowing investors to keep full liquidity. I remember reviewing the structure and appreciating how it focuses on Treasuries and a long horizon rather than tying someone into an insurance contract. It felt refreshing. many retirees dislike the idea of locking up money permanently, and this approach allowed them to protect their cash while still receiving consistent income. The experience reminded me of moments with founders who want efficiency without losing control, and pattern is similar

In my opinion, the biggest advantage of these longevity ETFs is the balance between predictability and freedom, since investors receive monthly payouts but can still adjust their strategy if life takes an unexpected turn. The main drawback is that there is no lifetime guarantee, so someone who ends up living much longer than expected might outlive the structure if they rely on it too heavily. I often explain that longevity planning still requires layering different tools rather than expecting one product to solve everything. Another point that came up during discussions with retirees is the sensitivity to interest rate changes, which can affect the value of the ETF itself, and it is important not to overlook that risk. Still, for clients who want something more adaptable than an annuity, this has become a strong option to consider. I also pay attention to emerging pooled longevity concepts, similar to modern tontine ideas, which share risk across participants and create higher payouts for those who live longer. Even though these structures are not mainstream in the U.S. yet, the logic is compelling for retirees who expect longer than average lifespans. Whenever I see innovation like this, I feel the same excitement I do when a founder shows us a new model at spectup because it signals that the industry is shifting toward more transparent, flexible solutions.

Niclas Schlopsna, Managing Partner, spectup

——————————————-

When I think about longevity-focused options beyond traditional annuities, one U.S. product I genuinely find compelling is the Stone Ridge LifeX Longevity Income ETFs. What draws me to LifeX is that it tries to solve the same problem that Canadian funds like Purpose Longevity and Guardian Longevity address — steady income over an unknown lifespan — but without locking someone into an irreversible insurance contract.

Instead of handing over capital permanently, retirees stay invested and receive structured monthly distributions, which feels more flexible and respectful of changing needs. I’ve always liked the idea of having income that mimics an annuity while still keeping the door open if health, family, or market circumstances shift.

I’ve come to see LifeX as especially appealing for clients who want predictable cash flow but aren’t comfortable giving up control of their assets. Because the funds are built largely on U.S. Treasuries, the income stream feels relatively stable, and the target-date structure helps align payouts with the later stages of retirement, when longevity risk becomes more real. The liquidity alone makes it feel like a meaningful evolution in retirement planning: it’s easier to sleep at night knowing the money isn’t trapped.

Of course, I’m also realistic about its limitations. There’s no lifetime guarantee the way a true annuity offers, and the income still depends on market and interest-rate dynamics. It’s not a perfect replacement for insurance-based products. But as a complement — or even a middle ground between full guarantees and full market exposure — it’s one of the few newer U.S. longevity products I’d feel confident putting on the table for someone approaching or entering retirement.

Sovic Chakrabarti, Director, Icy Tales

——————————————- Continue Reading…

My latest MoneySense Retired Money column looks at a curious Canadian phenomenon called The Annuity Puzzle: that while life annuities sold by insurance companies seem to have all sorts of compelling reasons to acquire them, more often that not retirees shun them.

You can find the full column by clicking the hypetexted headline here: Unlocking the Annuity Puzzle: Why Canadians avoid what seems to be the perfect retirement vehicle

Financial planner Robb Engen recently tackled this puzzle in his Boomer & Echo blog, illustrated in the above graphic. You can find the full blog here: Why Canadians avoid one of Retirement’s most misunderstood Tools.

Engen notes that experts like Finance professor Moshe Milevesky and retired actuary Fred Vettese say “converting a portion of your savings into guaranteed lifetime income is one of the smartest and most efficient ways to reduce retirement risk.” Vettese has said the math behind an annuity is “pretty compelling,” especially for those without Defined Benefit pensions.

Engen observes that a life annuity is “the cleanest version of longevity insurance … You hand over a lump sum to an insurer, and they guarantee you monthly income for life. If you live to 100, the insurer pays you. If stock markets collapse, you still get paid. If you’re 87 and never want to look at a portfolio again, the income keeps flowing.”

In other words, annuities neutralize the two big risks that haunt retirees: Longevity Risk (the chance of outliving your money) and Sequence-of-returns risk: the danger of suffering a stock-market meltdown early in Retirement and inflicting irreversible damage on a portfolio.

Despite all the seeming positives about annuities, Engen notes that “almost nobody buys one.” He cites a Vettese estimate that only about 5% of those who could buy an annuity actually do so.

A chance to lock in recent portfolio gains?

Even so, the new Retirement Club created by former Tangerine advisor Dale Roberts earlier this year — see this blog posted on this site in June — recently featured a guest speaker who extolled the virtues of annuities: Phil Barker of online annuities firm Life Annuities.com Inc. Barker said many clients tell him they’ve done really well in the markets over the last 20 years and now they’d like to lock in some of those gains. They may be looking for Fixed-Income strategies and many were delighted with GIC returns when they were a bit higher than they are now (some in the range of 5%). But they less happy with the new rates on GICs now reaching maturity. Meanwhile, annuities have just come off a 20-year high in November 2023 so the time to consider one has never been better, Barker told the Club in August. With annuities you can lock in a rate for the rest of your life so if your timing is good, it may make sense to allocate some funds to them.

See the full MoneySense column for the list of the eight life insurance companies that offer annuities in Canada, how they are covered under Assuris, when Annuities really shine, and how to fund annuities with registered or non-registered accounts.

I suspect the Club’s session on annuities was enough to get a few members off the fence. I have long been impressed by the aforementioned Fred Vettese, who often argues that those preparing to convert their RRSPs into RRIFs might opt to annuitize 20 or 30% of the amount, thereby transferring a chunk of investment risk from the do-it-yourself investor on to the shoulders of a Canadian life insurance company. Continue Reading…

Below we canvassed more than 20 retirement experts and financial planners in both Canada and the United States about how they and their clients can use new AI Tools to help investors pick stocks or ETFs and plan their retirement.

These experts were gathered by Featured.com, which has been supplying Findependence Hub with quality content for several years now. It has changed its procedure so that editors like myself can request input on particular topics we think will interest our readership. The sources are all on LinkedIn, as you can see by clicking on their profiles below.

Here’s what we asked:

Their answers are below, which have been re-ordered by me and in some instances edited down, using an ellipsis (…) to indicate cut passages.

“AI doesn’t replace financial advisors: it elevates investors to think and plan like one.”

One of the most powerful ways investors and retirees can use AI tools like Grok or ChatGPT is to transform information overload into clear, actionable insight not just faster, but smarter. These tools allow individuals to run scenario-based retirement models, stress-test investment ideas against historical data, and translate complex financial language into plain English they can actually act on. What I recommend most is using AI as an always-available financial co-pilot a tool that helps you ask better questions, explore tax and withdrawal strategies, and stay disciplined when emotions run high. Of course, AI should enhance, not replace, professional advice; but when paired with fiduciary guidance, it becomes a force multiplier for better decision-making. The future of retirement planning is not just automated: it’s augmented, where every person can access institutional-grade research and personalized planning at a fraction of the cost. — Justin Smith, CEO, Contractor+

One of the most powerful ways investors and retirees can use AI tools like Grok or ChatGPT is to transform information overload into clear, actionable insight not just faster, but smarter. These tools allow individuals to run scenario-based retirement models, stress-test investment ideas against historical data, and translate complex financial language into plain English they can actually act on. What I recommend most is using AI as an always-available financial co-pilot a tool that helps you ask better questions, explore tax and withdrawal strategies, and stay disciplined when emotions run high. Of course, AI should enhance, not replace, professional advice; but when paired with fiduciary guidance, it becomes a force multiplier for better decision-making. The future of retirement planning is not just automated: it’s augmented, where every person can access institutional-grade research and personalized planning at a fraction of the cost. — Justin Smith, CEO, Contractor+

Use AI for Grunt Work & Routine Analysis

I use AI to handle the grunt work for my finances. It’s great for automating my investment tracking and finding savings opportunities. For my SaaS business, I have ChatGPT audit expenses and run tax simulations. It catches small details I would definitely miss, but I always double-check with my accountant before making any big moves. — Cyrus Partow, CEO, ShipTheDeal

Running a fintech team, I use AI like Grok to track portfolios and summarize complex financial statements. I have it monitoring global trends that might affect Canadian retirement planning. Integrating these tools took some time, but the process is way less stressful now. My rule is to let AI handle the routine analysis while I double-check any critical decisions myself. — Sreekrishnaa Srikanthan, Head of Growth, Finofo

A good way to use AI tools like Grok or ChatGPT for investing and retirement planning is to treat them as helpful guides that explain financial topics, summarize current market information, and assist with planning choices. These tools can make complex financial ideas easier to understand, break down how different investment options work, and help create scenarios based on your retirement goals. You can ask questions to check your knowledge about topics like spreading your investments or tax rules related to retirement accounts, getting clear answers that fit your situation.

A good way to use AI tools like Grok or ChatGPT for investing and retirement planning is to treat them as helpful guides that explain financial topics, summarize current market information, and assist with planning choices. These tools can make complex financial ideas easier to understand, break down how different investment options work, and help create scenarios based on your retirement goals. You can ask questions to check your knowledge about topics like spreading your investments or tax rules related to retirement accounts, getting clear answers that fit your situation.

These AI tools also provide updated summaries of financial news and alert you to changes that could affect your retirement plans, like new laws or required withdrawals. While they do not replace a human financial advisor’s insight, they give you useful information that helps you talk to professionals with more confidence. Regular use helps keep you informed about your progress and reminds you of important details, making managing your retirement plan easier. — Richard Dalder, Business Development Manager, Tradervue

Use to summarize Market Trends

I work in tech marketing, so I’ve started using ChatGPT to research retirement investments. I’ll have it summarize market trends in telecom or healthcare IT, then cross-check with mainstream financial sources. This saves me hours of initial screening time. My advice is to never act on an AI’s take without fact-checking it first, but it’s a great way to get the lay of the land quickly. — Andrew Dunn, Vice President of Marketing, Zentro Internet

Use AI as a Personalized Planning Engine

My top recommendation is to use AI as a personalized planning engine. Feed it your retirement goals, income range, expected timeline, and risk comfort. Ask it to build draft scenarios, compare tax-advantaged account strategies, summarize differences between contribution options, or outline the impact of shifting a portion of your portfolio into metals, equities, or fixed income. This gives you a structured starting point before you meet with a licensed advisor.

My top recommendation is to use AI as a personalized planning engine. Feed it your retirement goals, income range, expected timeline, and risk comfort. Ask it to build draft scenarios, compare tax-advantaged account strategies, summarize differences between contribution options, or outline the impact of shifting a portion of your portfolio into metals, equities, or fixed income. This gives you a structured starting point before you meet with a licensed advisor.

AI also helps people evaluate items of value they already own. Many Americans keep gold or silver tucked away because they are unsure where to start or who to trust. Ask AI to walk you through how precious metal markets move, how payouts are typically calculated, and what reputable U.S. buyers offer. When people understand what their gold is actually worth, they make smarter decisions about whether to sell, hold, or incorporate it into their retirement strategy.

Using AI this way puts you in control. It speeds up research, cuts through noise, and helps you prepare with confidence before talking to a financial professional. — Brandon Aversano, CEO, The Alloy Market

I work with AI and financial data, and here’s what I’ve found: nobody reads those static retirement planning sheets. We switched to interactive simulations using tools like ChatGPT, letting people play out different investment choices and actually see the results. Engagement went way up. If you’re planning retirement in the U.S. or Canada, this gives you a much better feel for your financial future than any document. — John Cheng, CEO, PlayAbly.AI

I work with AI and financial data, and here’s what I’ve found: nobody reads those static retirement planning sheets. We switched to interactive simulations using tools like ChatGPT, letting people play out different investment choices and actually see the results. Engagement went way up. If you’re planning retirement in the U.S. or Canada, this gives you a much better feel for your financial future than any document. — John Cheng, CEO, PlayAbly.AI

Use to plan Retirement and support Financial Literacy

AI tools like Grok and ChatGPT shine brightest in retirement planning when used to simplify complex financial decisions. One powerful approach is creating personalized scenario models: quick projections that show how small adjustments in savings, expenses, or timelines can change long-term outcomes. This turns retirement planning from an abstract, overwhelming challenge into a set of clear, data-driven choices.

Another strong use case is ongoing financial literacy support. AI assistants can distill dense market insights, tax rules, or investment updates into plain-language summaries tailored to an individual’s stage of life. From my experience building learning systems at Edstellar, the real value comes when AI acts as a translator: cutting through jargon and helping people understand the “why” behind decisions. That level of clarity dramatically improves confidence, especially for long-horizon goals like retirement. — Arvind Rongala, CEO, Edstellar

An on-demand Analytical Partner

In my opinion, the best use of AI tools like Grok or ChatGPT when it comes to retirement planning is to enlist it as a personalized, on-demand analytical partner. When you present an AI with your financial data (savings, trajectory, risk profile, retirement age), it has the ability to remit stress testing of your assumptions at a breadth and speed most people will never do for themselves. I have even gone a step further and even asked the AI model to create a variety of long term simulations: good markets, flat markets, inflationary periods, tax shifts, and a few unexpected life surprises here and there. This is when you will feel a much better understanding of what the reality will look like on your retirement path versus static projections.

In my opinion, the best use of AI tools like Grok or ChatGPT when it comes to retirement planning is to enlist it as a personalized, on-demand analytical partner. When you present an AI with your financial data (savings, trajectory, risk profile, retirement age), it has the ability to remit stress testing of your assumptions at a breadth and speed most people will never do for themselves. I have even gone a step further and even asked the AI model to create a variety of long term simulations: good markets, flat markets, inflationary periods, tax shifts, and a few unexpected life surprises here and there. This is when you will feel a much better understanding of what the reality will look like on your retirement path versus static projections.

Where I do think AI can take the planning to another level is the rigor of thinking it is going to force on you. It will find blind spots you didn’t even know to look for, it will challenge your assumptions, it will allow you to show up to your advisor meeting with the potential to be prepared. In the U.S. and Canada—complex situations in retirement planning to say the least, not to mention personal—AI will present a great utility. It won’t replace your financial professional, but it might very well allow you to ask better questions and gain confidence in your decision making. — Kevin Baragona, Founder, Deep AI

AI is NOT a financial advisor

Running a finance team, I’ve found AI like ChatGPT is great for the first pass at retirement planning. It can explain jargon or summarize options way faster than reading a 20-page PDF. But here’s the thing: it’s not a financial advisor. Use it to get the lay of the land, but always talk to a licensed professional before you put any real money in. — Edward Piazza, President, Titan Funding

Treat AI tools as a Scenario Partner

One of the most useful ways I’ve leveraged AI tools like ChatGPT and Grok in the investing and retirement-planning process is by treating them as a “scenario partner.” Not a financial advisor, not a spreadsheet replacement, but a way to explore the assumptions behind long-term decisions.

One of the most useful ways I’ve leveraged AI tools like ChatGPT and Grok in the investing and retirement-planning process is by treating them as a “scenario partner.” Not a financial advisor, not a spreadsheet replacement, but a way to explore the assumptions behind long-term decisions.

When I was first building Zapiy, I didn’t have the luxury of long planning sessions with advisors. I needed quick clarity on questions like how much I should be contributing, how aggressive my allocations should be, or how different timelines would reshape my retirement targets. What I found was that AI excels at helping you pressure-test your thinking before you make any commitments.

I’d feed ChatGPT a basic profile — income, savings rate, intended retirement age, preferred account types like a Roth IRA or TFSA — and ask it to model a few “what if” versions: what if I increase contributions by five percent, what if I shift to a more conservative allocation in my forties, what if I retire earlier but maintain the same lifestyle? The answers weren’t perfect, but they gave me a clearer sense of how small behavioral changes compound over time.

The real value is that this preparation makes every conversation with a human advisor more productive. You walk in understanding your own priorities, trade-offs, and risk tolerance instead of starting from zero. For many investors in the U.S. and Canada, this hybrid approach — AI for exploration, experts for validation — seems to strike the right balance.

If I had to give one recommendation, it would be this: use AI to sharpen your financial instincts, not to substitute professional judgment. Let it help you see the landscape more clearly so you can plan with confidence and ask better questions when it’s time to make real decisions. — Max Shak, Founder/CEO, Zapiy

Large-language models aren’t crystal balls

With new AI tools, the first impulse is always to ask for a prediction. People want to find the next winning stock or time the market perfectly. I’ve seen this happen for decades with every new wave of technology.

With new AI tools, the first impulse is always to ask for a prediction. People want to find the next winning stock or time the market perfectly. I’ve seen this happen for decades with every new wave of technology.

But these large language models aren’t crystal balls. They’re incredibly good at synthesizing information and finding patterns in past data, but they also have a tendency to invent things with absolute confidence.

The hardest part of long-term investing isn’t about finding more data. It’s about managing your own psychology, your biases, and the emotional urge to react to every bit of market noise. This is where AI’s real, and more subtle, value comes in.

My top recommendation is to stop treating these tools like an analyst and start using them as a sparring partner to challenge your own thinking. Instead of asking something simple like, “What are the best Canadian dividend stocks for 2025?”, give it a much more powerful prompt.

Try something like this: “Act as a skeptical financial advisor. My plan is to invest 30% of my retirement portfolio in Canadian dividend stocks for income. Poke holes in this strategy. What are the biggest risks I’m ignoring, what behavioral biases might be at play, and what alternative approaches should I consider?”

What this does is force the AI to act as a “red team” for your own ideas. It uses its vast knowledge of economic principles and market history to find the flaws in your logic before you commit real capital.

This reminds me of a brilliant young engineer I once mentored. He had designed this complex, theoretically perfect trading algorithm and was in love with its elegance. Instead of telling him it would fail, I just spent an hour asking questions.

What happens if this data source is delayed by two seconds? How does the model behave in a flash crash? What’s the single point of failure? He came back two days later and scrapped the whole thing, starting over with a simpler, more resilient design.

The AI can be that patient questioner for you. True financial security isn’t built on finding the perfect answer, but on developing the wisdom to question your own. — Mohammad Haqqani, Founder, Seekario AI Job Search

Use for Stress Testing Assumptions

My top recommendation for using AI tools like Grok or ChatGPT to enhance retirement planning is not to use them for advice, but for stress testing assumptions. Never take financial advice from a large language model. That is a path to financial ruin. Instead, use the AI to aggressively challenge the core numbers you are already getting from a human financial advisor.

My top recommendation for using AI tools like Grok or ChatGPT to enhance retirement planning is not to use them for advice, but for stress testing assumptions. Never take financial advice from a large language model. That is a path to financial ruin. Instead, use the AI to aggressively challenge the core numbers you are already getting from a human financial advisor.

The effective use is feeding the AI a series of complex, negative scenarios based on your existing US or Canadian retirement plan. Ask the AI: “If inflation averages 5% over the next ten years, and my portfolio only returns 4%, where does the system fail?” or “If I move to a high-tax state and health care costs double, how does the plan survive?”

This approach works because it turns the AI into a powerful, objective risk auditor. It exposes the hidden vulnerabilities in your human-designed plan without the emotional filter of your advisor. This is the only high-value application: using AI to force clear, honest conversations about competence and failure points in your retirement strategy, ensuring you have the strongest system possible. — Flavia Estrada, Business Owner, Co-Wear LLC

Use to get a head-start on when to retire

Use AI tools like Grok or ChatGPT to get a head start on how to retire. These services will evaluate the state of your finances and most can administer a wide array of retirement and other accounts then recommend investments that fit your criteria. They demystify complicated financial subjects. They can help you with budgeting, monitor progress and shift plans as markets change. Ask questions in a frame where hopefully will receive clear and good advice. Bots driven by AI help save you time, reduce mistakes and change the way you think about money. It makes retirement planning much simpler and more straightforward. — Keith Sant, Founder & CEO, Kind House Buyers Continue Reading…

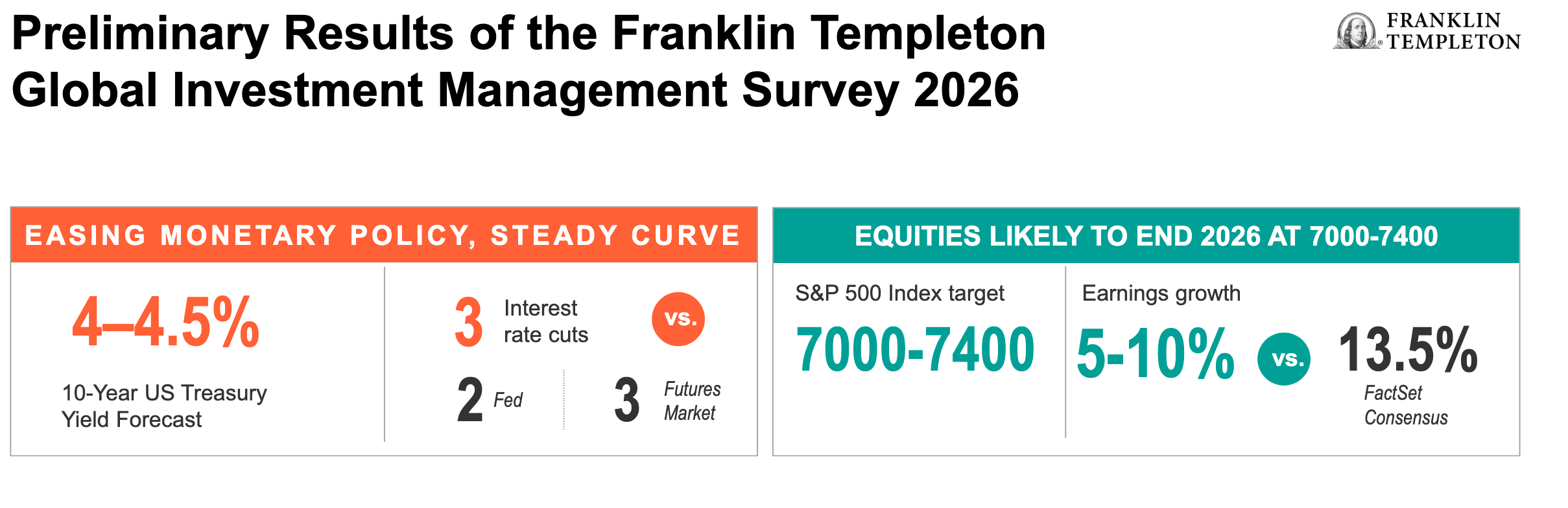

Franklin Templeton’s Investment Outlook for 2026 and beyond was largely positive, judging by the three speakers who presented to advisors and the media at Toronto’s Ritz Carleton Hotel on Tuesday (Nov. 25). In fact, UK-based Global Investment Strategist Michael Browne declared the year now closing, 2025, to be “the Year that the Bear cried Wolf.”

Browne, who is with the Franklin Templeton Institute, released the following preliminary results of Franklin Templeton’s Global Investment Management Survey 2026, shown below:

Browne expects three Fed rate cuts next year and foresees U.S. equities as measured by the S&P500 to end as high as 7400 by the end of 2026.

Like other Templeton executives, Browne expects to see rises in stocks outside the United States. This year, the story has been about growth in the U.S. market and Value in the rest of the world, he said. But even though there are no “Magnificent 7” stocks in Europe or the Emerging Markets — the Mag 7 and their innovation mindset seem unique to the U.S. — he expects a widening and broadening of global markets, with “opportunities in all asset classes.” He expects earnings growth of 5 to 10%, somewhat below the 13.5% Factset consensus.

Corporate margins keep rising, housing markets are weak, and the High-Yield Default Rate is near historically low levels, Browne said, with slides illustrating each point: “Stress indicators do not

point to a severe default cycle in the near term.”

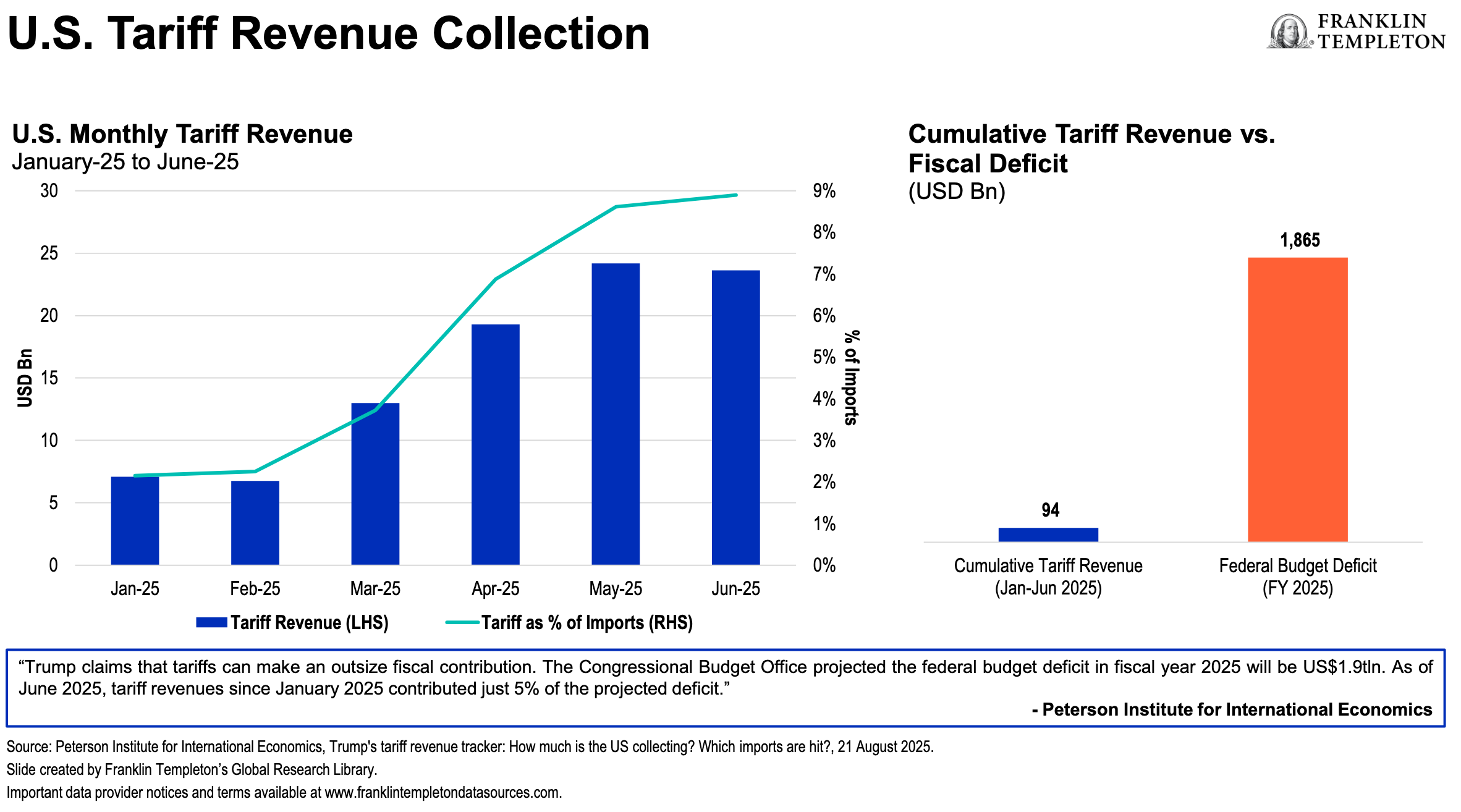

However, Tariff revenue for the U.S. is “unfortunately” high, he said.

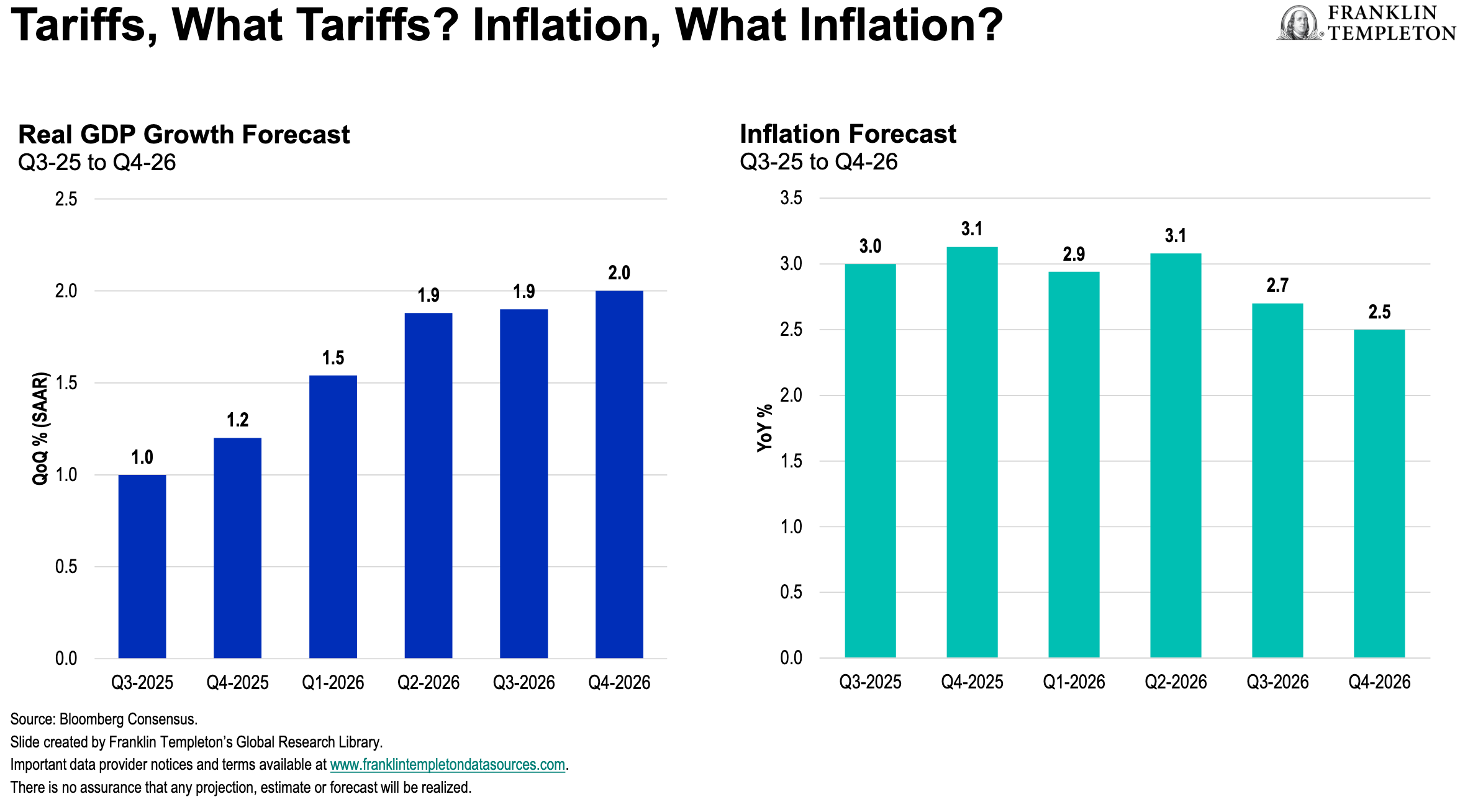

Even so, as the chart below demonstrates, real GDP (Gross Domestic Product) is forecast to rise over 2026 and inflation is expected to be flat to down next year.

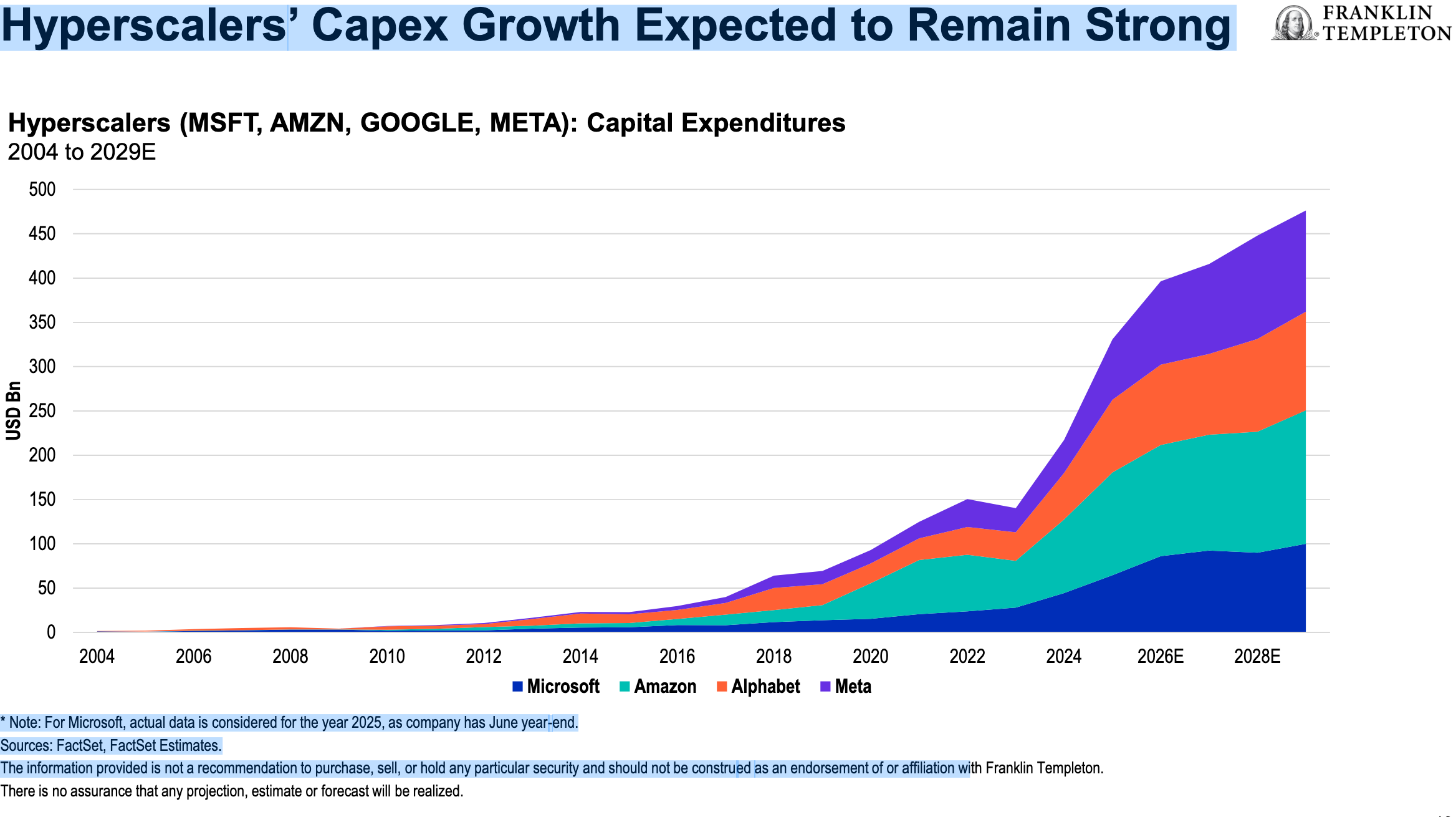

Meanwhile, there is more than US$7 trillion in cash still sitting on the sidelines and capex growth for the big hyperscalers is expected to remain strong, Browne said. They will spend US$3 trillion by the end of the decade and may generate significant returns for the four hyperscalers investing from Cash: Meta, Microsoft, Amazon and Google.

How to spot a Bubble … and a Crash

Browne provided past examples of historic bubbles, ranging from Dutch Tulipmania of 1637 to the American railway mania of the early 1850s, which crashed in 1873, and severe stock market declines in 1907, 1929, 1987, 2001 and 2008.

Bubbles usually end after 7 developments: Debt, Rate rises, a “First Failure,” Confidence fails Reverse Velocity, Margin Calls, Forced or Panic Selling and finally Fraud.

Comparing the 2020s to the 1990s, one of Browne’s slides said “The dot-com bubble burst in 2000: more than five years after the release of Netscape.”

Historically, Global Equities have delivered double-digit gains following Rate cuts and have supported P/E expansions, Browne said. All markets except China are more correlated to the U.S. than in the past. In Emerging Markets, Browne likes India and China: “When the Fed cuts, Emerging Markets fly.”

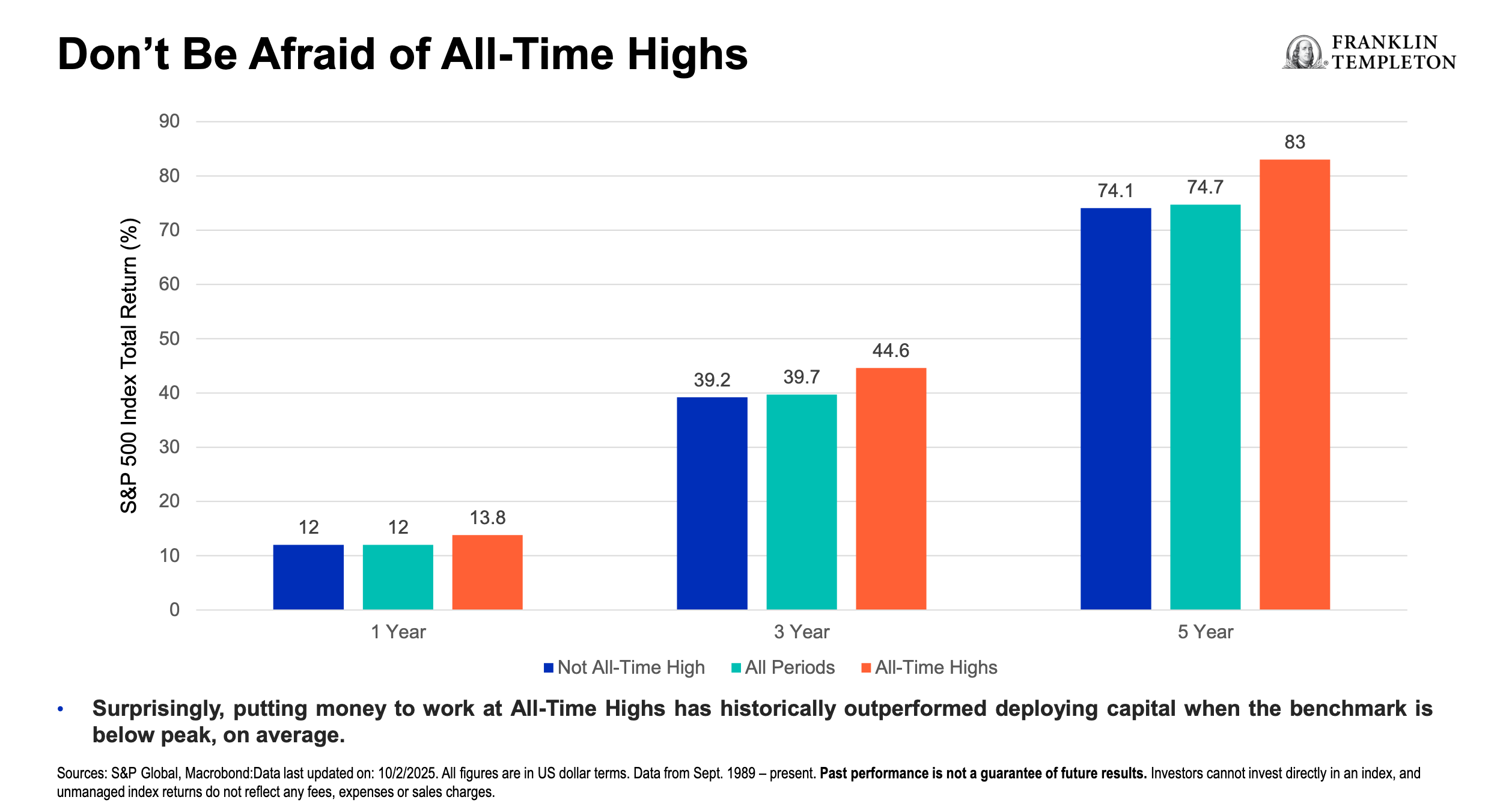

The last scheduled speaker was Jeff Schulze, CFA, Managing Director and Head of Economic and Market Strategy for ClearBridge Investments, who reassured attendees they don’t need to fear the All-Time Highs the U.S. has been experiencing throughout much of 2025:

Schulze says that with possible Tariff Refunds, “we think the economy next year will outperform consensus expectations … We’re buyers of Dips.” While valuations are “full” right now, with the Fed cutting we don’t see multiples going down … for the first time in a long time, diversification will be more additive as we see a broadening out.” The previous laggards will become leaders, including small- and mid- caps and the S&P493 (all but the Mag 7).

One slide on the Tariffs said this: “The Supreme Court may decide that the administration’s IEEPA tariffs need to be refunded, which would be a windfall to corporate America next year. Secretary of the Treasury Scott Bessent has noted that approximately half of the incremental tariff revenue, which is on pace to near $200 billion by year-end, has come from IEEPA tariffs.”