MoneySense.ca: Photo created by snowing – www.freepik.com

MoneySense magazine has begun to publish a package of three mutual fund articles they commissioned me to write. You can find the first article by clicking on the highlighted headline: DSC mutual funds and the future of investment advice. It ran on January 16th.

The first article looks specifically at the gradual decline of the once-ubiquitous DSC sales structure, or Deferred Sales Charge. It recaps recent regularatory developments surrounding DSC, and addresses the related issue of embedded compensation for financial advisors, or so-called Trailer Commissions. These are gradually being eliminated in various Western nations (notably the UK and Australia/NZ) and they are also being phased out in all Canadian provinces, with the conspicuous exception of Ontario.

The lesser-known “Direct-to-Consumer” mutual fund families

When it’s published, the second article will look at two particular “camps” of mutual fund providers: the big-name Embedded Compensation firms you may have heard from (because they can afford to advertise) and a lesser known camp of Direct-to-Consumer managers whose names may be less familiar because they don’t generally have embedded compensation and whose fees are lower and typically mean they don’t have as much money to throw around on big marketing and advertising budgets. The article focusses on four firms in particular you may not have heard of, except through family referrals and word of mouth: Beutel Goodman, Leith Wheeler, Mawer, Steadyhand.

Space precludes mentioning that in the good old days of mutual fund mania (the 90s) there were several other direct-to-consumer firms that either were acquired or are now a shadow of their former selves: the list includes Altamira, Saxon, Sceptre and a few others. We also look at two deep value firms that are still around but get so much publicity about their performance that they can hardly be dubbed as “firms you’ve never heard of.” They are Irwin Michael’s ABC Funds and Francis Chou’s Chou & Associates. Continue Reading…

Author David Aston, whose book becomes available today

Today is the formal release date for David Aston’s new book, The Sleep-Easy Retirement Guide. Below is a Q&A I conducted with David to mark the occasion. See also my review of the book at MoneySense that appeared in December, as well as the Hub’s throw to that piece.

Jon Chevreau: What inspired you to write the book after so many years of writing about Retirement?

David Aston: I have covered most of the key issues in planning for retirement in stand-alone articles I have written over the years. But I wanted to update that advice for current circumstances and figures, show how all the issues fit together as an interconnected whole, and provide it in a combined reference guide that people could have on their shelf and readily turn to when questions came up.

Q2: What do you think about the FIRE movement?

DA: The Financial Independence Retire Early (FIRE) movement is certainly laudable. It’s an admirable concept that people should try to achieve Financial Independence as early as possible, which frees them up to do work that is most meaningful to them (rather than being obligated to do work that maximizes income). As I understand it, it also includes the concept that people should adopt a modest lifestyle that consumes money carefully and wisely without wasting it, which in turn helps make Financial Independence more achievable at a relatively young age. But from what I’ve read, many of the FIRE scenarios are oriented to extreme examples of people trying to achieve Financial Independence in their 30s. So it sometimes comes up as a concept for millennials who are looking for Financial Independence as a near-time goal rather than one that is achieved after a long career at work. That’s only possible for a tiny minority of people. In my experience, it is far more common for people in their 30s to go through a very difficult financial crunch period where they are struggling to buy a house, then make humungous mortgage payments, and cover the expensive costs of raising kids. FIRE goals are not realistic and achievable in your 30s for the vast majority of people. However, the quality of thriftiness and emphasis on saving can be emulated by everyone. I personally think FIRE makes a fair amount of sense for the far more common case of people of average means who might aspire to achieving Financial Independence in their early 60s or possibly their late 50s, but that may not sound particularly appealing to millennials.

Q3: What’s your take on Semi-Retirement and/or Phased Retirement?

DA: The whole world of work for older workers is opening up. The once accepted norm that people retired from their career job to live a life of leisure close to age 65 has pretty much gone out the window. There are lots of expanding options for people to do post-career work that is different than their career job. Often it involves reduced hours, but it can also be full-time work that is less stressful or more fulfilling, or some combination of these attributes. There are various forms of part-time work, contract work, self-employment, consulting or temp work. Often it means switching employers or being self-employed, but it can also mean gearing down to reduced hours or a less stressful role with the same employer. And these post-career options are often started in your early 60s, but they can also happen earlier or later. So there is a vast array of options out there and it’s really up to people to pursue the opportunities that appeal to them the most.

I should mention that “phased retirement” is a term that is sometimes applied to formal corporate programs that allow older employees to adopt a reduced-work schedule or otherwise gear down with the same company prior to full-retirement from their career job. If you go back about 10 years or so, there was an expectation that these kind of corporate programs would increasingly catch on and be offered by major corporations. However, it never really caught on as formal corporate programs that are broadly offered to all older employees. What I have seen happen is that you get a lot of these kind of arrangements to offer reduced hours or less stressful/more fulfilling job functions negotiated on an informal, individual basis. They aren’t offered to everybody in the company. Whether or not an employee can achieve something like that or not depends on the nature of their job, what their boss is looking for, as well as their individual wants and needs. Continue Reading…

My latest MoneySense Retired Money column is one of the first review of financial writer David Aston’s first book, The SleepEasy Retirement Guide. The subtitle bills the book as answering “the 12 biggest financial questions that keep you up at night.” Click on the highlighted text to retrieve the full column: Good News — Your RRSP is probably in better shape than you think.

Aston is a long-time freelance financial writer, and is also a MoneySense writer. I got to know him when I was the editor and always enjoyed editing his popular Retirement column in the magazine. Now 63, after a corporate career spanning management consulting, corporate financial planning, and operations, Aston turned to financial journalism, which he has now been doing for 12 years.

As I note in the review, I had a small role to play in the creation of this book, since I introduced David to the publisher: Milner & Associates Inc., which is also the publisher of Victory Lap Retirement, coauthored by myself and Mike Drak.

In the case of Aston’s new book, I have to say it seems to have been a good piece of literary matchmaking. In due course, we hope to run some excerpts and/or blogs from David here on the Hub.

A nice feature of the book are the many charts and tables that spell out just how much money you need to accumulate to retire at various ages, whether a “barebones” el cheapo lifestyle, or a high-end luxury one defined as $100,000 in annual income for couples ($80,000 for singles) or the vast swath of retired lifestyles in between. Whether you’re single or half of a couple, all the numbers you need to project finances into your future golden years are there. For most of the calculations in these charts, Aston created simple Excel spreadsheets.

No need for $1 million unless you want a deluxe Retirement

Financial writer and author David Aston

And, as is often made clear at MoneySense.ca, you don’t necessarily need $1 million to retire, although you will need that much and more if you are counting on a deluxe retirement with all the bells and whistles (exotic travel once or twice a year, two cars in the garage, eating out regularly, etc.). Continue Reading…

‘Tis the season for the annual investment outlook, with a new year and some might argue a new decade ahead of us. While some pundits hold fire on their prognostications until January, a few big-name investment firms have just come out with their 2020 prognostications.

Among the early entrants was Franklin Templeton, which provided its predictions last week in Montreal and again yesterday (Dec. 10th) in Toronto. Also yesterday, Vanguard put out a release headlined Economic and Market Outlook 2020: Lower Growth Expectations in the New Age of Uncertainty.

Franklin Templeton is a well-known manager of actively managed mutual funds, and has now been in Canada for 65 years, going back to Sir John Templeton’s famous Templeton Growth Fund. Vanguard is best known for its “passive” or indexing approach to investing, both through index mutual funds and ETFs, although it is also an active manager. But their respective outlooks for the next year and decade are not too different, with investment returns projected to stay positive, albeit with cautions to investors not to expect quite as strong returns as they have received in the last decade.

Vanguard said global growth is set to slow in 2020, driven by US and China trade concerns and continued political uncertainty leading to depressed global economic activity.

Todd Schlanger, senior investment strategist at Vanguard Canada, said: “Investors should prepare for a lower-return environment over the next decade, with periods of market volatility in the near-term. We expect uncertainty stemming from geopolitics, policymaking, and trade tensions to undermine global growth over the coming year … For Canada, the picture is slightly rosier, with a resilient labour market and robust wage growth leading to growth levels stronger than most developed economies in 2020, with a slight improvement over 2019.”

Vanguard’s main bullet points were these:

It forecasts continued slowdown in global growth but Canada will be a bright spot among developed economies: Canadian growth is forecast at 1.6%, U.S. growth forecast at 1.0%, Eurozone, 1.0%, China at 5.8%

Canadian equity market returns are forecast to be 3.5%-5.5%, annualized over the next ten years

Canadian fixed income returns are likely to be 1.5%-2.5%, annualized over the next ten years.

Vanguard says global central banks have moved from expected policy tightening heading into 2019 to additional policy stimulus amid weakening growth outlooks and inflation shortfalls this year. It expects the US federal reserve to cut the federal funds rate by 25 to 20 basis points before the end of 2020. However, it expects the Bank of Canada to keep interest rates at current levels throughout 2020. While Canadian growth is stable, rising household debt levels and high exposure to global economic uncertainty “skew the balance of risks to the downside.” Schlanger advises Canadian investors to prepare for volatility over lack of trade clarity and slowing economic growth in the U.S. by maintaining diversified portfolios, keeping investment costs low and focusing on the long term while tuning out the daily noise.

Global stocks still have more performance potential than global bonds

Meanwhile, Franklin Templeton believes global stocks have “greater performance potential than global bonds, supported by continued global growth.” Over the next seven years it forecasts strong return potential for both bonds and equities in Emerging Markets. And with short-term interest rates below historical averages, “we see a lower performance potential for government bonds.”

William Yun, Franklin Templeton Multi-asset Solutions

Franklin Templeton recommends a multi-asset approach to deal with an environment of desyncronized global growth and moderate inflation worldwide.

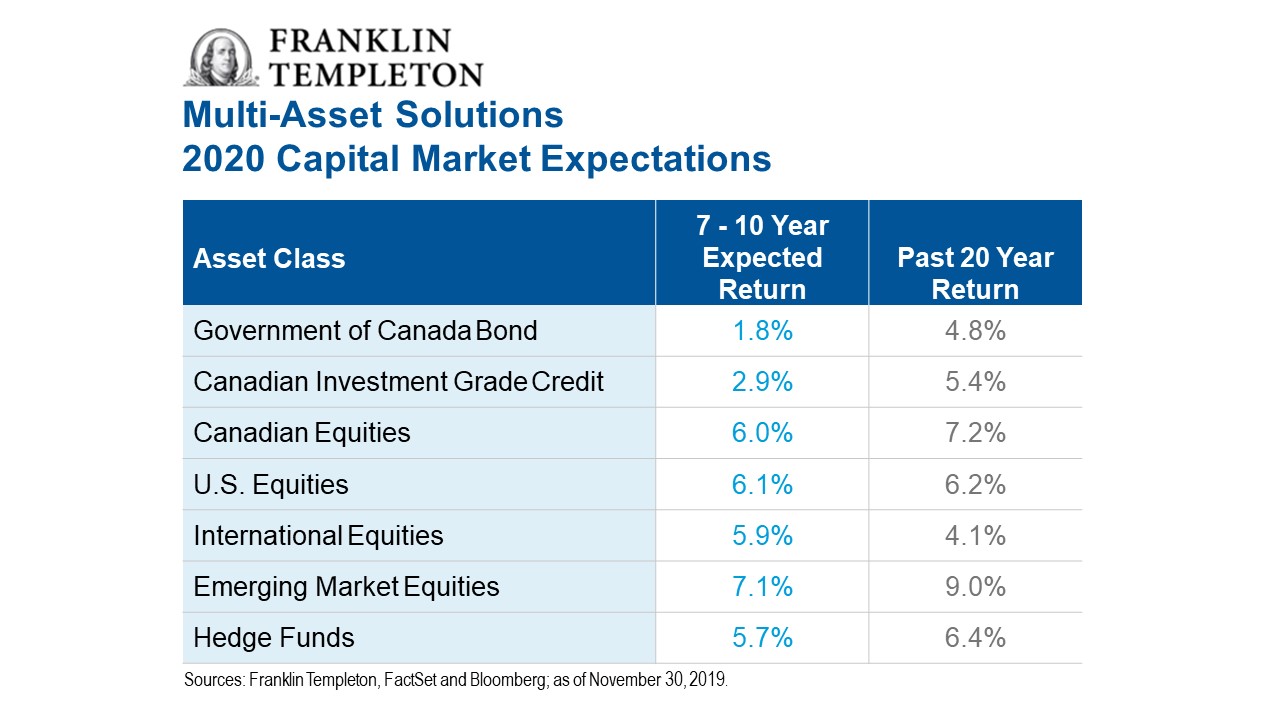

Bill Yun, executive vice president and investment strategist for Franklin Templeton Multi-Asset Solutions (pictured left) said the firm’s 7-year outlook for Canadian bonds the next 7 years is about 1.8% a year, versus 4.8% the past 20 years. Equity return expectations are all positive but reduced from the performance of the prior 20 years: 6% going forward for Canadian equities, versus a historical 7.2%; 6.1% for US equities compared to 6.2% the previous two decades; International equities are projected to return 5.9% versus an historic 4.1%; Emerging Markets 7.1 versus 9% historic, and hedge funds 5.75 compared to 6.4% in the past.

Global central banks have little ammo left

One positive for Canada is that the Bank of Canada has more room to cut rates to cope with an economic slowdown than most central banks in the rest of the world. Canada and the US both have room to cut but Europe does not, Yun said. Some rates are negative in parts of Europe. Continue Reading…

My latest MoneySense Retired Money column looks at a problem some think is a nice one for retirees to have: can an RRSP — and ultimately a RRIF — ever become too large? You can find the full column by clicking on the adjacent highlighted headline: How large an RRSP is too large for Retirement?

This is a surprisingly controversial topic. Some financial advisors advocate “melting down” RRSPs in the interim period between full employment and the end of one’s 71st year, when RRIFs are typically slated to begin their annual (and taxable) minimum withdrawals. Usually, RRSP meltdowns occur in your 60s: I began to do so personally a few years ago, albeit within the confines of a very conservative approach to the 4% Rule.

As the piece points out, tax does start to become problematic upon the death of the first member of a senior couple. At that point, a couple no longer has the advantage of having two sets of income streams taxed in two sets of hands: ideally in lower tax brackets.

True, the death of the first spouse may not be a huge tax problem, since the proceeds of RRSPs and RRIFs pass tax-free to the survivor, assuming proper beneficiary designations. But that does result in a far larger RRIF in the hands of the survivor, which means much of the rising annual taxable RRIF withdrawals may start to occur in the higher tax brackets. And of course if both members of a couple die with a huge combined RRIF, their heirs may share half the estate with the Canada Revenue Agency.

For many seniors, the main reason to start drawing down early on an RRSP is to avoid or minimize clawbacks of Old Age Security (OAS) benefits, which begin for most at age 65. One guideline is any RRSP or RRIF that exceeds the $77,580 (in 2019) threshold where OAS benefits begin to get clawed back. Of course you also need to consider your other income sources, including employer pensions, CPP and non-registered income.

Adrian Mastracci

“A nice problem to have.”

But the MoneySense column also introduces the counterargument nicely articulated by Adrian Mastracci, fiduciary portfolio manager with Vancouver-based Lycos Asset Management. Mastracci, who is also a blogger and occasional contributor to the Hub, is fond of saying to clients “A too-large RRSP is a nice problem to have!”

Retirement can last a long time: from 65 to the mid 90s can be three decades: a long time for portfolios to keep delivering. A larger RRIF down the road gives retirees more financial options, given the ravages of inflation, rising life expectancies, possible losses in bear markets, low-return environments and rising healthcare costs in one’s twilight years. These factors are beyond investors’ control, in which case Mastracci quips, “So much for the too-big RRSP.”