While 70% of Americans say they saved for retirement in 2016, many are anxious about the level of their savings and the need to direct money towards other goals and expenses, says a Harris Poll of 2,000 American adults conducted by the personal finance site NerdWallet. You can find the full results here.

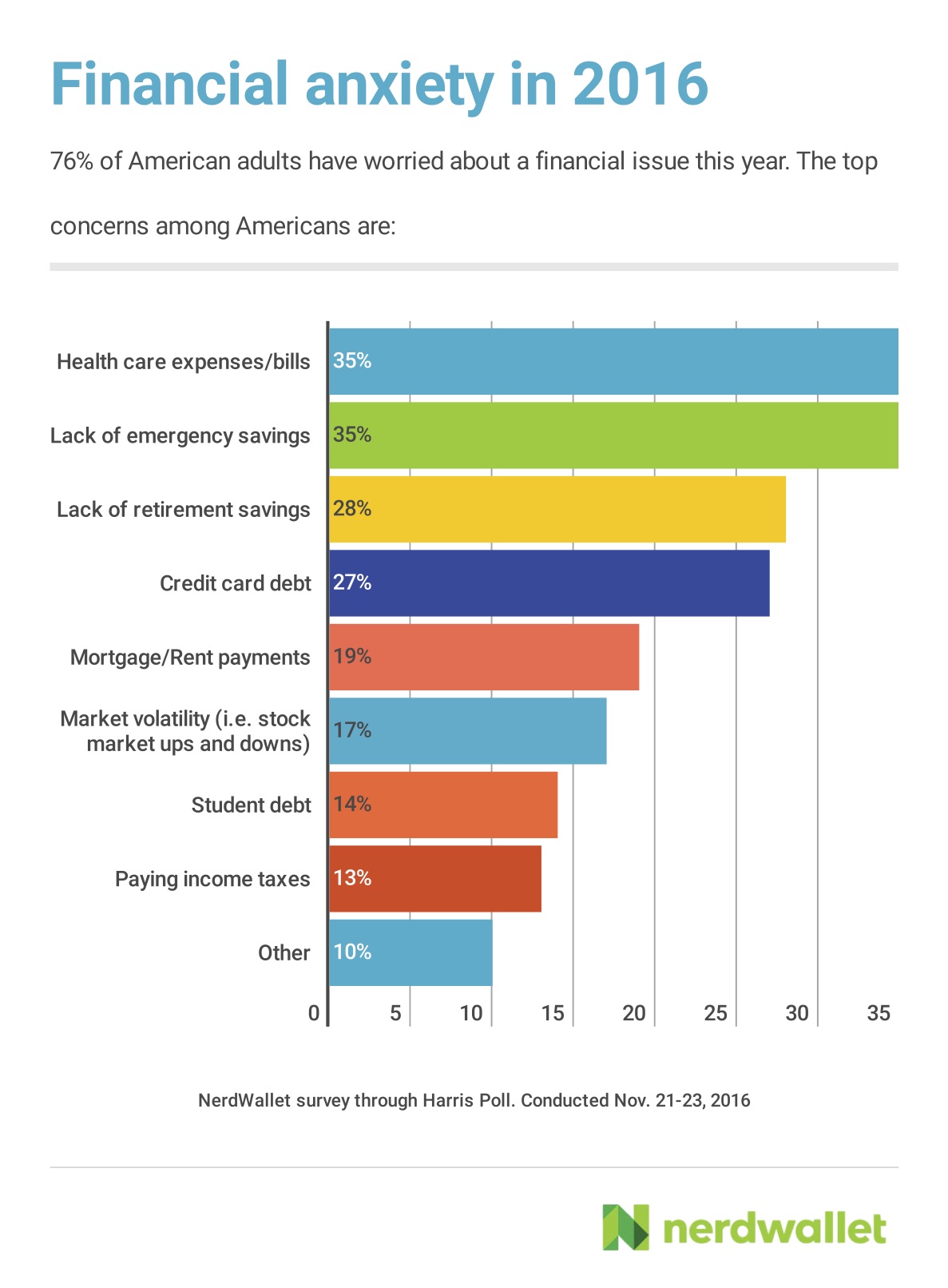

Other major financial concerns include lack of emergency funds (cited by 35%), health care expenses (also 35%)and credit-card debt (27%). Retirement remains the most commonly cited savings priority (mentioned by 28% surveyed) but only 29% feel confident they saved enough in 2016, while one in three aren’t saving for retirement at all (including 43% of Millennials aged 18 to 24). Lesser forms of financial anxiety in 2016 include making mortgage or rent payments (19%), stock market volatility (17%), student debt (14%), and paying income taxes (13%).

Next year may not be much better: of those with workplace pensions, only 32% plan to increase their contributions in 2017. Older Americans aged 45 to 54 are most likely to report concern about lack of retirement savings (40% surveyed), while only 20% are confident they saved enough this year.

Savers should favour tax-advantage accounts over savings accounts

Subsequent to that, my latest MoneySense Retired Money blog looks at the topic of estate planning as it related to Tax-free Savings Accounts (TFSAs). To access the full blog, click on the highlighted text here: Why your TFSA needs a Successor Holder.

We had mentioned in an earlier blog that TFSAs were excellent vehicles for estate planning and minimizing tax of families as a whole. See How TFSAs can aid your Victory Lap.

We also said that it’s by far preferable for couples to name each other Successor Holders on their respective TFSAs. Otherwise, things get pretty complex, which is what the MoneySense blog goes into in some depth.

TFSA succession planning often not well understood

Sandy Cardy

The blog is based largely on input from Mackenzie Investments and a brochure it published entitled What happens to your TFSA at the time of death?, which you can access in full by clicking on the link. It also quotes regular Hub contributor Sandy Cardy, who was the head of tax and estate planning at Mackenzie when that brochure was published. In that role, she was responsible for educating the financial advisors who sell mutual funds on estate planning, including its role in TFSAs. As she notes in the MoneySense blog, this topic of TFSAs at death is not well understood even by some financial professionals.

The popularity of exchange-traded funds (ETFs) in Canada continues to surge and 31% of domestic investors now report they own ETFs, says BlackRock Canada’s first-ever ETF Pulse Survey, released Friday.

Furthermore, 93% of existing ETF owners and 38% of non-owners are interested in buying ETFs in the next 12 months. The survey suggests education plays a big role in the adoption of ETFs: more than half of Canadian investors plan to learn more about ETFs in 2017 and non ETF investors are more than twice as likely to seek out more ETF knowledge next year.

41% are replacing mutual funds with ETFs

Not surprisingly, the survey found that 41% of investors polled are choosing ETFs largely to replace mutual funds while 45% are doing so to replace individual stocks. Improved diversification was cited by 53% while 43% felt ETFs would help reduce their risk profile. BlackRock added that these findings are consistent with a Greenwich Survey of Canadian institutional ETF users, which pointed to a rise in ETF allocations among institutional investors in the coming year.

My latest MoneySense Retired Money column on TFSAs is now online. You can read the whole thing by clicking on this highlighted link: How retirees can use TFSAs to save on tax.

I’m a huge fan of The Tax-free Savings Account or TFSA both for young people and for seniors, and everyone between.

It’s the single most powerful investment tax shelter available to Canadian investors. (For any American readers, the TFSA is roughly the equivalent of Roth IRAs).

So if you’re a member of the much-touted “Millennial” generation, you should move heaven or earth to maximize the annual $5,500 contribution as soon as you turn 18 – even if you have to solicit a “matching” contribution from your parents.

If you’ve not yet opened up a TFSA, as of 2017 the cumulative TFSA room built up since the plan’s debut in 2009 will be $52,000. As I say in the column, for millennials the combination of the newly expanded Canada Pension Plan and a TFSA maximized from age 18 on means that by the time they are old enough to read the Retired Money column, they will be well positioned for retirement.

While late for Boomers, TFSAs can still be a boon in retirement

But as this particular MoneySense column has been dubbed “Retired Money,” the focus is on what the TFSA can do for near-retirees and seniors already retired. When it first came out in 2009, we aging baby boomers lamented the fact the TFSA hadn’t been available when we we were just starting out.

KIPPERS. Should parents dip into retirement savings to help their kids?

As regular Hub readers may know, I often write financial articles for other (mostly) digital media, usually the Financial Post, MoneySense.ca and Motley Fool Canada. Here’s some of the most recent blogs or columns, with links via the headlines.

Nearing Retirement and still insecure about your finances? Sadly, you’re not alone. (FP, Nov. 17)). This came out of a survey released this week by Mackenzie Investments that suggested many of us actually feel less secure financially about retirement the closer the actual date arrives. One reason is grey divorce and another perhaps related one is dipping into retirement savings to help adult children.

KIPPERS stands for Kids in Parents’ Pockets Eroding Retirement Savings. I also mentioned this in a short segment on this topic on Tuesday with Peter Armstrong on CBC’s On the Money show.

That of course touched on the new book I’ve coauthored with Mike Drak, Victory Lap Retirement. The FP has also been running excerpts of the book the last several Mondays. You can find the first four here. Number 5 is slated for next Monday. By the way, co-author and fellow blogger Mike Drak and I both plan to attend the Canadian Personal Finance Conference 2016 this weekend in Toronto. Hope to see other financial bloggers there!

Earlier this week, Motley Fool Canada ran my take on investing in the post-Trump-victory world: Don’t dump your long-term investment plan over Trump’s victory. And it’s just published my latest quarterly report for Stock Advisor Canada, this one on CRM2 and Best Interest (only subscribers with a user name/password combo can access this).

Over at MoneySense.ca on November 11th was the online version of my most recent column from the November issue of the magazine, which is on annuities: How to win using annuities in retirement.

Hey, no one promised my Victory Lap Retirement would be easy!

While 70% of Americans say they saved for retirement in 2016, many are anxious about the level of their savings and the need to direct money towards other goals and expenses, says a Harris Poll of 2,000 American adults conducted by the personal finance site NerdWallet. You can find the full results here.

While 70% of Americans say they saved for retirement in 2016, many are anxious about the level of their savings and the need to direct money towards other goals and expenses, says a Harris Poll of 2,000 American adults conducted by the personal finance site NerdWallet. You can find the full results here.