My latest MoneySense Retired Money column looks in-depth at a new “Decumulation” offering from Sun Life, unveiled late in September. You can find the full column by clicking on the highlighted headline: What is Sun Life’s new decumulation product?

As you can see from image below taken from MyRetirement Income’s website, the emphasis is on providing regular income to last to whatever age a retiree specifies. That income is not, however, guranteed as a life annuity would be.

The Globe & Mail’s Rob Carrick first wrote about this shortly after the Sun announcement. My column adds the opinions of such varied Canadian retirement experts as author and finance professor Moshe Milevsky, retired actuary Malcolm Hamilton, Caring for Clients’ Rona Birenbaum and Trident Financial’s Matthew Audrey, as well as Sun Life Senior Vice President, Group Retirement Services, Eric Monteiro.

Some of the more cynical takes are that this is a way for Sun Life to continue to profit from client financial assets gathered during the long accumulation phase, rather than seeing them migrate to other solutions, such as annuities provided by either one of its own life insurance arms or that of rivals.

Aiming for Simplicity and Flexibility

As Sun’s Eric Monteiro told me in a telephone interview, the company’s preliminary research found that rival products that were first on the market (see full MoneySense column) were often perceived as complicated, and as a result uptake of some of these pioneering Decumulation products have been underwhelming. It sought to create a solution that was relatively simple and flexible.

In essence, it is not dissimilar to some Asset Allocation ETFs, such as Vanguard’s VRIF, which is 50% equities and 50% fixed income. But Sun’s product may and probably will have different proportions of the major asset classes. In fact, it lists 16 external global money managers who deploy up to 15 different asset classes, which include Emerging Market Debt, Liquid Real Assets, Direct Infrastructure, Liquid Alternatives and Direct Real Estate. Managers include BlackRock Asset Management, Lazard Asset Management, Phillips, Hager & North, RBC Global Asset Management and its own Sun Life Capital Management. Continue Reading…

Top investment executives told a webinar held Wednesday morning that investors should not mix Politics and Investing. Even so, while market observers at Franklin Templeton view the upcoming U.S. election as essentially a “toss-up” they seem to believe that a victory or sweep by the Republicans’ Donald Trump would be more positive for stocks than a Kamala Harris win.

Grant Bowers, portfolio manager and Senior Vice President for Franklin Equity Group, said “it’s a 50/50 tossup for the presidential winner. Both candidates are well known so it’s not surprising” there’s been little market volatility in the runup to the November 5th election. Generally, he’s bullish no matter the outcome. The economy did well in Trump’s first term while a Harris victory would be a continuation of Biden policies. The real differences are on tariffs, fiscal policy and regulation. “The most likely outcome is a split government” but there would be more volatility if there is a sweep by either party.

Of course, it’s quite possible that investors won’t know the official outcome for several weeks. If the process of counting votes drags on and there are legal challenges like there were in 2020, investors can expect more protracted volatility.

Sonai Desai, Chief Investment Officer for Franklin Templeton Fixed Income said the U.S. economy is set to do “quite well. I agree there’s a reduced probability of Recession: that’s not our baseline for a while.” If there’s a Republican sweep and broader tariffs measures introduced by Trump, “that might limit the Fed’s appetite for massive rate cuts.” Her baseline is that even with a Republican sweep, there won’t be a literal imposition of tariffs: that didn’t happen in 2016, so “I don’t think we will get the full range of cross-the-board tariffs.” Either way, the mighty U.S. consumer will “continue to consume and I don’t see that changing with the Election.”

Clearbridge’s Jeffrey Schulze

In the very long run, of course, any short-term market volatility from elections is likely to be a blip, which is why Franklin Templeton tells clients not to mix investing and politics.

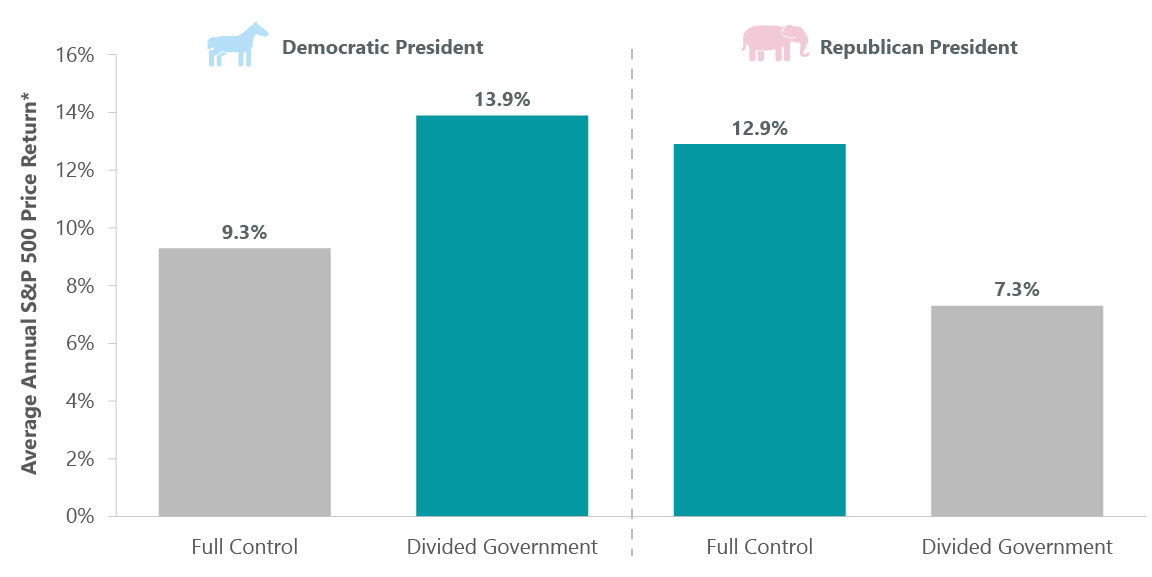

In an analysis released early in October, Clearbridge Investments Head of Economic and Market Strategy Jeffrey Schulze, CFA, showed the following annual returns for the S&P500, all positive for equities no matter which party wins and whether or not they get full control or are in a divided government. Based on that, the best outcomes for investors would be a Democratic president with a Divided Government or Full Control by a Republican president.

“We view a Trump win, likely coming in a sweep scenario, as net positive for equities as it preserves favorable corporate tax treatment and builds on tax elements that expired,” Schulze wrote in the October 1st update, “A Harris win, likely coming with a divided Congress, would be mildly negative due to fewer provisions of expiring tax legislation getting extended due to political gridlock.”

Trump win likely positive for Stocks

“In aggregate, we view a second Trump presidency under a sweep scenario as net positive for equities. The expectation is for a more favorable corporate tax regime and less of a regulatory burden, both of which should boost corporate profits. Conversely, there is the potential for increased tariffs and retaliation from U.S. trade partners … We view U.S. stocks as best placed under Trump, with banks and capital markets, as well as the oil and gas complex, well positioned due to lighter regulation. Aerospace and defense is also likely going to benefit as well as biopharmaceuticals. Areas that could see pressure are restaurants and leisure, due to the less availability of labor, as well as EVs, autos and clean energy producers.”

Harris win might be “mildly negative” for Stocks

A Kamala Harris win would be less positive for U.S. stocks, Schulze writes: “We see a Harris win as mildly negative to equities should she preside over a divided Congress. It will be more of a headwind to the markets should we see a Democratic sweep as she will then be able to implement higher taxes on corporations and high-income individuals, as well as push a more ambitious regulatory agenda. However, tax credits for low-income individuals would provide an offset, creating an economic boost to this segment of the economy.Tighter regulation could weigh on biopharmaceuticals, banks, capital markets, energy as well as mega cap technology. But again, we caution against basing investment or portfolio positioning solely on the regulatory environment. Areas to be bullish about under Harris would be consumer discretionary, specifically restaurants & leisure, home building and building products.”

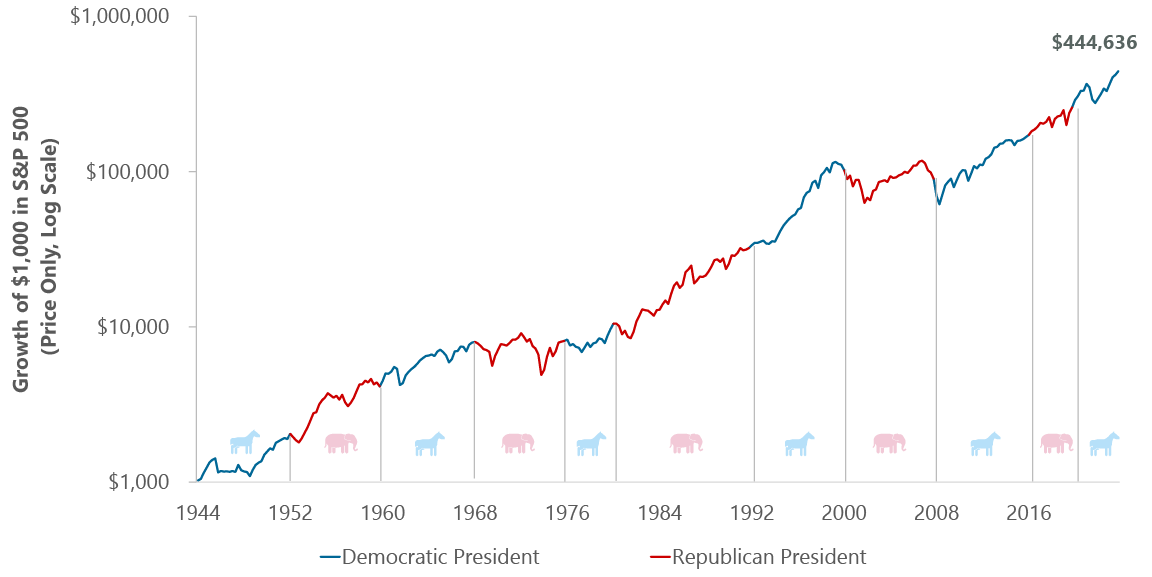

Generally, Franklin Templeton continues to advocate a “stay the course” stance for investors geared to the long term. The chart below shows that going back to 1944, the U.S. stock market has risen steadily over time regardless of which political party is in the White House.

Stephen Dover, chief market strategist and Head of Franklin Templeton Institute, acted as Moderator in Wednesday’s webinar, fielding audience questions. He also wrote a U.S. election update earlier this month, headlined “Uncertainty Reigns.”

He concluded back then that the election remains “too close to call. A divided government in Washington, DC, with no single party controlling the White House, Senate and House of Representatives is likely … Investors should gird themselves for uncertainty and potential bouts of volatility preceding and following election day. It is quite possible that the outcome for the presidency will not be settled until the December 17 certification deadline.”

Dover expects market uncertainty to continue well past November 5th, if not until January’s inauguration of the ultimate winner.”Legal challenges, some of which have already commenced, add to uncertainty. Re-counts, delays and disputes over certification of results, alongside courtroom litigation are virtually assured if state election outcomes are close. Various legal and procedural challenges are likely to endure until at least December 17, which is the deadline for state certification of the presidential election results and the official nomination of state electors to the Congressional certification on January 6, 2025.”

However, Dover says his basic investment conclusions remain unchanged. They are as follows: Continue Reading…

We provided a sneak preview of RetireMint late in August, which you can read here: Retirement needs a new definition. That was provided by RetireMint founder Ryan Donovan.

The MoneySense column goes into more depth, passing on my initial experiences using the program, as well as highlighting a few social media comments on the product and some user experiences provided by RetireMint.

RetireMint (with a capital M, followed by a small-case letter I rather than an e) is a Canadian retirement tool that just might affect how you plan for Retirement. There’s not a lot of risk as you can try it for free. One thing I liked once I gave it a spin is that it isn’t just another retirement app that tells you how much money you need to retire. It spends as much or more time on the softer aspects of Retirement in Canada: what you’re going to do with all that leisure time, travelling, part-time work, keeping your social networks intact and so on.

In that respect, the ‘beyond financial’ aspects of RetireMint remind me of a book I once co-authored with ex corporate banker Mike Drak: Victory Lap Retirement, or indeed my own financial novel Findependence Day. As I often used to explain, once you have enough money and reach your Financial Independence Day (Findependence), everything that happens thereafter can be characterized as your Victory Lap.

As Donovan puts it, this wider definition must “break free from the tethered association of solely financial planning.”

Donovan says roughly 8,000 Canadians will reach retirement every single week over the next 15 years. And yet more than 60% of them do not know their retirement date one year in advance, and more than a third will delay their retirement because they don’t have a plan in place.

Retirement not calendar date or amount in your bank account

Donovan says “Retirement has become so synonymous with financial planning, and so associated with ‘old age,’ that they’re practically inseparable. Yet, in reality, retirement is a stage of life, not a date on the calendar, an amount in your bank account, and is certainly not a death sentence.” He doesn’t argue that financial planning is the keystone of retirement preparation, as “you won’t even be able to flirt with the idea of retiring without it.” But it’s much broader in scope than that. As he puts it, this wider definition must “break free from the tethered association of solely financial planning.” Continue Reading…

In what it says is its first new ETF announcement in four years, Vanguard Investments Canada Inc. today announced a new Fixed-Income ETF designed to met investors’ short-term savings needs. Here is the full release on Canada News Wire.

Trading on the TSX under the ticker VVSG, Vanguard Canada says the Vanguard Canadian Ultra-Short Government Bond Index ETF offers AAA-rated high-quality government bonds and treasury bills with a low management fee of 0.10%. It seeks to track the Bloomberg Canadian Short Treasury 1-12 month Float Adjusted Index. The release says the ETF will invest primarily in public, investment-grade government fixed-income securities with maturities of less than 365 days issued in Canada.

Vanguard Canada’s first new ETF in 4 years

In an email to me, Vanguard Canada spokesman Matthew Gierasimczuk confirmed “It’s our first ETF launch in four years.” It brings the total number of Vanguard ETFs in Canada to 38, with $80 billion (CAD) in Canadian ETF assets under management. You can find the full list on its website here. Continue Reading…

At first glance, reverse mortgages sound appealing, especially for those whose wealth mostly resides in their home equity. If you have little other sources of future retirement income, and especially if you have no heirs who will be annoyed at having a reduced inheritance, then the prospect of living in your home in old age and generating tax-optimized retirement income to boot does sound appealing.

Have your Home and your Money too?

As P.J. Wade wrote in her 1999 book, Have Your Home and Money Too, reverse mortgages can be “your best friend or your worst enemy … your choice!”

However, there’s not a lot of Reverse Mortgages available in Canada. The two main ones of which I’m aware are Equitable Bank and HomeEquity Bank (aka CHIP). According to Rates.ca “Reverse mortgages always cost more than conventional mortgages because the lender’s funding costs are higher.”

The full column includes input from occasional MoneySense contributor Allan Small, who is a senior investment advisor with IA Private Wealth Inc. as well as a podcaster. He says reverse mortgages “have not played a part in any of the retirement plans and retirement planning that I have done so far in my career. I think the reverse mortgage idea or concept for whatever reason has not caught on.” Also, “those individual investors I see usually have money to invest, or they have already invested. Most downsize their residence and take the equity out that way versus pulling money out of the property while still living in it.”

Milevsky: It all depends on to what a financial strategy is compared

For me, the definitive word on Reverse Mortgages or any other financial instrument goes to noted Finance professor and author Moshe Milevsky. He told me in an email that when it comes to reverse mortgages – or any other financial strategy or product in the realm of decumulation – “I always ask this question before giving an opinion: Compared to what?” He worries about the associated interest rate risk, which is “difficult to control, manage or even comprehend at advanced ages with cognitive decline.”

What are the alternatives to a reverse mortgage? Is it selling the house and moving? Or, Milevsky asks, “Is the alternative reducing your standard of living? Is the alternative taking a loan from a local bookie? It’s the alternative that determines whether the reverse mortgage is a good idea or not … Generally I will not rule them out and I think they will continue to grow in popularity among retiring boomers, but I wouldn’t place them at the very top of the to-do list when you get to your golden years.”