By Kevin Flanagan, WisdomTree Investments

Special to the Financial Independence Hub

One of the lynchpins behind the Federal Reserve’s (Fed) decision-making process thus far in 2017 has apparently been the altered inflation landscape. The policy makers seem to be more comfortable that deflationary conditions have passed and that inflation will be “running close to the Committee’s 2 per cent longer-run objective.” Does that mean that fixed-income investors should be fearful of the inflation bogeyman rearing its ugly head anytime soon?

Calendar year 2017 did get off to a somewhat unexpected start on the inflation front. Indeed, the Consumer Price Index (CPI), perhaps the most widely followed gauge on price developments, revealed some visible upside during the winter months. According to the Bureau of Labor Statistics (BLS), overall CPI rose as high as +2.7%1 in February on a year-over-year basis, the strongest performance in five years.

In fact, as recently as July of last year, the figure came in as low as +0.8%2. The Fed’s preferred measure of inflation, the price index for personal consumption expenditure (PCE) exhibited a similar pattern, coming in at a five-year high watermark of +2.1%3 and crossing the FOMC’s mentioned 2% threshold in the process.

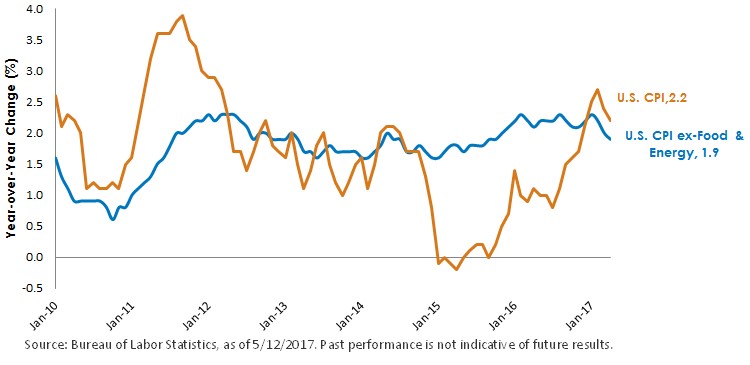

Core inflation slowing

Interestingly, inflation has not exhibited any further upward momentum in the months that followed. To provide some perspective, the year-over-year gains for CPI and the PCE price index have since dropped back to +2.2%4 and +1.8%5, respectively, in the latest data available.

Core inflation, such as the CPI excluding food and energy, is another closely monitored inflation gauge, as it removes those sometimes-volatile components and is viewed as a better barometer of demand pressures within the underlying economic setting. In the most recent BLS report, the 12-month increase for CPI ex-food and energy had slowed to +1.9%6, the lowest tally since October 2015 (shown in the chart at the top of this blog.)

Wage inflation

One area of importance when focusing on the potential for higher inflation is wages. The latest monthly jobs report did not display any further upside on this front, as average hourly earnings rose at an annual rate of +2.5%7, well within the recent band, since this time last year.

A broader measure of compensation is the Employment Cost Index (ECI), which includes wages and salaries as well as benefits, and is measured on a quarterly basis. For the three months ending in March, the ECI posted a 12-month gain of 2.4%8, the highest reading since 2008, certainly a trend for fixed income investors to keep an eye on in the months ahead.

Conclusion

Inflation expectations and actual inflation data should continue to be watched closely by both the Fed and the fixed-income markets in the months ahead. Against this backdrop, the break-even inflation rate, or the difference between the yield on a nominal bond (such as the U.S. Treasury 10-Year note) and an inflation-linked or real yield bond with the same maturity (such as the 10-Year U.S. Treasury Inflation-Protected Securities or TIPS), will serve as a useful guide regarding inflation expectations.

As of this writing, that rate has actually fallen to 1.84%9, as compared to its recent high point of 2.08%10 in January. Even with this pullback in inflation expectations, the path of least resistance still leads to the Fed implementing another rate hike at its upcoming policy meeting on June 13/14, a development the money and bond markets have fully discounted at this point.

1Source: Bureau of Labor Statistics, 5/12/2017.

2Source: Bureau of Labor Statistics, 5/12/2017.

3Source: Bureau of Economic Analysis, 5/1/2017.

4Source: Bureau of Labor Statistics, 5/12/2017.

5Source: Bureau of Economic Analysis, 5/1/2017.

6Source: Bureau of Labor Statistics, 5/12/2017.

7Source: Bureau of Labor Statistics, 5/5/2017.

8Source: Bureau of Labor Statistics, 4/28/2017.

9Source: Bloomberg, as of 5/15/2017.

10Source: Bloomberg, 5/15/2017.

Kevin Flanagan is the Senior Fixed Income Strategist for WisdomTree’s Investment Strategy group. In this role, he contributes to the asset allocation team, writes fixed income-related content and travels with the sales team, conducting client-facing meetings and providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was most recently a Managing Director. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S in Finance from Fairfield University.

Kevin Flanagan is the Senior Fixed Income Strategist for WisdomTree’s Investment Strategy group. In this role, he contributes to the asset allocation team, writes fixed income-related content and travels with the sales team, conducting client-facing meetings and providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was most recently a Managing Director. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S in Finance from Fairfield University.

Commissions, management fees and expenses all may be associated with investing in WisdomTree ETFs. Please read the relevant prospectus before investing. WisdomTree ETFs are not guaranteed, their values change frequently and past performance may not be repeated. Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates. “WisdomTree” is a marketing name used by WisdomTree Investments, Inc. and its affiliates globally. WisdomTree Asset Management Canada, Inc., a wholly-owned subsidiary of WisdomTree Investments, Inc., is the manager and trustee of the WisdomTree ETFs listed for trading on the Toronto Stock Exchange.